OfficeMax 2005 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2005 OfficeMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

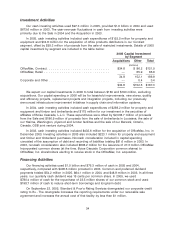

Note Agreements

In August 2003, we issued $50 million of 7.45% medium-term notes due in 2011. The proceeds

of the notes were used for general corporate purposes. On November 5, 2004, we purchased

$49.6 million of these notes pursuant to a tender offer for these securities.

In October 2003, we issued $300 million of 6.50% senior notes due in 2010 and $200 million of

7.00% senior notes due in 2013. Net proceeds from the senior notes were used to repay

borrowings under our revolving credit agreement, to provide cash for the OfficeMax, Inc. transaction

and for other general corporate purposes. At the time of issuance, the senior note indentures

contained a number of restrictive covenants, substantially all of which have been eliminated through

the execution of supplemental indentures and replaced with covenants found in the base indentures

that are applicable to our medium term notes and other public debt. Those covenants include a

limitation on mergers and similar transactions, a restriction on secured transactions involving

Principal Properties, as defined, and a restriction on sale and leaseback transactions involving

Principal Properties. On November 5, 2004, we repurchased approximately $286.3 million of the

6.50% senior notes and received the requisite consents to adopt amendments to the indenture

pursuant to a tender offer for these securities. As a result, the Company and the trustee executed a

Sixth Supplemental Indenture which eliminated substantially all of the restrictive covenants, certain

events of default and related provisions, and replaced them with the covenants from our other

public debt.

On December 23, 2004, both Moody’s Investors Service, Inc., and Standard & Poor’s Rating

Services upgraded the credit rating on our 7.00% senior notes to investment grade. The upgrades

were the result of actions the Company undertook to collateralize the notes by granting the

noteholders a security interest in $113 million in principal amount of General Electric Capital and

Bank of America Corp. notes maturing in 2008 (the ‘‘pledged instruments’’). These pledged

instruments are reflected as ‘‘Restricted investments’’ on our Consolidated Balance Sheets. As a

result of these ratings upgrades, the original 7.00% senior note covenants were replaced with the

covenants found in our other public debt. During 2005, we purchased and cancelled $87.3 million

of the 7.00% senior notes. As a result, $92.8 million of the pledged instruments were released from

the security interest granted to the 7.00% note holders and were sold in 2005. The remaining

balance of these pledged instruments continue to be subject to the security interest, and are

reflected as ‘‘Restricted Investments’’ in our Consolidated Balance Sheet at December 31, 2005.

Adjustable Conversion-Rate Equity Securities (ACES)

In December 2001, we issued 3,450,000 7.50% adjustable conversion-rate equity security units

(ACES) to the public at an aggregate offering price of $172.5 million. The units traded on the New

York Stock Exchange under the ticker symbol BEP. At the time of issuance, there were two

components of each unit. Investors received a preferred security issued by Boise Cascade Trust I

(the ‘‘Trust’’), a statutory business trust whose common securities were owned by the Company,

with a liquidation amount of $50. These preferred securities were mandatorily redeemable in

December 2006. Investors also entered into a contract to purchase $50 of common shares of the

Company, subject to a collar arrangement. The Trust used the proceeds from the offering to

purchase debentures issued by Boise Cascade Corporation (now OfficeMax Incorporated). These

debentures were 7.50% senior, unsecured obligations and had a scheduled maturity in

December 2006.

On September 16, 2004, we dissolved the Trust and distributed the debentures to the unit

holders in exchange for their preferred securities. Also on that date, the remarketing of

$144.5 million of these debentures was completed. In connection with the remarketing, the 7.50%

interest rate on the debentures was reset to 2.75% over the average of the interbank offered rates

37