Pizza Hut 2010 Annual Report Download - page 152

Download and view the complete annual report

Please find page 152 of the 2010 Pizza Hut annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

|

|

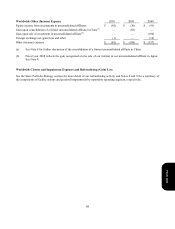

55

Impairment of Goodwill

We evaluate goodwill for impairment on an annual basis or more often if an event occurs or circumstances change that

indicates impairment might exist. Goodwill is evaluated for impairment through the comparison of fair value of our

reporting units to their carrying values. Our reporting units are our operating segments in the U.S., our YRI business units

(typically individual countries) and our China Division brands. Fair value is the price a willing buyer would pay for the

reporting unit, and is generally estimated using discounted expected future after-tax cash flows from company operations

and franchise royalties.

Future cash flow estimates and the discount rate are the key assumptions when estimating the fair value of a reporting

unit. Future cash flows are based on growth expectations relative to recent historical performance and incorporate sales

growth and margin improvement assumptions that we believe a buyer would assume when determining a purchase price

for the reporting unit. The sales growth and margin improvement assumptions that factor into the discounted cash flows

are highly correlated as cash flow growth can be achieved through various interrelated strategies such as product pricing

and restaurant productivity initiatives. The discount rate is our estimate of the required rate of return that a third-party

buyer would expect to receive when purchasing a business from us that constitutes a reporting unit. We believe the

discount rate is commensurate with the risks and uncertainty inherent in the forecasted cash flows.

The fair values of each of our reporting units were substantially in excess of their respective carrying values as of the 2010

goodwill impairment test that was performed at the beginning of the fourth quarter. However, our Pizza Hut United

Kingdom (“U.K.”) reporting unit, for which $104 million in goodwill was recorded at year end 2010, has experienced

deteriorating operating performance over the past several years as sales and profits have declined. Our forecasts of future

cash flows in determining the fair value of this reporting unit incorporate plans that have been put into place to return the

business to previous levels of profitability. These plans include specific measures to drive system sales growth, which is

the assumption that most significantly drives the cash flow expectations and resulting fair value estimations of the

reporting unit, over the next three years. While such forecasted system sales growth is higher than what we would

normally anticipate for a mature market like Pizza Hut U.K., such growth is reflective of our belief that the business has

experienced a temporary downturn and that sales declines in recent years can be recovered. If our plans to drive system

sales growth are not achieved or are not expected to be achieved, this could impact future estimations of fair value of the

Pizza Hut U.K. reporting unit and result in impairment of some or all of the Pizza Hut U.K. recorded goodwill. Likewise,

if other events, such as higher than anticipated inflation that we were unable to recover through increased sales, were to

occur that would negatively impact the outlook for the business and our resulting estimations of fair value, some or all of

the goodwill could be impaired.

When we refranchise restaurants we include goodwill in the carrying amount of the restaurants disposed of based on the

relative fair values of the portion of the reporting unit disposed of in the refranchising and the portion of the reporting unit

that will be retained. The fair value of the portion of the reporting unit disposed of in a refranchising is determined by

reference to the discounted value of the future cash flows expected to be generated by the restaurant and retained by the

franchisee, which include a deduction for the anticipated, future royalties the franchisee will pay us associated with the

franchise agreement entered into simultaneously with the refranchising transaction. Appropriate adjustments are made if

such franchise agreement is determined to not be at prevailing market rates. When determining whether such franchise

agreement is at prevailing market rates our primary consideration is consistency with the terms of our current franchise

agreements both within the country that the restaurants are being refranchised in and around the world. The Company

believes consistency in royalty rates as a percentage of sales is appropriate as the Company and franchisee share in the

impact of near-term fluctuations in sales results with the acknowledgment that over the long-term the royalty rate

represents an appropriate rate for both parties.

Form 10-K