HSBC 2008 Annual Report Download - page 125

Download and view the complete annual report

Please find page 125 of the 2008 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

|

|

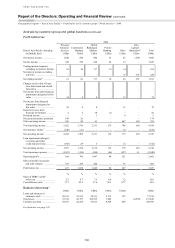

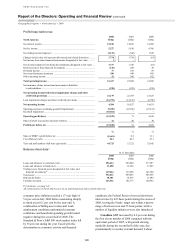

123

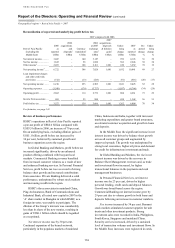

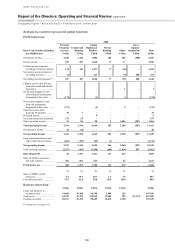

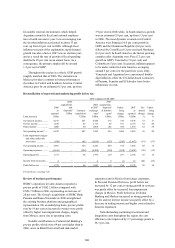

HSBC USA, loan impairment charges rose by 76 per

cent to US$2.6 billion driven by credit quality

deterioration across the Home Equity line of credit,

Home Equity loan, prime first lien residential

mortgage and private label card portfolios.

Loan impairment charges in US card and retail

services rose, driven by portfolio seasoning and

rising unemployment, particularly in the second half

of 2008, higher levels of personal bankruptcy filings

and lower recovery rates. As with mortgages, this

was most notable in parts of the country most

affected by house price falls and unemployment.

Vehicle finance loan impairment charges rose as

delinquencies rose and lower prices resulted in lower

recoveries when repossessed vehicles were sold at

auction.

Loan impairment charges in Commercial

Banking grew to US$449 million from a low base,

primarily driven by higher impairment losses due to

deterioration across the middle market, commercial

real estate and corporate banking portfolios in the

US and among firms in the manufacturing, export

and commercial real estate sectors in Canada. Higher

loan impairment charges and other credit risk

provisions in Global Banking and Markets reflected

weaker credit fundamentals in the US in 2008.

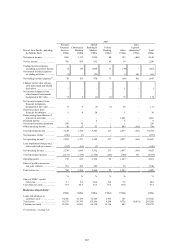

Operating expenses increased by 90 per cent,

driven by US$10.6 billion of impairment charge

recognised in respect of North America Personal

Financial Services in 2008 to fully write off

goodwill. Excluding the goodwill impairment

charge, expenses were US$1.1 billion or 11 per cent

lower. Staff costs declined, primarily in HSBC

Finance, following decisions taken in 2007 to close

the acquisition channels for new business in

Mortgage Services and a number of consumer

lending branches, and integrate the operations of the

card businesses. HSBC USA made the decision to

close its wholesale and third-party correspondent

mortgage business in November 2008, while HSBC

Finance took the decision to cease originations in the

dealer and direct-to-consumer channels in the

vehicle finance business in July 2008. Staff costs

in Global Banking and Markets also fell as

performance-related compensation and staff

numbers both declined.

Other administrative costs decreased as

origination activity declined, marketing costs in card

and retail services reduced and branch costs in

consumer lending fell as tightened underwriting

criteria curtailed business and led to branch closures.

This was partly offset by higher marketing and

occupancy costs in the retail bank reflecting a

continued expansion of the branch network,

increased community investment activities and

higher deposit insurance, collection, payments and

cash management and asset management costs in

support of business growth.

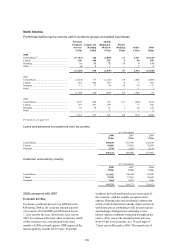

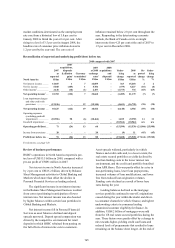

2007 compared with 2006

Economic briefing

In the US, GDP growth in 2007 was 2.2 per cent,

0.7 percentage points less than that recorded in 2006

as the housing-led downturn gathered pace.

Consumer spending in 2007 grew by 2.9 per cent,

the weakest annual expansion since 2003. Housing

activity continued to weaken in 2007, with

residential investment falling by 17 per cent during

the year. Both new and existing home sales also

declined to new lows in 2007. The unemployment

rate averaged 4.6 per cent in 2007, with the average

in the second half of the year slightly higher at

4.8 per cent. The trade deficit narrowed in 2007 as

export growth strengthened. Consumer price

inflation averaged around 4 per cent in the final

quarter of 2007. This was largely due to higher

energy prices; excluding food and energy, consumer

price inflation averaged 2.3 per cent in the fourth

quarter. The Federal Reserve lowered short-term

interest rates by 100 basis points in the second half

of 2007, from 5.25 per cent to 4.25 per cent, as

policymakers attempted to mitigate the worst effects

of the sub-prime related credit squeeze upon

economic activity. 10-year note yields reached a

high of 5.3 per cent in June 2007, before falling to

4 per cent by the year-end. Declines in the final

months of 2007 left the S&P 500 stock market index

practically unchanged compared with the end of 2006.

Canadian GDP increased by 2.4 per cent during

the first eleven months of 2007 compared with the

equivalent period of 2006. Domestic demand

remained strong despite tighter credit conditions in

the latter part of the year, supported by the robust

labour market. The unemployment rate averaged

6 per cent for the year, reaching a historical low of

5.8 per cent in October. After hitting a high of

2.5 per cent in April, core consumer price inflation

slowed to 1.5 per cent by the end of 2007. The

Canadian dollar appreciated during the year,

particularly in the second half. In July, the Bank of

Canada raised its overnight interest rate from

4.25 per cent to 4.5 per cent before reversing this

move in the final weeks of 2007.

Review of business performance

HSBC’s operations in North America experienced a

significant fall in pre-tax profits of 98 per cent in

2007, on both reported and underlying bases.