OfficeMax 2005 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2005 OfficeMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

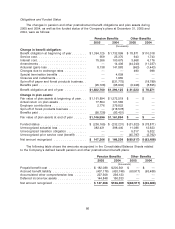

covered under the plans sponsored by the Company. The OfficeMax, Retail employees, among

others, never participated in any of the Company’s defined benefit pension plans. The Company’s

salaried pension plan was closed to new entrants on November 1, 2003, and on December 31,

2003, the benefits of eligible OfficeMax, Contract participants were frozen. Active OfficeMax,

Contract employees who were eligible to participate in the plan on December 31, 2003 were

credited with one additional year of service on January 1, 2004, at a reduced 1% crediting rate. As

a result of these actions, the Company’s future annual pension expenses and contributions will be

less than the amounts included in prior periods.

Under the terms of the Company’s plans, the pension benefit for salaried employees was

based primarily on the employees’ years of service and highest five-year average compensation.

The pension benefit for hourly employees was generally based on a fixed amount per year of

service. The Company’s general funding policy is to make contributions to the plans in amounts

that are within the limits of deductibility under current tax regulations, and not less than the

minimum contribution required by law. The Company generally uses a December 31 measurement

date for its pension plans.

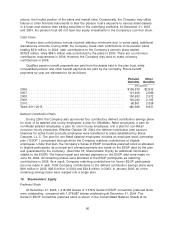

Other postretirement benefit obligations represent various retiree medical benefit plans. The

type of retiree medical benefits and the extent of coverage vary based on employee classification,

date of retirement, location, and other factors. All of the Company’s postretirement medical plans

are unfunded. The Company explicitly reserves the right to amend or terminate its retiree medical

plans at any time, subject only to constraints, if any, imposed by the terms of collective bargaining

agreements. Amendment or termination may significantly affect the amount of expense incurred.

During the third quarter of 2005, the Company made changes to its retiree medical benefit

plans that had the net effect of reducing the medical insurance subsidy provided to retirees,

including eliminating the subsidy for certain retirees. As a result of these plan changes, the

accumulated post-retirement benefit obligation was reduced by approximately $44 million. The plan

changes were considered to be a negative plan amendment, as defined in FASB Statement No.

106, ‘‘Employers’ Accounting for Postretirement Benefits Other than Pensions.’’ Accordingly, there

was no gain related to the plan changes recognized in the Consolidated Statement of Income

(Loss) for 2005. The reduction in the accumulated post-retirement benefit obligation will be

recognized ratably over the remaining life expectancy of the participants in the plans, which is

currently estimated to be approximately 12 years.

85