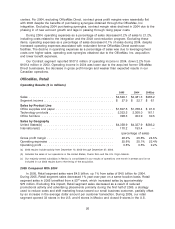

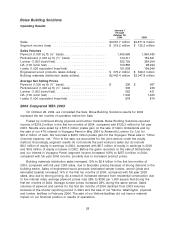

OfficeMax 2005 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2005 OfficeMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

Borrowings under the revolver bear interest at rates based on either the prime rate or the

London Interbank Offered Rate (‘‘LIBOR’’). Margins are applied to our borrowing rates and letters of

credit fees under the revolver depending on our average excess availability. Fees on letters of credit

issued under the revolver were charged at a weighted average rate of 1.125%. In addition, we are

also charged an unused line fee of .25% on the amount by which the maximum credit of

$500 million exceeds our average daily outstanding borrowings and letters of credit.

Borrowings under the revolver are secured by a lien on substantially all of our inventory and

related proceeds. The revolving loan and security agreement contains customary conditions to

borrowing including a monthly calculation of excess borrowing availability and reporting

compliance. Covenants in the revolver agreement restrict the amount of letters of credit that may be

issued, dividend distributions and other uses of cash if excess availability is less than $75 million. At

December 31, 2005, our excess availability totaled $391.7 million and we were in compliance with

all covenants under the revolver agreement. The revolver expires on June 24, 2010.

Timber Notes

In October 2004, we sold our timberlands as part of the Sale. In exchange for the timberlands,

we received installment timber notes in the amount of $1.6 billion which were credit enhanced with

guarantees. The guarantees were issued by financial institutions and were secured by the pledge of

underlying collateral notes. Subsequently, in December 2004, we completed a securitization

transaction in which we transferred our interest in the timber installment notes receivable to wholly

owned bankruptcy remote subsidiaries that were designated to be qualifying special purpose

entities (the ‘‘OMXQs’’). The OMXQs pledged the timber installment notes receivable and related

guarantees and issued securitization notes in the amount of $1.5 billion. Recourse on the

securitization notes is limited to the pledged timber notes receivable. The securitization notes are

15-year non-amortizing and were issued in two equal $735 million tranches paying interest of 5.42%

and 5.54%, respectively.

As a result of these transactions, OfficeMax received $1.5 billion in cash from the OMXQ’s, and

over 15 years will earn approximately $82.5 million per year in interest income on the timber

installment notes receivable and incur interest expense of approximately $80.5 million per year on

the securitization notes. The pledged timber installment notes receivable and nonrecourse

securitization notes will mature in 2020 and 2019, respectively. The securitization notes have an

initial term that is approximately three months shorter than the installment notes. The Company

expects to refinance its ownership of the installment notes in 2019 with a short-term secured

borrowing to bridge the period from initial maturity of the securitization notes to the maturity of the

installment notes.

The guidance related to the accounting for securitization transactions is complex and open to

interpretation. The original entities issuing the credit enhanced timber installment notes to OfficeMax

are variable-interest entities (the ‘‘VIE’s’’) under FASB Interpretation No. 46R, ‘‘Consolidation of

Variable Interest Entities.’’ The holders of the timber installment notes (the OMXQ’s) are considered

to be the primary beneficiaries, and therefore, the VIE’s are required to be consolidated with the

OMXQs, which are also the issuers of the securitization notes. Although we believe an argument

can be made that the consolidation of the VIE’s as a result of this transaction does not disqualify

the OMXQs from being qualified special purpose entities, as described in FASB Statement No 140,

‘‘Accounting for Transfers and Servicing of Financial Assets and Extinguishments of Liabilities,’’ we

have concluded that consolidating the VIE’s does disqualify the OMXQs from meeting this

guidance. As a result, the accounts of the OMXQs have been consolidated into our financial

statements. The effect of our consolidation of the OMXQs is that the securitization transaction is

treated as a financing, and both the timber notes receivable and the securitization notes payable

are reflected in our Consolidated Balance Sheet.

36