The Hartford 2010 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2010 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

|

|

75

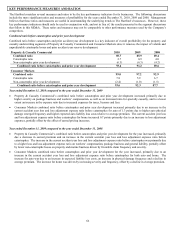

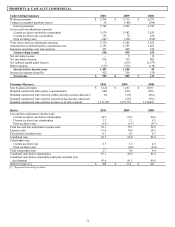

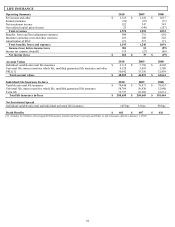

GROUP BENEFITS

Operating Summary 2010 2009 2008

Premiums and other considerations $ 4,278 $ 4,350 $4,391

Net investment income 429 403 419

Net realized capital gains (losses) 46 (124) (540)

Total revenues 4,753 4,629 4,270

Benefits, losses and loss adjustment expenses 3,331 3,196 3,144

Amortization of deferred policy acquisition costs 61 61 57

Insurance operating costs and other expenses 1,111 1,120 1,128

Total benefits, losses and expenses 4,503 4,377 4,329

Income (loss) before income taxes 250 252 (59)

Income tax expense (benefit) 65 59 (53)

Net income (loss) $ 185 $ 193 $(6)

Premiums and other considerations 2010 2009 2008

Fully insured – ongoing premiums $ 4,166 $ 4,309 $ 4,355

Buyout premiums 58 — 1

Other 54 41 35

Total premiums and other considerations $ 4,278 $ 4,350 $4,391

Fully insured ongoing sales, excluding buyouts $ 583 $ 741 $ 820

Ratios, excluding buyouts

Loss ratio 77.6% 73.5% 71.6%

Loss ratio, excluding financial institutions 82.8% 77.8% 76.3%

Expense ratio 27.8% 27.1% 27.0%

Expense ratio, excluding financial institutions 23.3% 22.6% 22.4%

Group Benefits has a block of financial institution business that is experience rated. This business comprised approximately 9% to 10%

of the segment’ s 2010, 2009 and 2008 premiums and other considerations (excluding buyouts). With respect to the segment’ s net

income (loss), excluding net realized capital gains (losses), the financial institution business comprised 6% for 2010, and on average,

2% to 4% for 2009 and 2008, excluding the commission accrual adjustment in 2009 discussed below.

Year ended December 31, 2010 compared to the year ended December 31, 2009

Net income decreased as compared to prior year, as a decrease in premiums and other considerations and higher claim costs offset the

improvements in net realized capital gains (losses) and net investment income. Premiums and other considerations decreased due to a

3% decline in fully insured ongoing premiums which was driven by lower sales due to the competitive marketplace, and the pace of the

economic recovery. The loss ratio, excluding buyouts, increased compared to the prior year, particularly in group disability, primarily

due to unfavorable morbidity experience from higher incidence and lower claim terminations.

The favorable change to net realized capital gains in 2010, from net realized capital losses in 2009, was due to impairments on

investment securities recorded in 2009. For further discussion on impairments, see Other-Than-Temporary Impairments within the

Investment Credit Risk section of the MD&A. Net investment income increased as a result of higher weighted average portfolio yields

primarily due to improved performance on limited partnerships and other alternative investments.

The effective tax rate, in both periods, differs from the U.S. Federal statutory rate primarily due to permanent differences related to

investments in tax exempt securities. For further discussion, see Income Taxes within Note 13 of the Notes to Consolidated Financial

Statements.

Year ended December 31, 2009 compared to the year ended December 31, 2008

The change to net income in 2009, from a net loss in 2008, was primarily due to lower net realized capital losses in 2009, partially offset

by higher claim costs, and decreases in premiums and other considerations and net investment income.

The lower net realized capital losses were primarily driven by fewer impairments in 2009 compared to 2008. For further discussion on

impairments, see Other-Than-Temporary Impairments within the Investment Credit Risk section of the MD&A.

The segment’ s loss ratio increased primarily due to unfavorable morbidity experience, which was primarily due to unfavorable reserve

development from the 2008 incurral loss year and higher new incurred long term disability claims in 2009. In addition, premiums and

other considerations decreased primarily due to reductions in covered lives within our customer base, and to a lesser extent, lower sales.

Fully insured ongoing sales, excluding buyouts, were lower as compared to the prior year due to the competitive marketplace and the

economic environment. Net investment income decreased primarily as a result of lower yields on fixed maturity investments.

The effective tax rate, in both periods, differs from the U.S. Federal statutory rate primarily due to permanent differences related to

investments in tax exempt securities. For further discussion, see Income Taxes within Note 13 of the Notes to Consolidated Financial

Statements.