Lenovo 2014 Annual Report Download - page 151

Download and view the complete annual report

Please find page 151 of the 2014 Lenovo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

|

|

149

2013/14 Annual Report Lenovo Group Limited

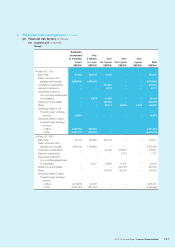

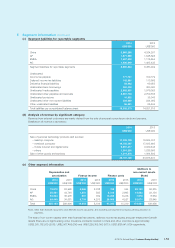

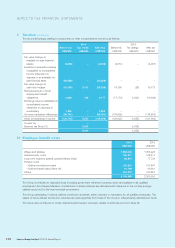

3 Financial risk management (continued)

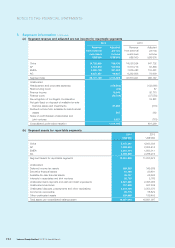

(c) Capital risks management (continued)

In order to maintain or adjust the capital structure, the Group may adjust the amount of dividends paid to shareholders,

return capital to shareholders, issue new shares or sell assets to reduce debt.

Consistent with others in the industry, the Group monitors capital on the basis of gearing ratio. This ratio is calculated

as total borrowings (including current and non-current borrowings) divided by total equity. The Group’s strategy remains

