Kroger 2015 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2015 Kroger annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

|

|

50

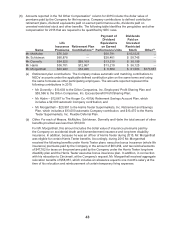

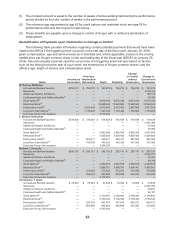

Offsetting Benefits

Mr. Donnelly also participates in the Dillon Companies, Inc. Employees’ Profit Sharing Plan, which

is a qualified defined contribution plan (the “Dillon Profit Sharing Plan”) under which Dillon Companies,

Inc. and its participating subsidiaries may choose to make discretionary contributions each year that are

allocated to each participant’s account. Participation in Dillon Profit Sharing Plan was frozen in 2001

and participants are no longer able to make employee contributions, but certain participants, including

Mr. Donnelly, are still eligible for employer contributions. Participants elect from among a number of

investment options and the amounts in their accounts are invested and credited with investment earnings

in accordance with their elections. Due to offset formulas contained in the Kroger Pension Plan, Mr.

Donnelly’s accrued benefits under the Dillon Profit Sharing Plan offset a portion of the benefit that would

otherwise accrue for him under the Kroger Pension for his service with Dillon Companies, Inc. This offset

is reflected in the table above.

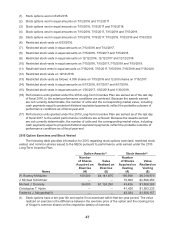

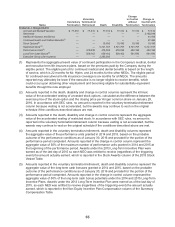

Harris Teeter Pension Plan

Mr. Morganthall participates in the HT Pension Plan, which is a defined benefit pension plan.

Participation in the HT Pension Plan was frozen effective October 1, 2005. For participants with age and

service points as of December 31, 2005 equal to or greater than 45, which includes Mr. Morganthall,

benefit accruals under the HT Pension Plan after September 30, 2005 will be offset by the actuarial

equivalent of the portion of their account balance under the Harris Teeter Supermarkets, Inc. Retirement

and Savings Plan (the “HT Savings Plan”) that are attributable to automatic retirement contributions

made by Harris Teeter after September 30, 2005, plus earnings and losses on such contributions. A

participant’s normal annual retirement benefit under the HT Pension Plan at age 65 is an amount equal

to 0.8% of his final average earnings multiplied by years of service at retirement, plus 0.6% of his final

average earnings in excess of Social Security covered compensation multiplied by the number of years

of service up to a maximum of 35 years. A participant’s final average earnings is the average annual

cash compensation paid to the participant during the plan year, including salary, incentive compensation

and any amount contributed to the HT Savings Plan, for the 5 consecutive years in the last 10 years that

produce the highest average.

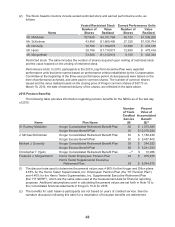

Harris Teeter SERP

Mr. Morganthall also participates in the HT SERP, which is a nonqualified deferred compensation

plan as defined in Section 409A of the Internal Revenue Code. The purpose of the HT SERP is to

supplement the benefits payable under the retirement plans. Under the HT SERP, participants who

retire at normal retirement age of 60 receive monthly retirement benefits equal to between 55% and

60% of his final average earnings times his accrual fraction and reduced by his (1) assumed HT Pension

Plan retirement benefit, and (2) assumed Social Security benefit. The final average earnings are the

average annual earnings during the highest 3 calendar years out of the last 10 calendar years preceding

termination of employment. The accrual fraction is a fraction, the numerator of which is the years of

credited service, the denominator of which is 20, and which may not exceed 1.0. The benefits payable

under the HT SERP are payable for the participant’s lifetime with an automatic 75% survivor benefit

payable to the participant’s surviving eligible spouse for his or her lifetime. Mr. Morganthall is eligible to

receive the full benefit as he has reached age 60. Harris Teeter uses a non-qualified trust to purchase

and hold the assets to satisfy Harris Teeter’s obligation under the HT SERP, and participants in the HT

SERP are general creditors of Harris Teeter in the event Harris Teeter becomes insolvent.