Xerox 2007 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2007 Xerox annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in millions, except per-share data and unless otherwise indicated)

Fair Value Accounting: In 2006, the FASB issued

SFAS No. 157, “Fair Value Measurements” (“FAS 157”).

FAS 157 defines fair value, establishes a market-based

framework or hierarchy for measuring fair value, and

expands disclosures about fair value measurements. FAS

157 is applicable whenever another accounting

pronouncement requires or permits assets and liabilities to

be measured at fair value. FAS 157 does not expand or

require any new fair value measures, however the

application of this statement may change current practice.

The requirements of FAS 157 are first effective for our

fiscal year beginning January 1, 2008. However, in

February 2008 the FASB decided that an entity need not

apply this standard to nonfinancial assets and liabilities

that are recognized or disclosed at fair value in the

financial statements on a nonrecurring basis until the

subsequent year. Accordingly, our adoption of this

standard on January 1, 2008 is limited to financial assets

and liabilities, which primarily affects the valuation of our

derivative contracts. We do not believe the initial adoption

of FAS 157 will have a material effect on our financial

condition or results of operations. However, we are still in

the process of evaluating this standard with respect to its

effect on nonfinancial assets and liabilities and therefore

have not yet determined the impact that it will have on

our financial statements upon full adoption.

In February 2007, the FASB issued SFAS No. 159,

“The Fair Value Option for Financial Assets and Financial

Liabilities – Including an Amendment of FASB Statement

No. 115” (“FAS 159”). FAS 159 permits entities to choose

to measure many financial instruments and certain other

items at fair value. Entities that elect the fair value option

will report unrealized gains and losses in earnings at each

subsequent reporting date. The fair value option may be

elected on an instrument-by-instrument basis, with few

exceptions. FAS 159 also establishes presentation and

disclosure requirements to facilitate comparisons between

companies that choose different measurement attributes

for similar assets and liabilities. The requirements of FAS

159 are effective for our fiscal year beginning January 1,

2008. We do not believe that the adoption of this

statement will have a material effect on our financial

condition or results of operations as election of this option

for our financial instruments is expected to be limited.

Stock-Based Compensation: In 2004, the FASB

issued SFAS No. 123(R), “Share-Based Payment” (“FAS

123(R)”), which requires companies to recognize

compensation expense using a fair value based method

for costs related to all share-based payments, including

stock options. On January 1, 2006, we adopted FAS 123(R)

using the modified prospective transition method and

therefore we did not restate the results of prior periods.

Prior to the adoption of FAS 123(R), under previous

accounting guidance, we did not expense stock options, as

there was no intrinsic value associated with the options

granted because the exercise price was set equal to the

market price at the date of grant. The adoption of FAS

123(R) was immaterial to our results of operations

primarily as a result of changes made in our stock-based

compensation programs in 2005, including the

accelerated vesting of substantially all outstanding

unvested stock options prior to the adoption of FAS

123(R).

In 2005, we implemented changes in our stock-based

compensation programs that included expanded use of

restricted stock grants with time and performance-based

restrictions in lieu of stock options. Prior to this change, our

stock-based compensation programs primarily consisted

of stock option grants. These new restricted stock awards

are reflected as compensation expense in our results of

operations for all years presented and the adoption of FAS

123(R) did not materially affect the expense recognized

for these awards.

In 2005, we accelerated the vesting of approximately

3.6 million stock options granted in 2004 that would have

been scheduled to vest on January 1, 2007, to

December 31, 2005. The accelerated vesting resulted in

substantially all outstanding stock options being vested at

the date of the adoption of FAS 123(R). The primary

purpose of this accelerated vesting was to reduce our pre-

tax compensation expense in 2006 by approximately $31

or $0.02 per diluted share.

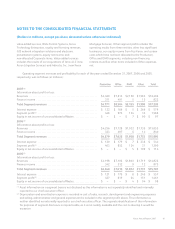

Stock-based compensation expense for the three

years ended December 31, 2007 was as follows (in

millions):

2007 2006 2005

Stock-based compensation expense,

pre-tax ......................... $89 $64 $40

Stock-based compensation expense,

netoftax ....................... 55 39 25

Prior to 2006, in accordance with previous accounting

guidance we did not recognize compensation expense

relating to employee stock options because the exercise

84