IBM 2006 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2006 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

MANAGEMENT DISCUSSION

INTERNATIONAL BUSINESS MACHIN ES CORPORATION AND SUBSI DIARY COMPANIES

45

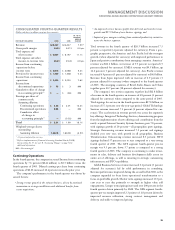

Contractual Obligations

(Dollars in millions)

TOTAL

CONTRACTUAL PAYMENTS DUE IN

PAYMENT STREAM 2007 2008-09 2010-11 AFTER 2011

Long-term debt obligations $, $, $, $, $,

Capital (finance) lease obligations

Operating lease obligations , , , ,

Purchase obligations ,

Other long-term liabilities:

Minimum pension funding (mandated)* , , , —

Executive compensation

Long-term termination benefits , ,

Other

Total $, $, $, $, $,

* These amounts represent future pension contributions that are mandated by local regulations or statute for retirees receiving pension benefits. They are all associated with non-U.S.

pension plans. The projected payments beyond 2011 are not currently determinable. See note V, “Retirement-Related Benefits,” on pages 100 to 111 for additional information on the

non-U.S. plans’ investment strategies and expected contributions and for information regarding the company’s unfunded pension liability of $14,543 million at December 31, 2006.

Total contractual payments are reported in the table above excluding the

effects of time value and therefore, may not equal the amounts reported

in the company’s Consolidated Statement of Financial Position.

Purchase obligations include all commitments to purchase goods

or services of either a fixed or minimum quantity that meet any of the

following criteria: (1) they are noncancelable, (2) the company would

incur a penalty if the agreement was canceled, or (3) the company

must make specified minimum payments even if it does not take deliv-

ery of the contracted products or services (“take-or-pay”). If the

obligation to purchase goods or services is noncancelable, the entire

value of the contract is included in the table above. If the obligation

is cancelable, but the company would incur a penalty if canceled, the

dollar amount of the penalty is included as a purchase obligation.

Contracted minimum amounts specified in take-or-pay contracts are

also included in the table as they represent the portion of each con-

tract that is a firm commitment.

In the ordinary course of business, the company enters into con-

tracts that specify that the company will purchase all or a portion of

its requirements of a specific product, commodity or service from a

supplier or vendor. These contracts are generally entered into in

order to secure pricing or other negotiated terms. They do not specify

fixed or minimum quantities to be purchased and, therefore, the com-

pany does not consider them to be purchase obligations.

Off-Balance Sheet Arrangements

In the ordinary course of business, the company entered into off-bal-

ance sheet arrangements as defined by the SEC Financial Reporting

Release 67 (FRR-67), “Disclosure in Management’s Discussion and

Analysis about Off-Balance Sheet Arrangements and Aggregate

Contractual Obligations.”

None of these off-balance sheet arrangements either has, or is

reasonably likely to have, a material current or future effect on finan-

cial condition, changes in financial condition, revenues or expenses,

results of operations, liquidity, capital expenditures or capital resources.

See the table above for the company’s contractual obligations and

note O, “Contingencies and Commitments,” on pages 91 and 92, for

detailed information about the company’s guarantees, financial com-

mitments and indemnification arrangements. The company does not

have retained interests in assets transferred to unconsolidated entities

(see note J, “Securitization of Receivables,” on page 81) or other mate-

rial off-balance sheet interests or instruments.

CRITICAL ACCOUNTING ESTIMATES

The application of GAAP requires the company to make estimates

and assumptions about future events that directly affect its

reported financial condition and operating performance. The account-

ing estimates and assumptions discussed in this section are those that

the company considers to be the most critical to its financial state-

ments. An accounting estimate is considered critical if both (a) the

nature of the estimates or assumptions is material due to the levels of

subjectivity and judgment involved, and (b) the impact within a rea-

sonable range of outcomes of the estimates and assumptions is material

to the company’s financial condition or operating performance. The

critical accounting estimates related to the company’s Global Financing

business are described on page 53 in the Global Financing section.

The company’s significant accounting policies are described in note

A, “Significant Accounting Policies,” on pages 62 to 71.

A quantitative sensitivity analysis is provided where that informa-

tion is reasonably available, can be reliably estimated and provides

material information to investors. The amounts used to assess sensi-

tivity (e.g., 1 percent, 5 percent, etc.) are included to allow users of

the Annual Report to understand a general direction cause and effect

of changes in the estimates and do not represent management’s pre-

dictions of variability.

Pension Assumptions

The measurement of the company’s benefit obligation to its employ-

ees and net periodic pension cost/(income) requires the use of certain

assumptions, including, among others, estimates of discount rates and

expected return on plan assets.

Black

MAC

2718 CG10