Xerox 2012 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2012 Xerox annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

93Xerox 2012 Annual Report

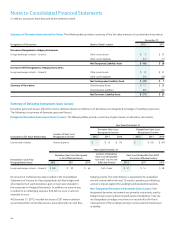

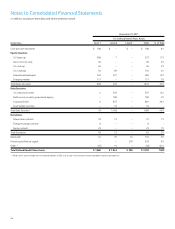

Retiree Health

Year Ended December 31,

2012 2011 2010

Components of Net Periodic Benefit Costs:

Service cost $ 9 $ 8 $ 8

Interest cost 42 47 54

Recognized net actuarial loss 1 – –

Amortization of prior service credit (41) (41) (30)

Net periodic benefit cost 11 14 32

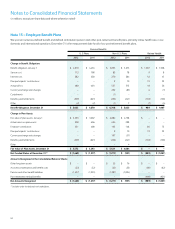

Other changes in plan assets and benefit

obligations recognized in

Other Comprehensive Income:

Net actuarial loss 18 25 13

Prior service credit (6) (3) (86)

Amortization of net actuarial loss (1) – –

Amortization of net prior service credit 41 41 30

Total recognized in Other

Comprehensive Income 52 63 (43)

Total recognized in Net Periodic Benefit Cost

and Other Comprehensive Income $ 63 $ 77 $ (11)

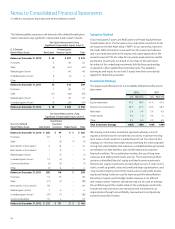

The net actuarial loss and prior service credit for the defined benefit

pension plans that will be amortized from Accumulated other

comprehensive loss into net periodic benefit cost over the next fiscal

year are $106 and $(2), respectively, excluding amounts that may be

recognized through settlement losses. The net actuarial loss and prior

service credit for the retiree health benefit plans that will be amortized

from Accumulated other comprehensive loss into net periodic benefit

cost over the next fiscal year are $2 and $(43), respectively.

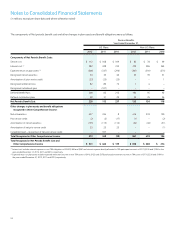

Pension plan assets consist of both defined benefit plan assets and

assets legally restricted to the TRA accounts. The combined investment

results for these plans, along with the results for our other defined

benefit plans, are shown above in the “actual return on plan assets”

caption. To the extent that investment results relate to TRA, such results

are charged directly to these accounts as a component of interest cost.

Plan Amendments

Pension Plan Freezes

Over the past several years, we have amended several of our defined

benefit pension plans to freeze current benefits and eliminate

benefits accruals for future service. In certain plans we are required

to continue to consider salary increases in determining the benefit

obligation related to prior service. The following is a discussion of these

amendments and their impact on our primary defined benefit pension

plans.

In 2011, we amended all of our primary U.S. defined benefit plans

for salaried employees. Our primary qualified plans had previously

been amended to freeze the final pay formulas within the plans as of

December 31, 2012, but a cash balance service credit was expected to

continue post December 31, 2012. The 2011 amendments fully freeze

any further benefit and service accrual after December 31, 2012 for all

of these plans, including the non-qualified plans. As a result of these

plan amendments, in 2011 we recognized a pre-tax curtailment gain of

$107 ($66 after-tax). The gain represents the recognition of deferred

gains from other prior year amendments (“Prior service credits”) as a

result of the discontinuation of any future benefit or service accrual

period. This amendment will also result in a change in amortization

period as of January 1, 2013 for actuarial gains and losses from the

average remaining service period of participants (approximately ten

years) to the average remaining life expectancy of all participants

(approximately thirty-three years) as a result of all participants being

considered inactive as of the effective date of the freeze.

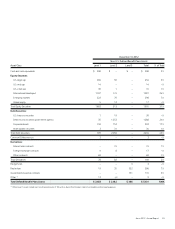

As of December 31, 2012, the aggregate accumulated actuarial losses

for our primary U.S. Defined Benefit Plans for salaried employees

amounted to $1.1 billion. This change is expected to reduce our 2013

pension expense by approximately $47. This reduction is expected

to be partially offset by an increased contribution to the U.S. defined

contribution plan as all employees have been transferred to that plan

following the freeze.

In 2011, the Canadian Salary Pension Plan was amended to close

the plan to future service accrual effective January 1, 2014. Benefits

earned up to January 1, 2014 will not be affected and participants will

continue receive the benefit of future salary increases to the extent

applicable; therefore, the amendment did not result in a material

change to the projected benefit obligation at the re-measurement date

of December 31, 2011.

In 2009, the U.K. Final Salary Pension Plan was amended to close

the plan to future service accrual effective January 1, 2014. Benefits

earned up to January 1, 2014 will not be affected and participants will

continue receive the benefit of future salary and inflation increases

to the extent applicable; therefore, the amendment does not result

in a material change to the projected benefit obligation at the re-

measurement date of December 31, 2009.

Retiree Health Plan Amendments

In 2010, we amended our domestic retiree health benefit plan to

eliminate the use of the Retiree Drug Subsidy that the Company

receives from Medicare as an offset to retiree contributions. This

amendment was effective January 1, 2011. The Company instead

decided to use this subsidy to reduce its retiree healthcare costs. The

amendment resulted in a net decrease of $55 to the retiree medical

benefit obligation and a corresponding $34 after tax increase to equity.

This amendment reduced both the 2012 and 2011 retiree-health

expenses by approximately $13.