HSBC 2008 Annual Report Download - page 259

Download and view the complete annual report

Please find page 259 of the 2008 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

|

|

257

contracts, so they are not included in the insurance

risk management analysis.

Life business tends to be longer-term in nature

than non-life business and frequently involves an

element of savings and investment in the contract.

Accordingly, separate tables are provided for life and

non-life businesses, reflecting their distinctive risk

characteristics. The life insurance risk table provides

an analysis of insurance liabilities as the best

available overall measure of insurance exposure,

because provisions for life contracts are typically set

by reference to expected future cash outflows

relating to the underlying policies. The table for non

life business uses written premiums as the best

available measure of risk exposure because policies

are typically priced by reference to the risk being

underwritten.

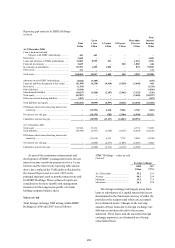

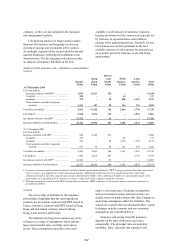

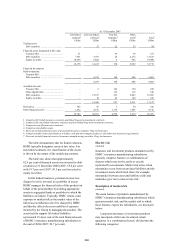

Analysis of life insurance risk – liabilities to policyholders

(Audited)

Europe

Hong

Kong

Rest of

Asia-

Pacific

North

America

Latin

America

Total

US$m US$m US$m US$m US$m US$m

At 31 December 2008

Life (non-linked)

Insurance contracts with DPF1 ....................... 1,015 11,213 216 – – 12,444

Credit life ........................................................ 252 – – 65 – 317

Annuities ........................................................ 379 – 28 805 1,363 2,575

Term assurance and other long-term

contracts ..................................................... 1,316 107 99 136 376 2,034

Total life (non-linked) ........................................ 2,962 11,320 343 1,006 1,739 17,370

Life (linked) ........................................................ 1,548 2,276 310 – 1,933 6,067

Investment contracts with DPF1,2 ....................... 17,732 – 34 – – 17,766

Insurance liabilities to policyholders .................. 22,242 13,596 687 1,006 3,672 41,203

At 31 December 2007

Life (non-linked)

Insurance contracts with DPF1 ........................... 940 8,489 231 – – 9,660

Credit life ........................................................ 235 – – 82 – 317

Annuities ........................................................ 413 – 28 1,154 1,532 3,127

Term assurance and other long-term

contracts ..................................................... 675 74 85 125 307 1,266

Total life (non-linked) ........................................ 2,263 8,563 344 1,361 1,839 14,370

Life (linked) ........................................................ 1,720 2,019 467 – 2,193 6,399

Investment contracts with DPF1,2 ....................... 18,954 – 29 – – 18,983

Insurance liabilities to policyholders .................. 22,937 10,582 840 1,361 4,032 39,752

1 Insurance contracts and investment contracts with discretionary participation features (‘DPF’) can give policyholders the contractual

right to receive, as a supplement to their guaranteed benefits, additional benefits that may be a significant portion of the total

contractual benefits, but whose amount and timing is determined by HSBC. These additional benefits are contractually based on the

performance of a specified pool of contracts or assets, or the profit of the company issuing the contracts.

2 Although investment contracts with DPF are financial investments, HSBC continues to account for them as insurance contracts as

permitted by IFRS 4.

(Audited)

The above table of liabilities to life insurance

policyholders highlights that the most significant

products are investment contracts with DPF issued in

France, insurance contracts with DPF issued in Hong

Kong and unit-linked contracts issued in Hong

Kong, Latin America and Europe.

The liabilities for long-term contracts are set by

reference to a range of assumptions which include

lapse and surrender rates, mortality and expense

levels. These assumptions typically reflect each

entity’s own experience. Economic assumptions,

such as investment returns and interest rates, are

usually based on market observable data. Changes in

underlying assumptions affect the liabilities. The

sensitivity of profit after tax and shareholders’ equity

to changes in both economic and non-economic

assumptions are considered below.

Insurance risk arising from life insurance

depends on the type of business, and varies

considerably. The principal risks are mortality,

morbidity, lapse, surrender and expense levels.