Berkshire Hathaway 2013 Annual Report Download - page 102

Download and view the complete annual report

Please find page 102 of the 2013 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

Management’s Discussion (Continued)

Interest Rate Risk (Continued)

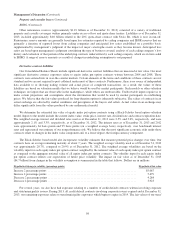

The fair values of our fixed maturity investments and notes payable and other borrowings will fluctuate in response to

changes in market interest rates. In addition, changes in interest rate assumptions used in our equity index put option contract

models cause changes in reported liabilities with respect to those contracts. Increases and decreases in interest rates generally

translate into decreases and increases in fair values of those instruments. Additionally, fair values of interest rate sensitive

instruments may be affected by the creditworthiness of the issuer, prepayment options, relative values of alternative

investments, the liquidity of the instrument and other general market conditions. The fair values of fixed interest rate

instruments may be more sensitive to interest rate changes than variable rate instruments.

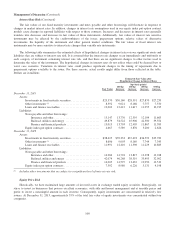

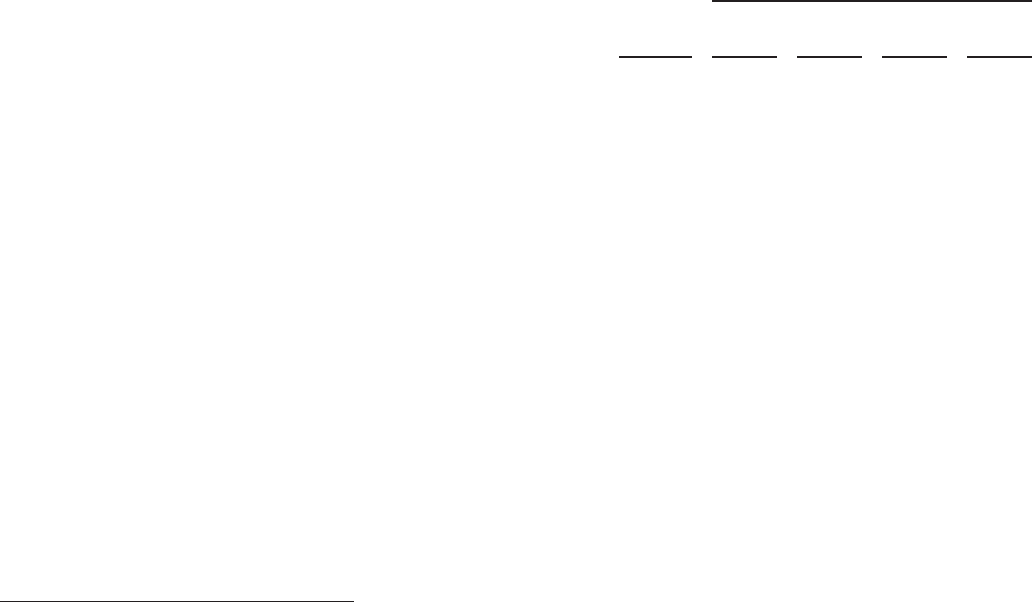

The following table summarizes the estimated effects of hypothetical changes in interest rates on our significant assets and

liabilities that are subject to interest rate risk. It is assumed that the interest rate changes occur immediately and uniformly to

each category of instrument containing interest rate risk, and that there are no significant changes to other factors used to

determine the value of the instrument. The hypothetical changes in interest rates do not reflect what could be deemed best or

worst case scenarios. Variations in interest rates could produce significant changes in the timing of repayments due to

prepayment options available to the issuer. For these reasons, actual results might differ from those reflected in the table.

Dollars are in millions.

Estimated Fair Value after

Hypothetical Change in Interest Rates

(bp=basis points)

Fair Value

100 bp

decrease

100 bp

increase

200 bp

increase

300 bp

increase

December 31, 2013

Assets:

Investments in fixed maturity securities .................... $29,370 $30,160 $28,591 $27,870 $27,259

Other investments (1) .................................. 8,592 9,021 8,166 7,757 7,370

Loans and finance receivables ........................... 12,002 12,412 11,617 11,255 10,915

Liabilities:

Notes payable and other borrowings:

Insurance and other ................................ 13,147 13,776 12,595 12,104 11,663

Railroad, utilities and energy ........................ 49,879 54,522 45,906 42,500 39,554

Finance and financial products ....................... 13,013 13,703 12,405 11,867 11,385

Equity index put option contracts ......................... 4,667 5,589 3,876 3,200 2,626

December 31, 2012

Assets:

Investments in fixed maturity securities .................... $38,425 $39,333 $37,493 $36,592 $35,783

Other investments (1) .................................. 8,606 9,003 8,169 7,744 7,343

Loans and finance receivables ........................... 11,991 12,410 11,598 11,229 10,883

Liabilities:

Notes payable and other borrowings:

Insurance and other ................................ 14,284 14,794 13,815 13,398 13,018

Railroad, utilities and energy ........................ 42,074 46,268 38,519 35,495 32,902

Finance and financial products ....................... 14,005 14,597 13,432 12,950 12,519

Equity index put option contracts ......................... 7,502 8,980 6,226 5,131 4,198

(1) Includes other investments that are subject to a significant level of interest rate risk.

Equity Price Risk

Historically, we have maintained large amounts of invested assets in exchange traded equity securities. Strategically, we

strive to invest in businesses that possess excellent economics, with able and honest management and at sensible prices and

prefer to invest a meaningful amount in each investee. Consequently, equity investments are concentrated in relatively few

issuers. At December 31, 2013, approximately 55% of the total fair value of equity investments was concentrated within four

companies.

100