HSBC 2008 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2008 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

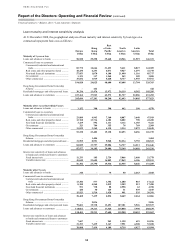

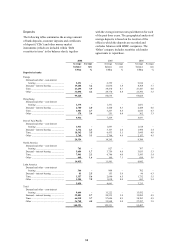

Critical accounting policies

64

The best evidence of fair value is a quoted price

in an actively traded market. In the event that the

market for a financial instrument is not active, a

valuation technique is used. The majority of

valuation techniques employ only observable market

data, and so the reliability of the fair value

measurement is high. However, certain financial

instruments are valued on the basis of valuation

techniques that feature one or more significant

market inputs that are unobservable. Valuation

techniques that rely to a greater extent on

unobservable inputs require a higher level of

management judgement to calculate a fair value than

those based wholly on observable inputs.

Valuation techniques used to calculate fair

values include comparisons with similar financial

instruments for which market observable prices

exist, discounted cash flow analysis, option pricing

models and other valuation techniques commonly

used by market participants. Valuation techniques

incorporate assumptions that other market

participants would use in their valuations, including

assumptions about interest rate yield curves,

exchange rates, volatilities, and prepayment and

default rates. When valuing instruments by reference

to comparable instruments, management takes into

account the maturity, structure and rating of the

instrument with which the position held is being

compared.

The main assumptions and estimates which

management considers when applying a model with

valuation techniques are:

• the likelihood and expected timing of future

cash flows on the instrument. These cash flows

are usually governed by the terms of the

instrument, although management judgement

may be required when the ability of the

counterparty to service the instrument in

accordance with the contractual terms is in

doubt. Future cash flows may be sensitive to

changes in market rates;

• selecting an appropriate discount rate for

the instrument. Management bases the

determination of this rate on its assessment of

what a market participant would regard as the

appropriate spread of the rate for the instrument

over the appropriate risk-free rate; and

• judgement to determine what model to use to

calculate fair value in areas where the choice of

valuation model is particularly subjective, for

example, when valuing complex derivative

products.

When applying a model with unobservable

inputs, estimates are made to reflect uncertainties

in fair values resulting from a lack of market data

inputs, for example, as a result of illiquidity in the

market. For these instruments, the fair value

measurement is less reliable. Inputs into valuations

based on unobservable data are inherently uncertain

because there are little or no current market data

available from which to determine the level at which

an arm’s length transaction would occur under

normal business conditions. However, in most cases

there are some market data available on which to

base a determination of fair value, for example

historical data, and the fair values of most financial

instruments will be based on some market

observable inputs even where the unobservable

inputs are significant.

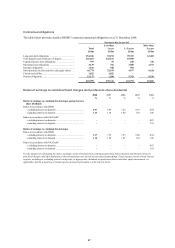

An analysis of the basis for valuation of

financial instruments measured at fair value in the

financial statements is provided on page 162. The

value of financial assets and liabilities that use a

valuation technique are US$876 billion (2007:

US$626 billion) and US$671 billion (2007: US$401

billion) or 71 per cent (2007: 66 per cent) and 83 per

cent (2007: 68 per cent) of total assets and total

liabilities measured at fair value, respectively. A

sensitivity analysis of fair values for financial

instruments with significant unobservable inputs to

reasonably possible alternative assumptions and a

range of assumptions and inputs used in valuation

models in respect of instruments of particular

interest in the current market turmoil can be found

on page 164. Given the uncertainty and subjective

nature of valuing financial instruments at fair value,

it is possible that the outcomes in the next financial

year could differ from the assumptions used, and this

could result in a material adjustment to the carrying

amount of financial instruments measured at fair

value.

Impairment of available-for-sale financial

assets

HSBC’s accounting policy for impairment of

available-for-sale financial assets is described in

Note 2(j) on the Financial Statements.

Available-for-sale financial assets are measured

at fair value, and changes in fair value are recognised

in equity in the available-for-sale fair value reserve

until the financial assets are either sold or become

impaired. An impairment loss is recognised if there

is objective evidence of impairment as a result of

loss events which have an impact on the estimated

future cash flows of the financial asset that can be

reliably estimated. If an available-for-sale financial

asset becomes impaired, the entire balance in equity