Xerox 2007 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2007 Xerox annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

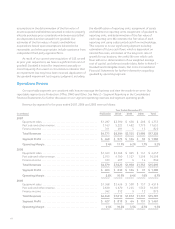

Defined Benefit Pension and Other Postretirement Plans,

an amendment of FASB Statements No. 87, 88, 106 and

132(R).”

Income Taxes and Tax Valuation Allowances: We

record the estimated future tax effects of temporary

differences between the tax bases of assets and liabilities

and amounts reported in our Consolidated Balance

Sheets, as well as operating loss and tax credit

carryforwards. We follow very specific and detailed

guidelines in each tax jurisdiction regarding the

recoverability of any tax assets recorded in our

Consolidated Balance Sheets and provide necessary

valuation allowances as required. We regularly review our

deferred tax assets for recoverability considering historical

profitability, projected future taxable income, the

expected timing of the reversals of existing temporary

differences and tax planning strategies. If we continue to

operate at a loss in certain jurisdictions or are unable to

generate sufficient future taxable income, or if there is a

material change in the actual effective tax rates or time

period within which the underlying temporary differences

become taxable or deductible, we could be required to

increase the valuation allowance against all or a

significant portion of our deferred tax assets resulting in a

substantial increase in our effective tax rate and a

material adverse impact on our operating results.

Conversely, if and when our operations in some

jurisdictions were to become sufficiently profitable to

recover previously reserved deferred tax assets, we would

reduce all or a portion of the applicable valuation

allowance in the period when such determination is made.

This would result in an increase to reported earnings in

such period. Adjustments to our valuation allowance,

through charges/(credits) to income tax expense, were

$14 million, $12 million, and $(38) million for the years

ended December 31, 2007, 2006 and 2005, respectively.

There were other increases/(decreases) to our valuation

allowance, including the effects of currency, of $86

million, $45 million, and $61 million for the years ended

December 31, 2007, 2006 and 2005, respectively, that did

not affect income tax expense in total as there was a

corresponding adjustment to deferred tax assets or other

comprehensive income. Gross deferred tax assets of $3.6

billion and $3.9 billion had valuation allowances of $747

million and $647 million at December 31, 2007 and 2006,

respectively.

We adopted FASB Interpretation No. 48, “Accounting

for Uncertainty in Income Taxes – an Interpretation of

FASB Statement No. 109,” on January 1, 2007. The

adoption of this interpretation changed the way we

evaluated recognition and measurement of uncertain tax

positions. Refer to Note 1 – “New Accounting Standards

and Accounting Changes” and Note 15 – “Income and

Other Taxes” in the Consolidated Financial Statements for

further information regarding the adoption and

application of this interpretation.

We are subject to ongoing tax examinations and

assessments in various jurisdictions. Accordingly, we may

incur additional tax expense based upon our assessment

of the more-likely-than-not outcomes of such matters. In

addition, when applicable, we adjust the previously

recorded tax expense to reflect examination results. Our

ongoing assessments of the more-likely-than-not

outcomes of the examinations and related tax positions

require judgment and can materially increase or decrease

our effective tax rate as well as impact our operating

results.

We file income tax returns in the U.S. Federal

jurisdiction and various foreign jurisdictions. In the U.S. we

are no longer subject to U.S. Federal income tax

examinations by tax authorities for years before 2006.

With respect to our major foreign jurisdictions, we are no

longer subject to tax examinations by tax authorities

before 2000.

Legal Contingencies: We are involved in a variety of

claims, lawsuits, investigations and proceedings

concerning securities law, intellectual property law,

environmental law, employment law and ERISA, as

discussed in Note 16 – Contingencies in the Consolidated

Financial Statements. We determine whether an

estimated loss from a contingency should be accrued by

assessing whether a loss is deemed probable and can be

reasonably estimated. We assess our potential liability by

analyzing our litigation and regulatory matters using

available information. We develop our views on estimated

losses in consultation with outside counsel handling our

defense in these matters, which involves an analysis of

potential results, assuming a combination of litigation and

settlement strategies. Should developments in any of

these matters cause a change in our determination as to

an unfavorable outcome and result in the need to

recognize a material accrual, or should any of these

matters result in a final adverse judgment or be settled for

significant amounts, they could have a material adverse

effect on our results of operations, cash flows and

financial position in the period or periods in which such

change in determination, judgment or settlement occurs.

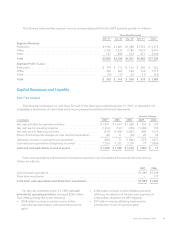

Business Combinations and Goodwill: The application

of the purchase method of accounting for business

combinations requires the use of significant estimates and

Xerox Annual Report 2007 59