The Hartford 2010 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2010 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

|

|

83

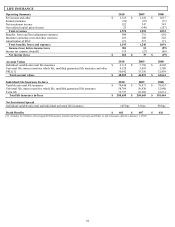

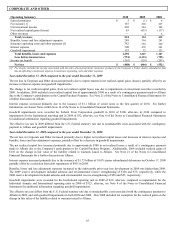

Year ended December 31, 2010 compared to the year ended December 31, 2009

Net income increased in 2010 compared to 2009 primarily due to net realized capital gains and Unlock benefit in 2010. In addition,

Life Insurance’ s net income increased, excluding the improvements to net realized gains and an Unlock benefit, due to improvements in

the segment’ s individual life business.

Life Insurance’ s net realized gains in 2010 compared to net realized capital losses in 2009 were primarily due to lower losses from

impairments. For further discussion on impairments, see Other-Than-Temporary Impairments within the Investment Credit Risk section

of the MD&A.

The Unlock benefit was $28, after-tax, in 2010 as compared to an Unlock charge of $51, after-tax, in 2009. The benefit in 2010 was

primarily due to assumption updates related to lapse rates, investment margin and mortality, partially offset by persistency, while 2009’ s

charge was primarily the result of assumption updates related to investment margin and expenses, as well as equity market performance

significantly below expectations in 2009, partially offset by assumption updates on lapse rates. The Unlock primarily resulted in

decreases to amortization of DAC and fee income and other. For further discussion of the Unlock see the Critical Accounting Estimates

within the MD&A.

Life Insurance’ s individual life business increased driven by improvements in net investment income primarily related to improved

performance of limited partnerships and other alternative investment and earnings on a higher average invested asset base in 2010

compared to 2009, partially offset by lower yields on fixed maturity investments. Net investment spread for individual life’ s variable

universal life and universal life products increased primarily due to the improved performance of limited partnerships and other

alternative investments for the year ended December 31, 2010.

Life Insurance’ s effective tax rate differs from the statutory rate of 35% primarily due to permanent differences for the separate account

DRD, partially offset by a valuation allowance on deferred tax benefits related to certain realized losses in 2010. Income taxes include

separate account DRD benefits of $19 in 2010 compared to $24 in 2009. For further discussion, see Note 13 of the Notes to

Consolidated Financial Statements.

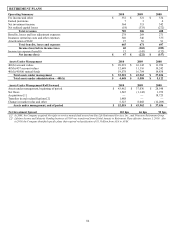

Year ended December 31, 2009 compared to the year ended December 31, 2008

Life Insurance’ s net income in 2009 compared to a net loss in 2008 is primarily due increased fee income and other and lower net

realized capital losses, as well as the impact of the effective tax rate, partially offset by the impact of the Unlock during the first quarter

of 2009.

Fee income and other increased primarily due to the impact of the amortization of unearned revenue reserves of $83 within the 2009

Unlock and increased cost of insurance charges of $38 for individual life products, as a result of growth in guaranteed universal life

insurance in-force, partially offset by lower variable life fees as a result of equity market declines.

Life Insurance’ s net realized losses decreased in 2009 compared to net realized losses in 2008 primarily due to lower impairments. For

further discussion on impairments, see Other-Than-Temporary Impairments within the Investment Credit Risk section of the MD&A.

The Unlock charge was $51, after-tax, in 2009 as compared to an Unlock charge of $44, after-tax, in 2008. The charges related to

assumption updates and the impact from equity market performance that was less than expectations was greater in 2009 than 2008. The

Unlock primarily resulted in increases to amortization of DAC and an increase in fee income and other as discussed above. For further

discussion of DAC Unlock see the Critical Accounting Estimates within the MD&A.

Life Insurance’ s effective tax rate differs from the statutory rate of 35% primarily due to permanent differences for the separate account

DRD. Income taxes include separate account DRD benefits of $24 in 2009 compared to $14 in 2008. For further discussion, see Note

13 of the Notes to Consolidated Financial Statements.

Net investment spread for individual variable universal life and universal life products was lower due to a decline in investment income

and an increase in interest credited. Interest credited increased due primarily to increased average account values, partially offset by a

reduction in the average credited rate of 18 bps.