Xerox 2012 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2012 Xerox annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

65Xerox 2012 Annual Report

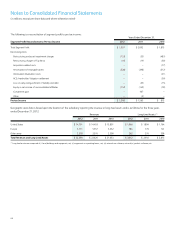

Goodwill and Other Intangible Assets

Goodwill represents the excess of the purchase price over the fair value

of acquired net assets in a business combination, including the amount

assigned to identifiable intangible assets. The primary drivers that

generate goodwill are the value of synergies between the acquired

entities and the company and the acquired assembled workforce,

neither of which qualifies as an identifiable intangible asset. Goodwill

is not amortized but rather is tested for impairment annually or more

frequently if an event or circumstance indicates that an impairment

loss may have been incurred.

Impairment testing for goodwill is done at the reporting unit level.

A reporting unit is an operating segment or one level below an

operating segment (a “component”) if the component constitutes

a business for which discrete financial information is available, and

segment management regularly reviews the operating results of that

component.

When testing goodwill for impairment, we may assess qualitative

factors for some or all of our reporting units to determine whether it

is more likely than not (that is, a likelihood of more than 50 percent)

that the fair value of a reporting unit is less than its carrying amount,

including goodwill. Alternatively, we may bypass this qualitative

assessment for some or all of our reporting units and perform a

detailed quantitative test of impairment (Step 1). If we perform the

detailed quantitative impairment test and the carrying amount of the

reporting unit exceeds its fair value, we would perform an analysis (Step

2) to measure such impairment. In 2012, we elected to proceed to the

quantitative assessment of the recoverability of our goodwill balances

for each of our reporting units in performing our annual impairment

test. Based on our quantitative assessments, we concluded that the fair

values of each of our reporting units exceeded their carrying values and

no impairments were identified.

Other intangible assets primarily consist of assets obtained in

connection with business acquisitions, including installed customer

base and distribution network relationships, patents on existing

technology and trademarks. We apply an impairment evaluation

whenever events or changes in business circumstances indicate that

the carrying value of our intangible assets may not be recoverable.

Other intangible assets are amortized on a straight-line basis over their

estimated economic lives. We believe that the straight-line method

of amortization reflects an appropriate allocation of the cost of the

intangible assets to earnings in proportion to the amount of economic

benefits obtained annually by the Company.

Refer to Note 9 – Goodwill and Intangible Assets, Net for further

information.

Impairment of Long-Lived Assets

We review the recoverability of our long-lived assets, including

buildings, equipment, internal use software and other intangible assets,

when events or changes in circumstances occur that indicate that the

carrying value of the asset may not be recoverable. The assessment

of possible impairment is based on our ability to recover the carrying

value of the asset from the expected future pre-tax cash flows

(undiscounted and without interest charges) of the related operations.

If these cash flows are less than the carrying value of such asset, an

impairment loss is recognized for the difference between estimated fair

value and carrying value. Our primary measure of fair value is based on

discounted cash flows.

Pension and Post-Retirement Benefit Obligations

We sponsor defined benefit pension plans in various forms in several

countries covering employees who meet eligibility requirements. Retiree

health benefit plans cover U.S. and Canadian employees for retiree

medical costs. We employ a delayed recognition feature in measuring

the costs of pension and post-retirement benefit plans. This requires

changes in the benefit obligations and changes in the value of assets

set aside to meet those obligations to be recognized not as they occur,

but systematically and gradually over subsequent periods. All changes

are ultimately recognized as components of net periodic benefit cost,

except to the extent they may be offset by subsequent changes. At

any point, changes that have been identified and quantified but not

recognized as components of net periodic benefit cost, are recognized

in Accumulated Other Comprehensive Loss, net of tax.

Several statistical and other factors that attempt to anticipate future

events are used in calculating the expense, liability and asset values

related to our pension and retiree health benefit plans. These factors

include assumptions we make about the discount rate, expected return

on plan assets, rate of increase in healthcare costs, the rate of future

compensation increases and mortality. Actual returns on plan assets

are not immediately recognized in our income statement due to the

delayed recognition requirement. In calculating the expected return

on the plan asset component of our net periodic pension cost, we

apply our estimate of the long-term rate of return on the plan assets

that support our pension obligations, after deducting assets that are

specifically allocated to Transitional Retirement Accounts (which are

accounted for based on specific plan terms).

For purposes of determining the expected return on plan assets, we

utilize a market-related value approach in determining the value of

the pension plan assets, rather than a fair market value approach. The

primary difference between the two methods relates to systematic

recognition of changes in fair value over time (generally two years)