HSBC 2008 Annual Report Download - page 127

Download and view the complete annual report

Please find page 127 of the 2008 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

|

|

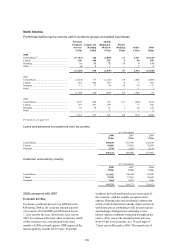

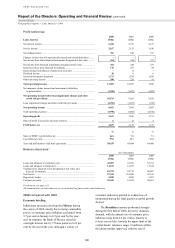

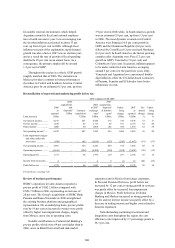

125

contrast, foreign exchange trading performance

was strong, supported by activity generated by a

weakening dollar and volatile markets.

Net income from financial instruments

designated at fair value rose to US$1.8 billion,

driven by significant fair value movements on

HSBC’s own debt as a result of the widening of

credit spreads and related derivatives in the second

half of the year.

Gains less losses from financial investments of

US$245 million were primarily attributable to the

sale of shares in MasterCard.

Net earned insurance premiums decreased by

9 per cent to US$449 million, as the decline in loan

volumes led to a fall in credit insurance sales and

HSBC stopped reinsuring credit insurance for other

lenders.

Other operating income decreased significantly,

as higher losses were recorded on foreclosed

properties due to the combined effect of an increase

in the stock of such properties and a reduction in

their value due to falling prices. In addition, there

were lower gains on the sale of investments, mainly

due to a significant one-off gain in the latter part of

2006.

Net insurance claims incurred and movement in

liabilities to policyholders decreased by 7 per cent to

US$241 million, in line with the change in net

earned insurance premiums.

Loan impairment charges posted a steep rise,

increasing by 79 per cent to US$12.2 billion,

reflecting substantially higher charges in the US

consumer finance loan book, primarily in mortgage

lending but also in the credit cards portfolio in the

final part of the year. The main factor driving this

deterioration was the effect of the weaker housing

market on both economic activity and the ability of

borrowers to extend or refinance debt. In addition,

seasoning and mix change within the credit cards

portfolio and increases in bankruptcy filings after

the exceptionally low levels seen in 2006, following

changes in legislation, added to loan impairment

charges.

The real estate secured portfolios experienced

continuing deterioration in credit quality as a lack of

demand for securitised sub-prime mortgages and

falls in house prices severely restricted refinancing

options for many customers. Loan impairment

charges rose by 41 per cent to US$3.1 billion and by

139 per cent to US$4.1 billion in the mortgage

services business and consumer lending,

respectively. Delinquency rates exceeded recent

historical trends, particularly for those loans

originated in 2005 and 2006. Performance was

weakest in housing markets which had previously

experienced the steepest home price appreciation,

second lien products and stated income products.

US card services experienced a rise in loan

impairment charges from a combination of factors,

primarily a growth in balances, higher losses in the

final part of the year as the economy slowed, a rise

in bankruptcy rates to levels approaching those seen

historically, and a shift in portfolio mix towards non-

prime loans.

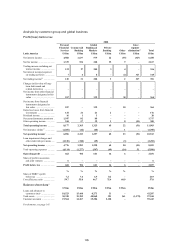

Loan impairment charges in Commercial

Banking rose by 151 per cent to US$191 million,

reflecting growth in the loan book, the increasing

probability of default among commercial real estate

loans in the US and a change in methodology for

determining loan impairment allowances on a

portfolio of revolving loans to small businesses. In

addition, in Canada, loan impairment charges

increased due to exposure to certain sectors affected

by the strength of the Canadian dollar and an

impairment charge for non-bank asset-backed

commercial paper was also taken.

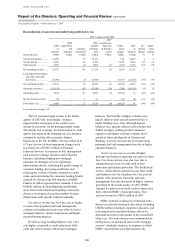

Operating expenses increased by 3 per cent,

compared with growth in net operating income

before loan impairment charges of 5 per cent. The

retail bank branch network was extended both within

and beyond the Group’s traditional spheres of

operation to support the expansion of the Personal

Financial Services and Commercial Banking

businesses in the US and Canada. Premises and

equipment expenses rose as a consequence. The

consumer finance business incurred restructuring

charges from the discontinuation of the wholesale

and correspondent channels in mortgage services and

the closing of branch offices in consumer lending.

There were corresponding benefits in origination

costs. The Canadian consumer finance business was

also restructured in a similar fashion to the US. The

business incurred US$70 million of one-off costs

arising from the indemnification agreement with

Visa ahead of Visa’s planned IPO. In the cards and

consumer lending businesses, communication

expenses increased due to higher mailing volumes

on cards and consumer lending as credit collection

policies were tightened. In the third quarter,

however, expenditure on card marketing declined in

line with a decision to slow lending growth.

Share of profit in associates and joint ventures

declined to US$20 million.