HSBC 2008 Annual Report Download - page 205

Download and view the complete annual report

Please find page 205 of the 2008 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

|

|

203

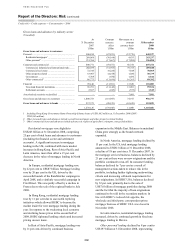

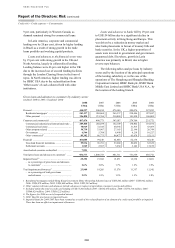

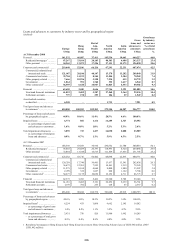

21 per cent of total loans and advances to customers

(including the financial sector and settlement

accounts).

In Europe, other personal lending declined

by 11 per cent from the end of 2007 to

US$54 billion. The decrease was primarily

attributable to the UK as a stronger focus on secured

lending restricted originations in the unsecured

portfolio. The sale of certain non-core credit card

portfolios in the first half of 2008 also contributed to

the decrease in the UK. In France, balances declined

due to the sale of the regional banks in the second

half of 2008. In Turkey, continued expansion of the

branch network during 2008 resulted in higher

balances, particularly in credit cards and overdrafts.

In Hong Kong, other personal lending declined

by 2 per cent to US$13 billion. HSBC remained the

market leader for credit cards in Hong Kong based

on cards in circulation, cardholder spending and

balances.

In Rest of Asia-Pacific, other personal lending

rose by 12 per cent, primarily due to strong growth

in the Middle East. Elsewhere in the region, balances

rose in Malaysia and Indonesia.

In North America, other personal lending

balances declined by 12 per cent to US$97 billion. In

the US, consumer finance business and credit card

lending fell due to the combined effect of tighter

underwriting criteria and lower marketing

expenditure. A reduction in non-credit card personal

lending reflected the decision to cease new business

in guaranteed direct mail loans and personal home-

owner loans in the second half of 2007, and tighter

underwriting criteria applied to originations in the

remainder of the portfolio. In the mortgage services

business, second lien balances declined due to the

continued run-off of the portfolio following the

cessation of originations in 2007. Lower vehicle

finance lending at HSBC Finance reflected the

discontinuation of certain product offerings and the

cessation of new vehicle loan originations from the

dealer and direct-to-consumer channels in July 2008.

HSBC USA also discontinued originations of

indirect vehicle finance loans, but second lien loans

increased following a promotional campaign

channelled through the branch network in the first

half of 2008. In Canada, lower balances were

attributable to the disposal of the vehicle finance

businesses during the year.

In Latin America, other personal lending rose by

9 per cent to US$15 billion. Lending growth was

primarily concentrated in Brazil and reflected strong

demand for payroll loans and vehicle lending. In

Mexico, balances were broadly in line with

31 December 2007 and the mix was adjusted

towards customers of higher credit quality. Further

growth was restricted as risk appetite was adjusted

by closing certain products to new originations and

tightening underwriting criteria on cards, leading to a

sharp reduction in the number of cards issued in

2008.

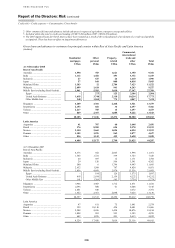

Loans and advances to corporate and

commercial customers rose by 19 per cent to

US$407 billion, with strong growth across all

regions. Lending was primarily concentrated in

Europe, where it accounted for 54 per cent of

advances to this sector, of which more than

40 per cent were in the UK.

In Europe, corporate and commercial advances

rose by 24 per cent. In the UK, lending rose by

35 per cent, driven by growth in lending to large

corporates. Balances declined in France due to the

sale of the regional banks in July 2008.

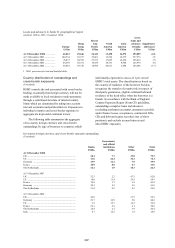

In Hong Kong, corporate and commercial

lending rose by 19 per cent, driven by higher lending

in commercial, industrial and international trade,

commercial real estate and other property-related

sectors.

In Rest of Asia-Pacific, strong corporate and

commercial lending growth was experienced in the

Middle East and Singapore, which rose by 26 per

cent and 50 per cent respectively and, to a lesser

extent, in Malaysia, India and Taiwan, the latter due

to the acquisition of the assets and liabilities of The

Chinese Bank in March 2008. In the Middle East,

the corporate and commercial loan book continued

to grow, owing to an expansion of lending in UAE,

particularly for trade and investment projects, in

addition to general business growth. In Singapore,

higher lending was driven by strong demand from

the international trade sector. Lending in Japan

declined due to the closure of inactive and

unprofitable accounts, and lending in mainland

China fell as a result of tightened government

regulations and tighter lending criteria in response to

the weakening local economy. This partly offset the

strong growth elsewhere in the region.

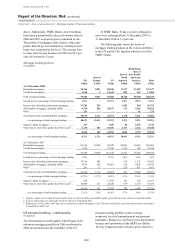

In North America, corporate and commercial

lending increased by 7 per cent, driven by growth in

HSBC USA and, to a lesser extent, in Canada.

In HSBC USA, higher lending to corporate and

commercial clients reflected the targeted expansion

of middle market activities and the drawdown of

existing credit facilities, partly offset by a decline in

commercial real estate activity as the bank managed

down its lending exposures in light of lower risk

appetite and a deterioration in market conditions. In

Canada, corporate and commercial lending rose by