Xerox 2007 Annual Report Download - page 112

Download and view the complete annual report

Please find page 112 of the 2007 Xerox annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in millions, except per-share data and unless otherwise indicated)

At December 31, 2006, we had outstanding Japanese

Yen/USD cross-currency interest rate swap agreements

with aggregate notional amounts of $126 and a net

liability fair value of $9. These contracts matured during

2007 together with the scheduled repayment of the

related debt. No such contracts were outstanding at

December 31, 2007.

Cash Flow Hedges:

Debt related: As of December 31, 2006, our cross

currency interest rate swaps were used to hedge the

currency exposure for interest payments and principal on

half of our Japanese Yen denominated debt of ¥30 billion

(U.S. $252). In addition, certain forward currency

contracts were used to hedge the currency exposure for

interest payments on the remaining Yen debt. These

combined strategies converted the hedged cash flows on

our Japanese Yen denominated debt to U.S. dollars and

qualified for cash flow hedge accounting. The derivatives

matured during 2007 together with the scheduled

repayment of the related debt.

No amount of ineffectiveness was recorded in the

Consolidated Statements of Income for the three years

ended December 31, 2007 for these designated cash flow

hedges and all components of each derivative’s gain or

loss was included in the assessment of hedge

effectiveness.

Inventory purchases: During 2007 we began to

designate some of our foreign currency derivative

contracts as cash flow hedges for a portion of our

foreign currency denominated inventory purchases.

The changes in fair value for these contracts were

reported in AOCL and reclassified to Cost of Sales in the

period or periods during which the related inventory

was sold. No amount of ineffectiveness was recorded in

the Consolidated Statements of Income for these

designated cash flow hedges and all components of

each derivative’s gain or loss was included in the

assessment of hedge effectiveness. As of December 31,

2007, there were no contracts outstanding.

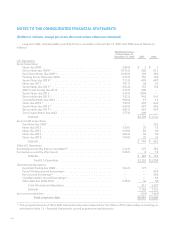

Accumulated Other Comprehensive Loss

(“AOCL”): The following table provides a summary of

the activity associated with all of our designated cash

flow hedges (interest rate and foreign currency)

reflected in AOCL for the three years ended

December 31, 2007:

Years ended

December 31,

2007 2006 2005

Net Gain/(Loss):

Beginning balance, net of tax ...... $ 1 $1 $ 3

Changes in fair value .............. 4 (1) (32)

Reclass to earnings ................ (5) 1 30

Ending balance, net of tax ...... $– $1 $ 1

Fair Value of Financial Instruments: The estimated fair values of our financial instruments at December 31, 2007

and 2006 were as follows:

2007 2006

(in millions) Carrying

Amount Fair

Value Carrying

Amount Fair

Value

Cash and cash equivalents .................................................. $1,099 $1,099 $1,399 $1,399

Short-term investments ..................................................... – – 137 137

Accounts receivable, net .................................................... 2,457 2,457 2,199 2,199

Short-term debt ............................................................ 525 525 1,485 1,487

Long-term debt ............................................................ 6,939 7,176 5,660 5,917

Liability to subsidiary trust issuing preferred securities ......................... 632 632 624 640

The fair value amounts for Cash and cash equivalents

and Accounts receivable, net approximate carrying

amounts due to the short maturities of these instruments.

The fair value of Short and Long-term debt, as well as our

Liability to subsidiary trust issuing preferred securities, was

estimated based on quoted market prices for publicly

traded securities or on the current rates offered to us for

debt of similar maturities. The difference between the fair

value and the carrying value represents the theoretical net

premium or discount we would pay or receive to retire all

debt at such date.

110