Xcel Energy 2002 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2002 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90

|

|

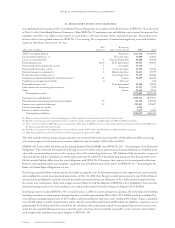

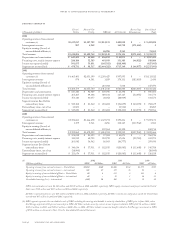

1993 to 2008. NSP-Minnesota is amortizing each installment to expense on a monthly basis. The most recent installment paid in 2002

was $4 million; future installments are subject to inflation adjustments under DOE rules. NSP-Minnesota is obtaining rate recovery of

these DOE assessments through the cost-of-energy adjustment clause as the assessments are amortized. Accordingly, we deferred the

unamortized assessment of $21 million at Dec. 31, 2002, as a regulatory asset.

Plant Decommissioning Decommissioning of NSP-Minnesota’s nuclear facilities is planned for the years 2010 through 2022, using the

prompt dismantlement method. We are currently following industry practice by ratably accruing the costs for decommissioning over the

approved cost recovery period and including the accruals in Accumulated Depreciation. Consequently, the total decommissioning cost

obligation and corresponding assets currently are not recorded in Xcel Energy’s Consolidated Financial Statements.

Monticello began operation in 1971 and is licensed to operate until 2010. Prairie Island units 1 and 2 began operation in 1973 and 1974,

respectively, and are licensed to operate until 2013 and 2014, respectively. Once a decision is made by the Minnesota Legislature regarding

interim spent fuel storage facilities, Xcel Energy will make a decision on whether to pursue license renewal for Monticello and Prairie

Island plants. Applications for license renewal must be submitted to the Nuclear Regulatory Commission (NRC) at least five years prior

to license expiration. Preliminary scoping efforts for license renewal of the Monticello plant have begun, including data collection and

review. The Prairie Island license renewal process has not yet begun. Xcel Energy’s decision whether to apply for license renewal approval

could be contingent on incremental plant maintenance or capital expenditures, recovery of which would be expected from customers

through the respective rate recovery mechanisms. Management cannot predict the specific impact of such future requirements, if any, on

its results of operations.

In 2001, the Financial Accounting Standards Board (FASB) issued SFAS No. 143 “Accounting for Asset Retirement Obligations.” This

statement will require NSP-Minnesota to record its future nuclear plant decommissioning obligations as a liability at fair value with a

corresponding increase to the carrying value of the related long-lived asset. The liability will be increased to its present value each period,

and the capitalized cost will be depreciated over the useful life of the related long-lived asset. If at the end of the asset’s useful life the

recorded liability differs from the actual obligations paid, SFAS No. 143 requires a gain or loss be recognized at that time. However, rate-

regulated entities may recognize a regulatory asset or liability instead, if the criteria for SFAS No. 71 are met. NSP-Minnesota adopted

SFAS No. 143 as required on Jan. 1, 2003. For additional information, see Note 20 to the Consolidated Financial Statements.

Consistent with cost recovery in utility customer rates, we record annual decommissioning accruals based on periodic site-specific cost

studies and a presumed level of dedicated funding. Cost studies quantify decommissioning costs in current dollars. Funding presumes that

current costs will escalate in the future at a rate of 4.35 percent per year. The total estimated decommissioning costs that will ultimately

be paid, net of income earned by external trust funds, is currently being accrued using an annuity approach over the approved plant recovery

period. This annuity approach uses an assumed rate of return on funding, which is currently 5.5 percent, net of tax, for external funding

and approximately 8 percent, net of tax, for internal funding. Unrealized gains on nuclear decommissioning investments are deferred as

Regulatory Liabilities based on the assumed offsetting against decommissioning costs in current ratemaking treatment.

The MPUC last approved NSP-Minnesota’s nuclear decommissioning study request in April 2000, using 1999 cost data. A new filing

was submitted to the MPUC in October 2002 that requests continuation of the current accrual. Since the timeframe is getting short on

the recovery of the Prairie Island costs, less than five years at the start of 2003, NSP-Minnesota has recommended that the next filing be

submitted in October 2003. The Department of Commerce has recommended that the internal fund, which is currently being transferred

to the external funds, be transferred over a shorter period of time. This proposal would increase the fund cash contribution by approximately

$13 million in 2003, but may not have a statement of operations impact. Although we expect to operate Prairie Island through the end of

each unit’s licensed life, the approved capital recovery would allow for the plant to be fully depreciated, including the accrual and recovery

of decommissioning costs, in 2007. This is about seven years earlier than each unit’s licensed life. The approved recovery period for Prairie

Island has been reduced because of the uncertainty regarding spent-fuel storage. We believe future decommissioning cost accruals will

continue to be recovered in customer rates.

The total obligation for decommissioning currently is expected to be funded 100 percent by external funds, as approved by the MPUC.

Contributions to the external fund started in 1990 and are expected to continue until plant decommissioning begins. The assets held in

trusts as of Dec. 31, 2002, primarily consisted of investments in fixed income securities, such as tax-exempt municipal bonds and U.S.

government securities that mature in one to 20 years, and common stock of public companies. We plan to reinvest matured securities

until decommissioning begins.

page 94 xcel energy inc. and subsidiaries

notes to consolidated financial statements