HSBC 2008 Annual Report Download - page 124

Download and view the complete annual report

Please find page 124 of the 2008 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

|

|

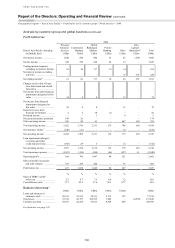

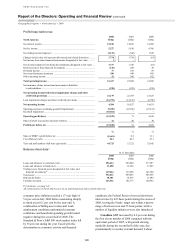

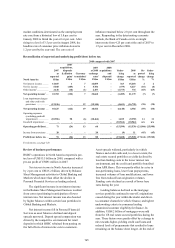

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

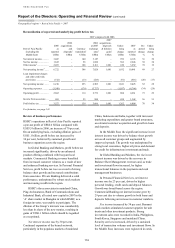

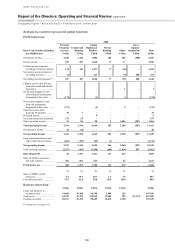

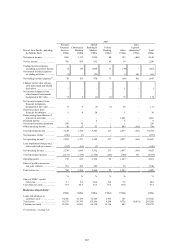

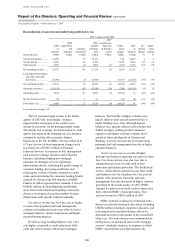

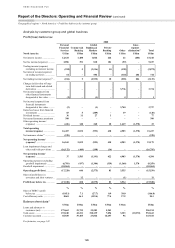

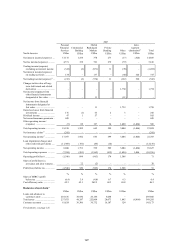

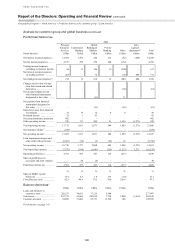

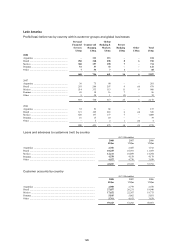

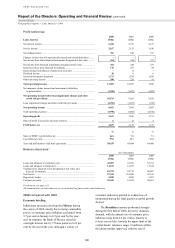

Geographical regions > North America > 2008 / 2007

122

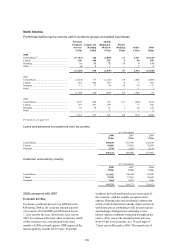

February 2009, HSBC authorised the discontinuation

as soon as practicable of all new receivable

originations of all products by the branch-based

consumer lending business of HSBC Finance in

North America (see page 70).

Net fee income declined by 8 per cent, driven by

reductions in US credit card fees following changes

in fee practices implemented since the fourth quarter

of 2007 and lower cash advance and interchange fees

as a result of reduced volumes. Partly offsetting the

decline were increased income from enhancement

services due to higher customer acceptance rates of

Account Secure Plus and Identity Protection Plan,

a rise in syndication, credit and service fees in

Commercial Banking and increased fees from asset

management.

Trading losses were dominated by write-downs

in Global Banking and Markets on legacy exposures

as continuing turmoil in credit markets adversely

affected valuations of credit and structured credit

trading positions, monoline exposures and leveraged

and acquisition finance loans. Continued

deterioration in the fair value of the run-off portfolio

of sub-prime residential mortgage loans held for sale

also contributed to the loss. US$3.6 billion in

leveraged loans, high yield notes and securities held

for balance sheet management were reclassified in

2008 under revised IFRS rules from trading assets

to loans and receivables and available for sale,

preventing any further mark-to-market trading losses

on these assets. If these reclassifications had not

been made, the loss before tax would have been

US$0.9 billion higher.

The losses on legacy assets were partly offset

by strong performances in other trading areas as

foreign exchange trading benefited from pronounced

market volatility, Rates trading correctly anticipated

central bank rate cuts and gains were generated on

credit default swaps in Global Banking. Revenues

from emerging markets trading and precious metals

trading also rose as a result of ongoing market

volatility and increased transaction volumes as

prices of gold and platinum rose during 2008.

Losses on non-qualifying hedge positions in interest

rate swaps generated further trading losses. In 2007,

the Decision One business, which was closed that

year, recorded trading losses of US$263 million.

Net income from financial instruments

designated at fair value rose by US$2.0 billion to

US$3.7 billion, primarily on HSBC’s fixed-rate

long-term debt as credit spreads widened

significantly in the second half of 2008 in the

ongoing market turmoil. These gains, together with

those booked in previous years, will fully reverse

over the life of the debt.

Gains less losses from financial investments

declined, mainly due to losses on US government

agency securities in 2008 and the non-recurrence of

the sale of MasterCard shares, partly offset by gains

from the Visa IPO in 2008.

Net earned insurance premiums decreased by

13 per cent to US$390 million, driven by lower

credit related premiums in HSBC Finance due to

declining loan volumes.

Other operating income declined due to losses

on sale of the Canadian vehicle finance businesses

and other loan portfolios in 2008, in addition to the

non-recurrence of gains on disposal of fixed assets

and a small portfolio of private equity investments in

2007.

Net insurance claims incurred and movement in

liabilities to policyholders were broadly in line with

2007 at US$238 million.

Loan impairment charges and other credit

risk provisions rose sharply, by 38 per cent to

US$16.8 billion, reflecting substantially higher

impairment charges in HSBC Finance across all

portfolios and, in HSBC USA, the deterioration of

credit quality in prime residential mortgages, second

lien portfolios and private label cards. The main

factors driving this deterioration were the continued

weakening of the US economy, which led to rising

levels of unemployment and personal bankruptcy

filings: higher early-stage delinquency and increased

roll rates in consumer lending: the ageing of

portfolios: and further declines in house prices which

increased loss severity and reduced customers’

ability to refinance and access equity in their homes.

Partly offsetting these factors was a reduction in

overall lending as HSBC continued to actively

reduce its balance sheet and lower its risk profile in

the US.

In the Mortgage Services business, loan

impairment charges rose by 14 per cent to

US$3.5 billion as the 2005 and 2006 vintages

continued to season and experience rising

delinquency. Run-off of the portfolio slowed in light

of continued house price depreciation which, along

with the constrained credit environment, restricted

refinancing options for personal customers. In

consumer lending, loan impairment charges rose by

39 per cent to US$5.7 billion. In the second half

of 2008, delinquency rates began to accelerate

particularly in the first lien portfolios in the parts

of the country most affected by house price

depreciation and rising unemployment rates. In