OfficeMax 2005 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2005 OfficeMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

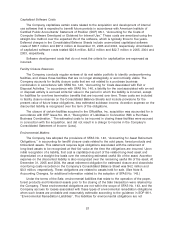

Capitalized Software Costs

The Company capitalizes certain costs related to the acquisition and development of internal

use software that is expected to benefit future periods in accordance with American Institute of

Certified Public Accountants’ Statement of Position (SOP) 98-1, ‘‘Accounting for the Costs of

Computer Software Developed or Obtained for Internal Use.’’ These costs are amortized using the

straight-line method over the expected life of the software, which is typically three to five years.

Deferred charges in the Consolidated Balance Sheets include unamortized capitalized software

costs of $36.7 million and $57.3 million at December 31, 2005 and 2004, respectively. Amortization

of capitalized software costs totaled $25.6 million, $25.2 million and $22.7 million in 2005, 2004 and

2003, respectively.

Software development costs that do not meet the criteria for capitalization are expensed as

incurred.

Facility Closure Reserves

The Company conducts regular reviews of its real estate portfolio to identify underperforming

facilities, and closes those facilities that are no longer strategically or economically viable. The

Company accounts for facility closure costs that are not related to a purchase business

combination in accordance with SFAS No. 146, ‘‘Accounting for Costs Associated with Exit or

Disposal Activities.’’ In accordance with SFAS No. 146, a liability for the cost associated with an exit

or disposal activity is accrued at its fair value in the period in which the liability is incurred, except

for liabilities for one-time termination benefits that are incurred over time. These costs are included

in facility closure reserves on the Consolidated Balance Sheets and include provisions for the

present value of future lease obligations, less estimated sublease income. Accretion expense on the

discounted liability is recognized over the term of the obligations.

The closure of certain facilities acquired in the OfficeMax, Inc. acquisition was accounted for in

accordance with EITF Issue No. 95-3, ‘‘Recognition of Liabilities in Connection With a Purchase

Business Combination.’’ The estimated costs to be incurred in closing these facilities were accrued

in connection with the acquisition, and did not result in a charge to income in the Company’s

Consolidated Statement of Income (Loss).

Environmental Matters

The Company has adopted the provisions of SFAS No. 143, ‘‘Accounting for Asset Retirement

Obligations,’’ in accounting for landfill closure costs related to the sold paper, forest products and

timberland assets. This statement requires legal obligations associated with the retirement of

long-lived assets to be recognized at their fair value at the time the obligations are incurred. Upon

initial recognition of a liability, that cost is capitalized as part of the related long-lived asset and

depreciated on a straight-line basis over the remaining estimated useful life of the asset. Accretion

expense on the discounted liability is also recognized over the remaining useful life of the asset. At

December 31, 2005 and 2004, the asset retirement obligation for estimated closure and closed-site

monitoring costs recorded on the Company’s Consolidated Balance Sheet was $4.2 million and

$0.3 million, respectively. These obligations are related to assets held for sale. (See Note 8,

Accounting Changes, for additional information related to the adoption of SFAS No. 143.)

Under the terms of the Sale, environmental liabilities that relate to the operation of the paper,

forest products and timberland assets prior to the closing of the Sale transaction were retained by

the Company. These environmental obligations are not within the scope of SFAS No. 143, and the

Company accrues for losses associated with these types of environmental remediation obligations

when such losses are probable and reasonably estimable according to the guidance in SOP 96-1,

‘‘Environmental Remediation Liabilities’’. The liabilities for environmental obligations are not

57