IBM 2006 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2006 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

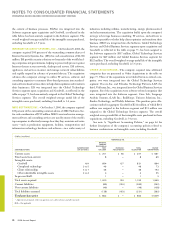

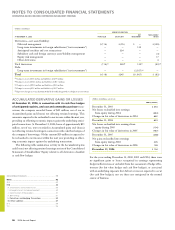

As a result of the company’s use of derivative instruments, the

company is exposed to the risk that counterparties to derivative con-

tracts will fail to meet their contractual obligations. To mitigate the

counterparty credit risk, the company has a policy of only entering

into contracts with carefully selected major financial institutions

based upon their credit ratings and other factors, and maintains strict

dollar and term limits that correspond to the institution’s credit rating.

The company’s established policies and procedures for mitigating

credit risk on principal transactions include reviewing and establishing

limits for credit exposure and continually assessing the creditworthi-

ness of counterparties. Master agreements with counterparties include

master netting arrangements as further mitigation of credit exposure

to counterparties. These arrangements permit the company to net

amounts due from the company to a counterparty with amounts due

to the company from a counterparty reducing the maximum loss from

credit risk in the event of counterparty default.

In its hedging programs, the company uses forward contracts,

futures contracts, interest-rate swaps, currency swaps and options

depending upon the underlying exposure. The company does not use

derivatives for trading or speculative purposes, nor is it a party to

leveraged derivatives.

A brief description of the major hedging programs follows.

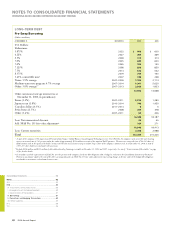

DEBT RISK MANAGEMENT

The company issues debt in the global capital markets, principally

to fund its financing lease and loan portfolio. Access to cost-effec-

tive financing can result in interest rate and/or currency mismatches

with the underlying assets. To manage these mismatches and to

reduce overall interest cost, the company uses interest-rate swaps to

convert specific fixed-rate debt issuances into variable-rate debt (i.e.,

fair value hedges) and to convert specific variable-rate debt issuances

into fixed-rate debt (i.e., cash flow hedges). The resulting cost of

funds is lower than that which would have been available if debt with

matching characteristics was issued directly. At December 31, 2006,

the weighted-average remaining maturity of all swaps in the debt risk

management program was approximately three years, as compared to

approximately four years at December 31, 2005.

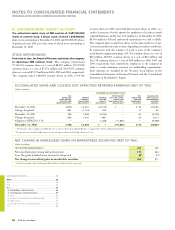

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

INTERNATIONAL BUSINESS MACHINES CORPORATION AND SUBSIDIARY COMPANIES

84 2006 Annual Report

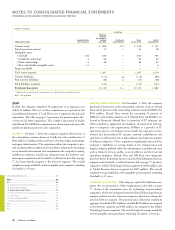

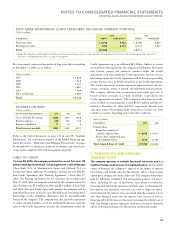

LONG-TERM INVESTMENTS IN FOREIGN

SUBSIDIARIES (NET INVESTMENT)

A significant portion of the company’s foreign currency denomi-

nated debt portfolio is designated as a hedge of net investment to

reduce the volatility in stockholders’ equity caused by changes in for-

eign currency exchange rates in the functional currency of major for-

eign subsidiaries with respect to the U.S. dollar. The company also

uses currency swaps and foreign exchange forward contracts for this

risk management purpose. The currency effects of these hedges

(approximately $350 million losses in 2006, $570 million gains in 2005

and $156 million losses in 2004, net of tax) were reflected in the

Accumulated gains and (losses) not affecting retained earnings section

of the Consolidated Statement of Stockholders’ Equity, thereby offset-

ting a portion of the translation adjustment of the applicable foreign

subsidiaries’ net assets.

ANTICIPATED ROYALTIES AND

COST TRANSACTIONS

The company’s operations generate significant nonfunctional cur-

rency, third-party vendor payments and intercompany payments

for royalties and goods and services among the company’s non-U.S.

subsidiaries and with the parent company. In anticipation of these

foreign currency cash flows and in view of the volatility of the currency

markets, the company selectively employs foreign exchange forward

and option contracts to manage its currency risk. Currently, these cash

flow hedges have maturities of one year or less, however, from time to

time can extend beyond one year commensurate with the underlying

hedged anticipated cash flows. At December 31, 2006, the weighted-

average remaining maturity of these derivative instruments was 216

days, as compared to 240 days at December 31, 2005.

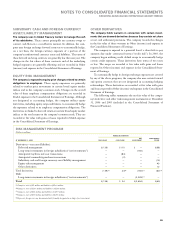

ANTICIPATED COMMODITY

PURCHASE TRANSACTIONS

In connection with the purchase of electricity for anticipated

manufacturing requirements, the company selectively employs

forward contracts to manage its price risk. Currently, these cash flow

hedges have maturities of one year or less, however, from time to time

could extend beyond one year commensurate with the underlying

hedged anticipated cash flows. At December 31, 2006, the weighted-

average remaining maturity of these derivative instruments was

approximately seven months. This risk management program was

implemented in 2006.

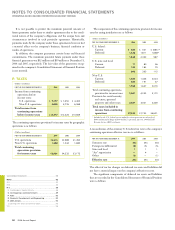

Consolidated Statements .........................................................

Notes .....................................................................................

A-G ......................................................................................... 62

H-M .........................................................................................

H. Investments and Sundry Assets ......................................

I. Intangible Assets Including Goodwill ...............................

J. Securitization of Receivables ...........................................

K. Borrowings .......................................................................

L. Derivatives and Hedging Transactions ............................

M. Other Liabilities ...............................................................

N-S ..........................................................................................

T-X ..........................................................................................

Black

MAC

390 CG10