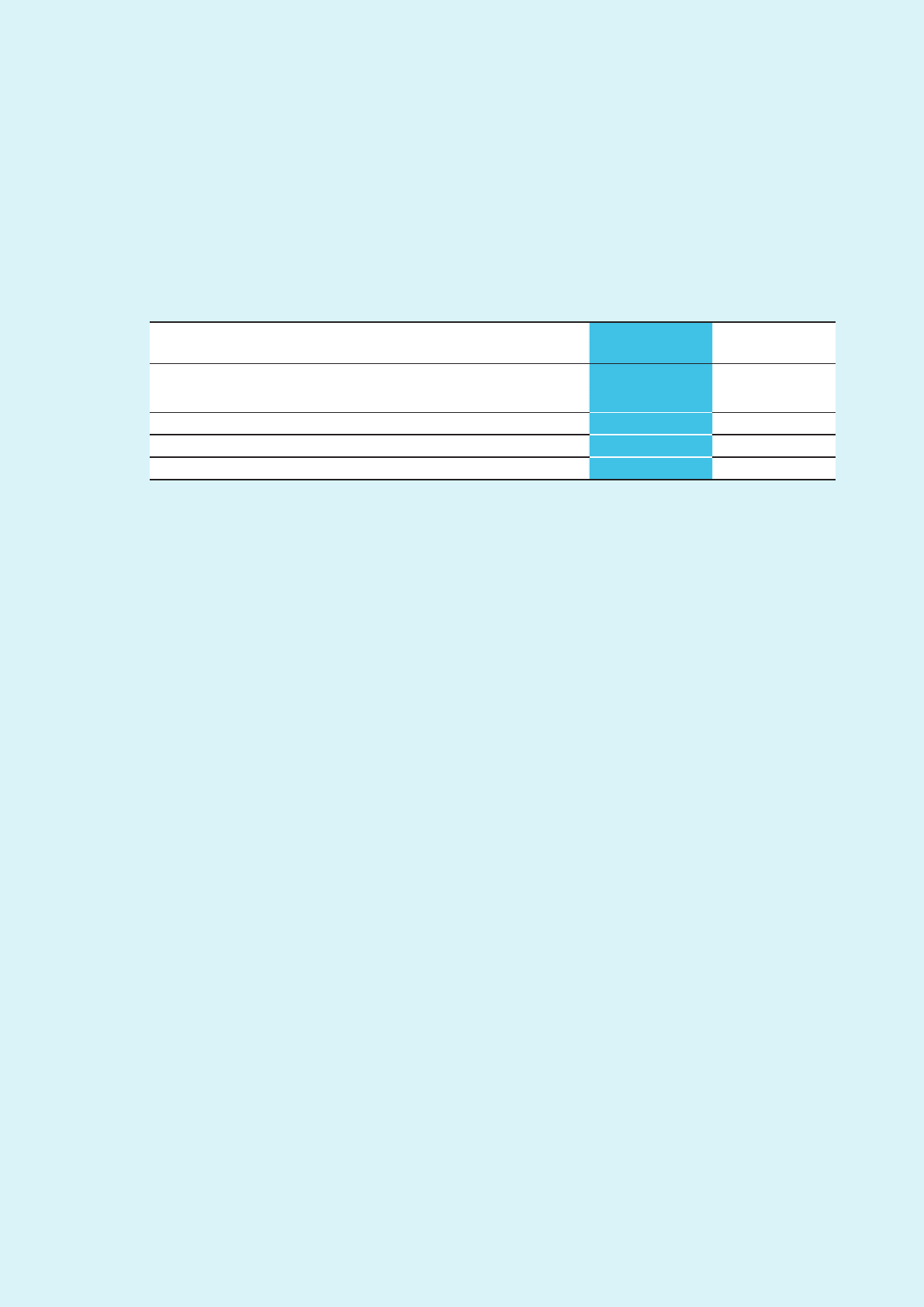

unchanged and the gearing ratios and net cash position of the Group as at March 31, 2014 and 2013 are as follows:

2014 2013

US$ million US$ million

Bank deposits and cash and cash equivalents 3,953 3,573

Less: total borrowings (455) (479)

Net cash position 3,498 3,094

Total equity 3,025 2,680

Gearing ratio 0.15 0.18

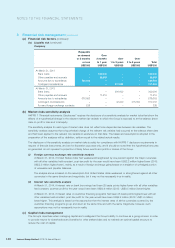

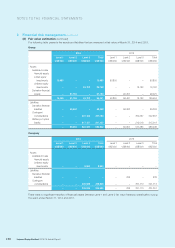

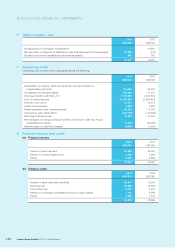

(d) Fair value estimation

The table below analyzes financial instruments carried at fair value, by valuation method. The different levels have been

defined as follows:

– Level 1 Quoted prices (unadjusted) in active markets for identical assets or liabilities

– Level 2 Inputs other than quoted prices included within level 1 that are observable for the asset or liability,

either directly (that is, as prices) or indirectly (that is, derived from prices)

– Level 3 Inputs for the asset or liability that are not based on observable market data (that is,

unobservable inputs)

The fair value of financial instruments traded in active markets is based on quoted market prices at the balance sheet date.

A market is regarded as active if quoted prices are readily and regularly available from an exchange, dealer, broker, industry

group, pricing service, or regulatory agency, and those prices represent actual and regularly occurring market transactions

on an arm’s length basis. The quoted market price used for financial assets held by the Group is the current bid price.

These instruments are included in Level 1.

The fair value of financial instruments that are not traded in an active market (for example, over-the-counter derivatives)

is determined by using valuation techniques. These valuation techniques maximize the use of observable market data

where it is available and rely as little as possible on entity specific estimates. If all significant inputs required to fair value an

instrument are observable, the instrument is included in Level 2.

If one or more of the significant inputs is not based on observable market data, the instrument is included in Level 3.

Specific valuation techniques used to value financial instruments include:

– Quoted market prices or dealer quotes for similar instruments are used for long-term debt.

– The fair value of interest rate swaps is calculated as the present value of the estimated future cash flows based on

observable yield curves.

– The fair value of forward foreign exchange contracts is determined using quoted forward exchange rates at the

balance sheet date, with the resulting value discounted back to present value.

– Other techniques, such as estimated discounted cash flows, are used to determine fair value for the remaining

financial instruments.