Xerox 2012 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2012 Xerox annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

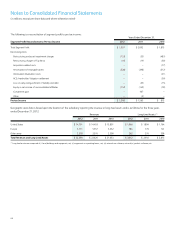

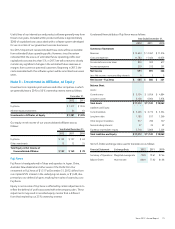

Notes to Consolidated Financial Statements

(in millions, except per-share data and where otherwise noted)

72

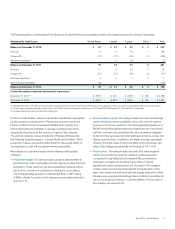

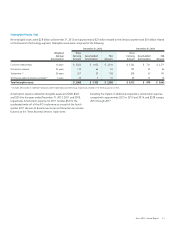

to wholly-owned consolidated bankruptcy-remote limited purpose

subsidiaries which in turn sold the principal and interest portions of

such contracts to the third-party financial institution (the “ultimate

purchaser”). As of December 31, 2012, the net carrying value of the

receivables sold and derecognized from our balance sheet was $647.

A pre-tax gain of $44 was recognized on these sales and is net of fees

and expenses of approximately $5. The gain was reported in Finance

income in Document Technology segment revenues. We continue to

service the sold receivables for which we receive a 1% servicing fee. We

have concluded that the 1% servicing fee (approximately $12 over the

expected life of the associated receivables) is adequate compensation

and, accordingly, no servicing asset or liability was recorded.

The beneficial interests represent our right to receive future cash flows

from the sold receivables which exceed the ultimate purchaser’s initial

investment and associated return on that investment as well as the

servicing fee. The beneficial interests were initially recognized at an

estimate of fair value based on the present value of the expected

future cash flows. The present value of the expected future cash flows

was calculated using management’s best estimate of key assumptions

including credit losses, prepayment rates and an appropriate risk-

adjusted discount rate (all unobservable Level 3 inputs) for which we

utilized annualized rates of approximately 2.1%, 9.3% and 10.0%,

respectively. These assumptions are supported by both our historical

experience and anticipated trends relative to the particular portfolios

of receivables sold. However, to assess the sensitivity on the fair value

of the beneficial interests, we adjusted the credit loss rate, prepayment

rate and discount rate assumptions individually by 10% and 20%

while holding the other assumptions constant. Although the effect of

multiple assumption changes was not considered in this analysis, a

10% or 20% adverse variation in any one of these three individual

assumptions would each decrease the recorded beneficial interests by

approximately $4 or less.

The ultimate purchaser has no recourse to our other assets for the

failure of customers to pay principal and interest when due beyond our

beneficial interests of which $35 and $68 is included in “Other current

assets” and “Other long-term assets,” respectively, in the accompanying

Consolidated Balance Sheets at December 31, 2012. The beneficial

interests are held by the bankruptcy-remote subsidiaries and therefore

are not available to satisfy any of our creditor obligations. We will

report collections on the beneficial interests as operating cash flows in

the Consolidated Statements of Cash Flows because such beneficial

interests are the result of an operating activity and the associated

interest rate risk is de minimis considering their weighted average lives

of less than 2 years.

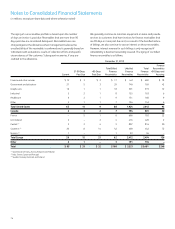

Allowance for Credit Losses and Credit Quality

Our finance receivable portfolios are primarily in the U.S., Canada and

Western Europe. We generally establish customer credit limits and

estimate the allowance for credit losses on a country or geographic

basis. We establish credit limits based upon an initial evaluation of the

customer’s credit quality and adjust that limit accordingly based upon

ongoing credit assessments of the customer, including payment history

and changes in credit quality.

The allowance for doubtful accounts and provision for credit losses

represents an estimate of the losses expected to be incurred from the

Company’s finance receivable portfolio. The level of the allowance is

determined on a collective basis by applying projected loss rates to our

different portfolios by country, which represent our portfolio segments.

This is the level at which we develop and document our methodology

to determine the allowance for credit losses. This loss rate is primarily

based upon historical loss experiences adjusted for judgments about

the probable effects of relevant observable data including current

economic conditions as well as delinquency trends, resolution rates, the

aging of receivables, credit quality indicators and the financial health of

specific customer classes or groups. The allowance for doubtful finance

receivables is inherently more difficult to estimate than the allowance

for trade accounts receivable because the underlying lease portfolio has

an average maturity, at any time, of approximately two to three years

and contains past due billed amounts, as well as unbilled amounts. We

consider all available information in our quarterly assessments of the

adequacy of the allowance for doubtful accounts. The identification

of account-specific exposure is not a significant factor in establishing

the allowance for doubtful finance receivables. Our policy and

methodology used to establish our allowance for doubtful accounts has

been consistently applied over all periods presented.

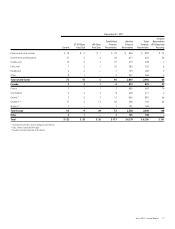

Since our allowance for doubtful finance receivables is determined

by country, the risk characteristics in our finance receivable portfolio

segments will generally be consistent with the risk factors associated

with the economies of those countries/regions. Loss rates declined in

both the U.S. and Canada reflecting the effects of improved collections

in those countries during 2011 and 2012. Since Europe is comprised

of various countries and regional economies, the risk profile within

our European portfolio segment is somewhat more diversified due to

the varying economic conditions among the countries. Charge-offs

in Europe were flat in 2012 as compared to the prior year’s, reflecting

a stabilization of the credit issues noted in 2011. Loss rates peaked in

2011 as a result of the European economic challenges particularly for

those countries in the southern region.