The Hartford 2010 Annual Report Download - page 104

Download and view the complete annual report

Please find page 104 of the 2010 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

|

|

104

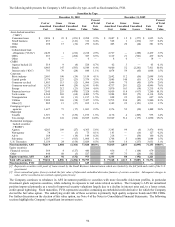

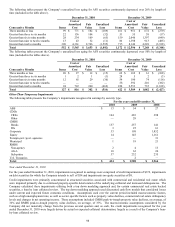

GMDB

The majority of the Company’ s U.S. variable annuity contracts include a GMDB rider. Declines in the equity markets will increase the

Company’ s liability for GMDB riders. The Company’ s total gross exposure (i.e., before reinsurance) to U.S. GMDB as of December

31, 2010 and December 31, 2009 is $10.7 billion and $18.4 billion, respectively. However, the Company will incur these payments in

the future only if the policyholder has an “in the money” GMDB at their death. As of December 31, 2010 and December 31, 2009, 70%

and 82%, respectively, of all unreinsured U.S. GMDB contracts were “in the money”. For those contracts that were “in the money”, the

average contract was 12% and 18% “in the money” as of December 31, 2010 and 2009, respectively. The Company reinsured 60% and

53% of these death benefit guarantees as of December 31, 2010 and December 31, 2009, respectively. Under certain of these

reinsurance agreements, the reinsurers’ exposure is subject to an annual cap. The Company’ s net exposure (i.e., after reinsurance), is

$4.3 billion and $8.5 billion, as of December 31, 2010 and December 31, 2009, respectively.

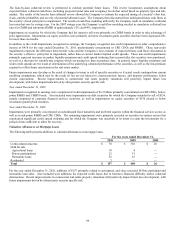

In the second quarter of 2009, the Company suspended all new product sales in Japan. Prior to that, the Company offered variable

annuity products in Japan with a GMDB. For the in-force block of Japan business, declines in equity markets, as well as a strengthening

of the Japanese yen in comparison to the U.S. dollar, the euro and other currencies will increase the Company’ s liability for GMDB

riders. This increase may be significant in extreme market scenarios. In general, the GMDB riders entitle the policyholder to receive

the original investment value at the date of death. If the original investment value exceeds the account value upon death then the

contract is “in the money”. As of December 31, 2010 and 2009, substantially all of the unreinsured Japan GMDB contracts were “in the

money”. For those contracts that were “in the money”, the average contract was 22% and 18% “in the money” as of December 31, 2010

and 2009, respectively. The Company’ s total gross exposure (i.e., before reinsurance) to the GMDB offered in Japan is $8.8 billion and

$6.3 billion as of December 31, 2010 and December 31, 2009, respectively. The Company reinsured 14% and 17% of the GMDB to a

third-party reinsurer as of December 31, 2010 and 2009, respectively. Under certain of these reinsurance agreements, the reinsurers’

exposure is subject to an annual cap. The Company’ s net GMDB exposure (i.e. after reinsurance) is $7.6 billion and $5.2 billion as of

December 31, 2010 and 2009, respectively. Many policyholders with a GMDB also have a GMWB in the US or GMIB in Japan.

Policyholders that have a product that offer both guarantees can only receive the GMDB or the GMIB benefit in Japan or the GMDB or

GMWB in the U.S. For additional information on the Company’ s GMDB liability, see Note 9 of the Notes to Consolidated Financial

Statements.

GMIB

In the second quarter of 2009, the Company suspended all new product sales in Japan. Prior to that, the Company offered variable

annuity products in Japan with a GMIB. For GMIB contracts, in general, the policyholder has the right to elect to annuitize benefits,

beginning (for certain products) on the tenth or fifteenth anniversary year of contract commencement, receive lump sum payment of

account value, or remain in the variable sub-account. For GMIB contracts, the policyholder is entitled to receive the original investment

value over a 10- to 15- year annuitization period. A small percentage of the contracts will first become eligible to elect annuitization

beginning in 2013. The remainder of the contracts will first become eligible to elect annuitization from 2014 to 2022. Because

policyholders have various contractual rights to defer their annuitization election, the period over which annuitization election can take

place is subject to policyholder behavior and therefore indeterminate. In addition, upon annuitization the contractholder surrenders

access to the account value and the account value is transferred to the Company’ s general account where it is invested and the additional

investment proceeds are used towards payment of the original investment value. If the original investment value exceeds the account

value upon annuitization then the contract is “in the money”. As of December 31, 2010 and 2009, substantially all of the Japan GMIB

contracts were “in the money”. For those contracts that were “in the money”, the average contract was 17% and 12% “in the money” as

of December 31, 2010 and 2009, respectively. In addition, as of December 31, 2010, 54% of retained net amount at risk is reinsured to

an affiliate of The Hartford. For additional information on the Company’ s GMIB liability, see Note 9 of the Notes to Consolidated

Financial Statements.

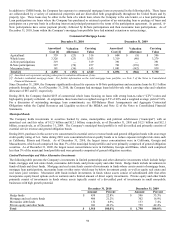

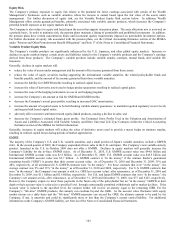

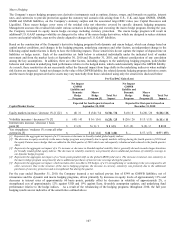

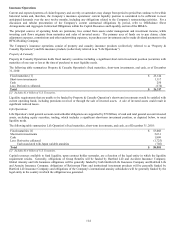

The following table represents the timing of account values eligible for annuitization under the Japan GMIB as of December 31, 2010,

as well as the retained net amount at risk. The account values reflect 100% annuitization at the earliest point allowed by the contract

and no adjustments for future market returns and policyholder behaviors. Future market returns, changes in the value of the Japanese

yen and policyholder behaviors will impact account values eligible for annuitization in the years presented.

GMIB [1]

($ in billions) Account Value Net Amount at Risk

2013 $ 0.3 $ —

2014 4.7 0.7

2015 7.6 1.4

2016 2.6 0.6

2017 2.9 0.7

2018 & beyond [2] 7.3 2.0

Total $ 25.4 $ 5.4

[1] Excludes certain GMIB products where annuitization eligibility is based on attained age.

[2] In 2018 & beyond, $2.8 billion of the $7.3 billion is primarily associated with account value that is eligible in 2021.