IBM 2006 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2006 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

Black

MAC

CG10

of a computer system that PSI says is compatible with IBM’s S/390 and

System z architectures. IBM also sought a declaratory judgment that

its refusal to license its patents to PSI and certain of its software for use

on PSI systems does not violate the antitrust laws. IBM seeks damages

and injunctive relief. On January 19, 2007, PSI answered the complaint

and asserted counterclaims against IBM for alleged monopolization and

attempted monopolization, tying, violations of New York and California

statutes proscribing unfair competition, tortious interference with the

acquisition of PSI by a third party and promissory estoppel. PSI also

sought declaratory judgments of noninfringement of IBM’s patents

and patent invalidity. The court has not yet set a trial date.

In October 2003, a purported collective action lawsuit was filed

against IBM in the United States District Court for the Northern

District of California by ten former IBM employees alleging, on behalf

of themselves and allegedly similarly situated former employees, that

the company engaged in a pattern and practice of discriminating

against employees on the basis of age when it terminated employees

in connection with reductions in force. Initially, the District Court

dismissed the lawsuit on the basis of release agreements signed by all

the plaintiffs. On appeal, the Ninth Circuit reversed the trial court’s

finding that the release barred these claims, and in January 2007 after

denial of IBM’s petition for rehearing, the matter was returned to the

trial court for further proceedings.

The company is party to, or otherwise involved in, proceedings

brought by U.S. federal or state environmental agencies under the

Comprehensive Environmental Response, Compensation and Liability

Act (CERCLA), known as “Superfund,” or laws similar to CERCLA.

Such statutes require potentially responsible parties to participate in

remediation activities regardless of fault or ownership of sites. The

company is also conducting environmental investigations or remedia-

tions at or in the vicinity of several current or former operating sites

pursuant to permits, administrative orders or agreements with state

environmental agencies, and is involved in lawsuits and claims con-

cerning certain current or former operating sites.

The company is also subject to ongoing tax examinations and gov-

ernmental assessments in various jurisdictions. Similar to many other

U.S. companies doing business in Brazil, the company is involved in

various challenges with Brazilian authorities regarding non-income

tax assessments and non-income tax litigation matters. These matters

principally relate to claims for taxes on the importation of computer

software. The total amounts related to these matters are approxi-

mately $1.5 billion, including amounts currently in litigation and

other amounts. The company believes it will prevail on these matters

and that these amounts are not meaningful indicators of liability.

In accordance with SFAS No. 5, “Accounting for Contingencies,”

(SFAS No. 5), the company records a provision with respect to a claim,

suit, investigation or proceeding when it is probable that a liability has

been incurred and the amount of the loss can be reasonably estimated.

Any provisions are reviewed at least quarterly and are adjusted to reflect

the impact and status of settlements, rulings, advice of counsel and

other information pertinent to a particular matter. Any recorded liabil-

ities for the above items, including any changes to such liabilities for the

year ended December 31, 2006, were not material to the Consolidated

Financial Statements. Based on its experience, the company believes

that the damage amounts claimed in the matters referred to above are

not a meaningful indicator of the potential liability. Claims, suits,

investigations and proceedings are inherently uncertain and it is not

possible to predict the ultimate outcome of the matters previously

discussed. While the company will continue to defend itself vigorously

in all such matters, it is possible that the company’s business, financial

condition, results of operations or cash flows could be affected in any

particular period by the resolution of one or more of these matters.

Whether any losses, damages or remedies finally determined in any

such claim, suit, investigation or proceeding could reasonably have a

material effect on the company’s business, financial condition, results

of operations or cash flow will depend on a number of variables, includ-

ing the timing and amount of such losses or damages; the structure

and type of any such remedies; the significance of the impact any such

losses, damages or remedies may have on the company’s Consolidated

Financial Statements; and the unique facts and circumstances of the

particular matter which may give rise to additional factors.

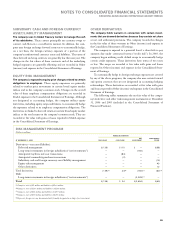

COMMITMENTS

The company’s extended lines of credit to third-party entities

include unused amounts of $2,895 million and $3,019 million at

December 31, 2006 and 2005, respectively. A portion of these amounts

was available to the company’s business partners to support their

working capital needs. In addition, the company has committed to

provide future financing to its clients in connection with client pur-

chase agreements for approximately $2,496 million and $2,155 million

at December 31, 2006 and 2005, respectively. The change over the

prior year is due to increased signings of long-term IT infrastructure

arrangements in which financing is committed by the company to

fund a client’s future purchases from the company.

The company has applied the provisions of FIN 45 to its agree-

ments that contain guarantee or indemnification clauses. These provi-

sions expand those required by SFAS No. 5, by requiring a guarantor to

recognize and disclose certain types of guarantees, even if the likelihood

of requiring the guarantor’s performance is remote. The following is

a description of arrangements in which the company is the guarantor.

The company is a party to a variety of agreements pursuant to

which it may be obligated to indemnify the other party with respect

to certain matters. Typically, these obligations arise in the context of

contracts entered into by the company, under which the company

customarily agrees to hold the other party harmless against losses aris-

ing from a breach of representations and covenants related to such

matters as title to assets sold, certain IP rights, specified environmen-

tal matters, third-party performance of non-financial contractual

obligations and certain income taxes. In each of these circumstances,

payment by the company is conditioned on the other party making a

claim pursuant to the procedures specified in the particular contract,

which procedures typically allow the company to challenge the other

party’s claims. Further, the company’s obligations under these agree-

ments may be limited in terms of time and/or amount, and in some

instances, the company may have recourse against third parties for

certain payments made by the company.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

INTERNATIONAL BUSINESS MACHINES CORPORATION AND SUBSIDIARY COMPANIES

91