Kroger 2015 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2015 Kroger annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

|

|

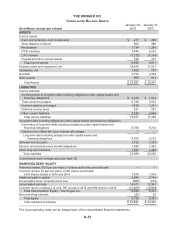

A-21

$1.8 billion, after-tax, which includes Roundy’s share of underfunding of its multi-employer plans. This

represents an increase in the estimated amount of underfunding of approximately $1.1 billion, pre-tax,

or approximately $680 million, after-tax, as of December 31, 2015, compared to December 31, 2014.

The increase in the amount of underfunding is attributable to lower than expected returns on the assets

held in the multi-employer plans during 2015, changes in mortality rate assumptions and the merger

of Roundy’s. Our estimate is based on the most current information available to us including actuarial

evaluations and other data (that include the estimates of others), and such information may be outdated

or otherwise unreliable.

We have made and disclosed this estimate not because, except as noted above, this underfunding

is a direct liability of ours. Rather, we believe the underfunding is likely to have important consequences.

In 2016, we expect to contribute approximately $260 million to multi-employer pension plans, subject

to collective bargaining and capital market conditions. We expect increases in expense as a result of

increases in multi-employer pension plan contributions over the next few years. Finally, underfunding

means that, in the event we were to exit certain markets or otherwise cease making contributions to

these funds, we could trigger a substantial withdrawal liability. Any adjustment for withdrawal liability will

be recorded when it is probable that a liability exists and can be reasonably estimated, in accordance

with GAAP.

The amount of underfunding described above is an estimate and could change based on contract

negotiations, returns on the assets held in the multi-employer plans and benefit payments. The amount

could decline, and our future expense would be favorably affected, if the values of the assets held in

the trust significantly increase or if further changes occur through collective bargaining, trustee action

or favorable legislation. On the other hand, our share of the underfunding could increase and our future

expense could be adversely affected if the asset values decline, if employers currently contributing

to these funds cease participation or if changes occur through collective bargaining, trustee action or

adverse legislation. We continue to evaluate our potential exposure to under-funded multi-employer

pension plans. Although these liabilities are not a direct obligation or liability of ours, any commitments

to fund certain multi-employer plans will be expensed when our commitment is probable and an estimate

can be made.

See Note 16 to the Consolidated Financial Statements for more information relating to our

participation in these multi-employer pension plans.

Uncertain Tax Positions

We review the tax positions taken or expected to be taken on tax returns to determine whether and

to what extent a benefit can be recognized in our Consolidated Financial Statements. Refer to Note 5 to

the Consolidated Financial Statements for the amount of unrecognized tax benefits and other disclosures

related to uncertain tax positions.

Various taxing authorities periodically audit our income tax returns. These audits include questions

regarding our tax filing positions, including the timing and amount of deductions and the allocation of

income to various tax jurisdictions. In evaluating the exposures connected with these various tax filing

positions, including state and local taxes, we record allowances for probable exposures. A number of

years may elapse before a particular matter, for which an allowance has been established, is audited and

fully resolved. As of January 30, 2016, the Internal Revenue Service had concluded its examination of

our 2010 and 2011 federal tax returns. Tax years 2012 and 2013 remain under examination.

The assessment of our tax position relies on the judgment of management to estimate the

exposures associated with our various filing positions.

Share-Based Compensation Expense

We account for stock options under the fair value recognition provisions of GAAP. Under this method,

we recognize compensation expense for all share-based payments granted. We recognize share-based

compensation expense, net of an estimated forfeiture rate, over the requisite service period of the award. In

addition, we record expense for restricted stock awards in an amount equal to the fair market value of the

underlying stock on the grant date of the award, over the period the award restrictions lapse.