The Hartford 2010 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2010 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

|

|

77

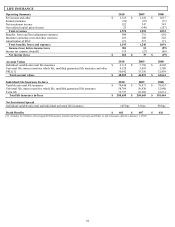

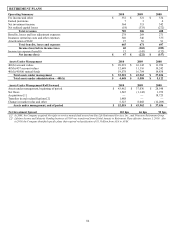

Ratios and Supplemental Data 2010 2009 2008

Loss and loss adjustment expense ratio

Current accident year before catastrophes 69.4 68.4 64.8

Current accident year catastrophes 7.6 5.8 6.5

Prior accident years (2.2) (0.8) (1.3)

Total loss and loss adjustment expense ratio 74.8 73.3 70.1

Expense ratio 24.2 23.9 22.8

Combined ratio 99.0 97.2 92.9

Catastrophe ratio

Current accident year 7.6 5.8 6.5

Prior accident years 0.3 0.1 0.2

Total catastrophe ratio 7.8 5.9 6.7

Combined ratio before catastrophes 91.2 91.3 86.2

Combined ratio before catastrophes and prior accident year development 93.6 92.3 87.7

Other revenues [1] $ 172 $ 154 $ 135

[1] Represents servicing revenues.

Product Combined Ratios 2010 2009 2008

Automobile 97.1 96.9 91.1

Homeowners 104.0 98.2 97.6

Total 99.0 97.2 92.9

Year ended December 31, 2010 compared to the year ended December 31, 2009

Net income increased slightly in 2010, as compared to the prior year, despite a decrease in underwriting results. The primary causes of

the decrease in underwriting results were higher current accident year losses and loss adjustment expenses, including catastrophes,

partially offset by more favorable prior accident year reserve development. The lower underwriting results were offset by improvements

in net realized capital gains (losses) and higher net investment income.

Earned premiums decreased in 2010, as lower earned premiums in auto were partially offset by an increase in homeowners’ . Auto

earned premiums were down reflecting a decrease in new business written premium and policy count retention since the fourth quarter

of 2009 and a decrease in average renewal earned premium per policy. Homeowners’ earned premiums grew primarily due to the effect

of increases in earned pricing, partially offset by a decrease in new business written premium and policy count retention.

Auto and home new business written premium decreased primarily due to the effect of written pricing increases and underwriting

actions that lowered the policy issue rate. Also contributing to the decrease in new business were fewer responses from direct marketing

on AARP business and fewer quotes from independent agents driven by increased competition. Partially offsetting the decrease in auto

new business was the effect of an increase in policies sold to AARP members through agents. Partially offsetting the decrease in home

new business was an increase in the cross-sale of homeowners’ insurance to insureds that have auto policies.

The change in auto renewal earned pricing was due to rate increases and the effect of policyholders purchasing newer vehicle models in

place of older models. Despite auto renewal earned pricing increasing, average renewal earned premium per policy for auto declined

due to a shift to more preferred market segments and a greater concentration of business in states and territories with lower average

premium. Homeowners’ renewal earned pricing increased due to rate increases and increased coverage amounts reflecting higher

rebuilding costs. For both auto and home, the Company has increased rates in certain states for certain classes of business to maintain

profitability in the face of rising loss costs.

Policy count retention for auto and home decreased primarily driven by the effect of renewal written pricing increases and underwriting

actions to improve profitability. The decrease in the policy count retention for homeowners was partially offset by the effect of the

Company’ s non-renewal of Florida homeowners’ agency business in 2009. Compared to 2009, the number of policies in-force as of

2010 decreased for both auto and home, driven by the decreases in policy retention and new business.

Current accident year losses and loss adjustment expenses before catastrophes increased primarily due to an increase in the current

accident year loss and loss adjustment expense ratio before catastrophes for auto of 1.3 points due to higher auto physical damage

emerged frequency and higher expected auto liability loss costs relative to average premium. The current accident year loss and loss

adjustment expense ratio before catastrophes for home increased 0.7 points primarily due to an increase in loss adjustment expenses,

partially offset by the effect of earned pricing increases.

Current accident year catastrophes were higher in 2010 than in 2009 primarily due to a severe wind and hail storm event in Arizona

during the fourth quarter of 2010. Losses in 2010 were also incurred from tornadoes, thunderstorms and hail events in the Midwest,

plains states and the Southeast, as well as from winter storms in the Mid-Atlantic and Northeast. Catastrophe losses in 2009 were

primarily incurred from windstorms in Texas and the Midwest as well as the two large Colorado hail and windstorm events.

Net favorable reserve development was higher in 2010 due to more favorable development of auto liability reserves. Net favorable

reserve development in both 2010 and 2009 included a release of personal auto liability reserves, partially offset by a strengthening of

reserves for non-catastrophe homeowners’ claims. For additional information on prior accident year reserve development, see the

Property and Casualty Insurance Product Reserves, Net of Reinsurance section within Critical Accounting Estimates.