The Hartford 2010 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2010 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

|

|

50

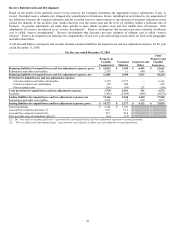

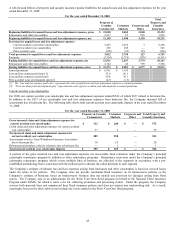

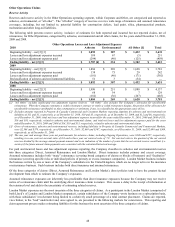

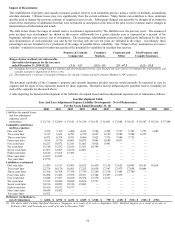

In reporting environmental results, the Company classifies its gross exposure into Direct, Assumed Reinsurance, and London Market.

The following table displays gross environmental reserves and other statistics by category as of December 31, 2010.

Summary of Environmental Reserves

As of December 31, 2010

Total Reserves

Gross [1] [2]

Direct $273

Assumed Reinsurance 47

London Market 58

Total 378

Ceded (39)

Net $339

[1] The one year gross paid amount for total environmental claims is $61, resulting in a one year gross survival ratio of 6.2.

[2] The three year average gross paid amount for total environmental claims is $56, resulting in a three year gross survival ratio of 6.8.

During the second quarters of 2010, 2009 and 2008, the Company completed its annual ground-up asbestos reserve evaluations. As part

of these evaluations, the Company reviewed all of its open direct domestic insurance accounts exposed to asbestos liability, as well as

assumed reinsurance accounts and its London Market exposures for both direct insurance and assumed reinsurance. Based on this

evaluation, the Company increased its net asbestos reserves by $169 in second quarter 2010. During 2010 and 2009, for certain direct

policyholders, the Company experienced increases in claim severity and expense. Increases in severity and expense were driven by

litigation in certain jurisdictions and, to a lesser extent, development on primarily peripheral accounts. The Company also experienced

unfavorable development on its assumed reinsurance accounts driven largely by the same factors experienced by the direct

policyholders. The net effect of these changes in 2009 resulted in a $138 increase in net asbestos reserves. In the second quarter of

2008, the Company found estimates for individual cases changed based upon the particular circumstances of each account. These

changes were case specific and not as a result of any underlying change in the current environment. The net effect of these changes

resulted in a $50 increase in net asbestos reserves. The Company currently expects to continue to perform an evaluation of its asbestos

liabilities annually.

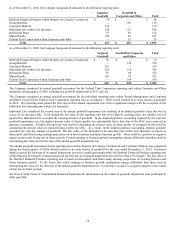

The Company classifies its gross asbestos exposures into Direct, Assumed Reinsurance and London Market. The Company further

classifies its direct asbestos exposures into the following categories: Major Asbestos Defendants (the “Top 70” accounts in Tillinghast’ s

published Tiers 1 and 2 and Wellington accounts), which are subdivided further as: Structured Settlements, Wellington, Other Major

Asbestos Defendants, Accounts with Future Expected Exposures greater than $2.5, Accounts with Future Expected Exposures less than

$2.5, and Unallocated.

• Structured Settlements are those accounts where the Company has reached an agreement with the insured as to the amount and

timing of the claim payments to be made to the insured.

• The Wellington subcategory includes insureds that entered into the “Wellington Agreement” dated June 19, 1985. The Wellington

Agreement provided terms and conditions for how the signatory asbestos producers would access their coverage from the signatory

insurers.

• The Other Major Asbestos Defendants subcategory represents insureds included in Tiers 1 and 2, as defined by Tillinghast that are

not Wellington signatories and have not entered into structured settlements with The Hartford. The Tier 1 and 2 classifications are

meant to capture the insureds for which there is expected to be significant exposure to asbestos claims.

• Accounts with future expected exposures greater or less than $2.5 include accounts that are not major asbestos defendants.

• The Unallocated category includes an estimate of the reserves necessary for asbestos claims related to direct insureds that have not

previously tendered asbestos claims to the Company and exposures related to liability claims that may not be subject to an

aggregate limit under the applicable policies.

An account may move between categories from one evaluation to the next. For example, an account with future expected exposure of

greater than $2.5 in one evaluation may be reevaluated due to changing conditions and recategorized as less than $2.5 in a subsequent

evaluation or vice versa.