Vodafone 2003 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2003 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

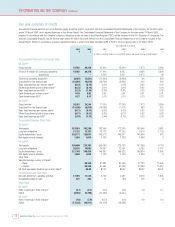

Vodafone Group Plc Annual Report & Accounts and Form 20-F 2003 29

Revenue recognition and presentation

Turnover from mobile telecommunications comprises amounts charged to

customers in respect of monthly access charges, airtime usage, messaging, the

provision of other mobile telecommunication services, including data services

and information provision, fees for connecting customers to a mobile network

and revenues from the sale of equipment, including handsets. Turnover is

reported for all segments, including “Other operations”which primarily comprises

amounts charged to customers of the Group’s fixed line businesses, principally in

respect of access charges and line usage.

When determining the amount of revenue to record in any period, the overriding

principle followed is to match revenues with the provision of service. When

deciding the most appropriate basis for presenting revenue or costs of revenue,

both the legal form and substance of the agreement between the Group and its

business partners are reviewed to determine each parties’ respective roles in the

transaction.

Where the Group’s role in a transaction is that of principal, revenue is recognised

on a gross basis. This requires turnover to comprise the gross value of the

transaction billed to the customer, after trade discounts, with any related

expenditure charged as an operating cost.

Where the Group’s role in a transaction is that of an agent, revenue is

recognised on a net basis, with turnover representing the margin earned and no

entries made to operating costs.

Revenues generated through the provision of voice or messaging services are

measured according to the appropriate tariff structure and accounted for gross of

any amounts payable to third parties for interconnect fees or other similar

charges. Such revenues principally comprise amounts charged to contract

customers for monthly access charges, which are invoiced and recorded as part

of a periodic billing cycle, and airtime, either from contract customers as part of

the invoiced amount, or prepaid customers through the sale of prepaid top up

cards. Revenue is recorded in the period in which the customer uses the service.

Unbilled turnover resulting from mobile services provided to contract customers

from the billing cycle date to the end of each period is accrued. Unearned

monthly access charges relating to periods after each accounting period are

deferred.

Turnover from a customer for the purchase of a handset or other equipment is

recognised upon delivery to the customer. Connection revenues are recognised

upon connection of the customer to the network. A customer, whether prepaid or

contract, is recognised as such upon activation of the handset or SIM card for

use by the end user customer. Costs of connecting a customer to a network are

also taken to the profit and loss account at the point when the customer

connects to the network.

Retirement benefits

The Group accounts for retirement benefits in accordance with SSAP 24,

“Accounting for pension costs”, and provides additional disclosures as required by

FRS 17, “Retirement benefits”. Application of SSAP 24 requires the exercise of

judgement in relation to assumptions for expected rates of inflation, expected asset

returns, salary and pension increases and a suitable rate at which liabilities can be

discounted. These assumptions used are derived following discussion with a firm of

independent actuaries. Accordingly, they are subject to periodic review and change.

Accounting for pensions under SSAP 24 allows certain gains and losses to be

spread over the average service lives of employees, thereby reducing the impact

of changes in actuarial assumptions on the period’s reported profit or loss.

However, pensions schemes are subject to periodic review by independent

actuaries which, typically, also result in assumptions being changed to take into

account any economic and demographic changes.

The Group’s total pension charge for the year, which is shown as part of other

administrative costs, amounted to £95 million (2002: £64 million, 2001:

£47 million). Most countries in which the Group operates have pension schemes

and so all segments are affected, albeit to a lesser or greater extent dependent

on the relative size and nature of the various schemes.

SSAP 24 is expected to be replaced by FRS 17 (or its international equivalent,

IAS 19, “Employee benefits”) and will result in pension scheme assets being

accounted for at market values. Liabilities will continue to be subject to

discounting. However, any resultant gains or losses will be reported in the profit

and loss account or statement of total recognised gains and losses, depending

on their nature, as they are identified and will therefore increase volatility in the

profit and loss account.

US GAAP

The Group also prepares a reconciliation of the Group’s revenues, net loss,

shareholders’ equity and total assets between UK GAAP and US GAAP, involving

the application of adjustments in conformity with accounting policies compliant

with US GAAP. Of these policies, the policies on revenue recognition and goodwill

and other intangibles are considered critical and are discussed below. This

discussion should also be read in conjunction with the description of the Group’s

US GAAP accounting policies and other US GAAP-related disclosures provided in

note 37 to the Consolidated Financial Statements, “US GAAP information”.

Revenue recognition

Under US GAAP, whilst the accounting treatment of revenue follows similar

principles to those followed under UK GAAP, US Staff Accounting Bulletin (“SAB”)

No. 101, “Revenue Recognition in Financial Statements”, results in the Group’s

connection revenues being accounted for in a different way to that prescribed

under UK GAAP and described above. SAB 101 specifies that performance is

viewed from the perspective of the customer and takes place over the life of the

customer relationship.

Deferring connection revenues and associated costs over the estimated life of

the customer relationship, using the methodology required under SAB 101,

results in the Group’s revenues for the 2003, 2002 and 2001 financial years

being reduced by £1,760 million, £1,044 million and £492 million, respectively.

Profits are materially unaffected by this adjustment as a broadly equal amount of

costs would also be deferred.

Goodwill and other intangibles

Under US GAAP, the accounting treatment for goodwill and other intangible

assets is different to that required by UK GAAP and described above and

represents the most significant adjustment made to the Group’s results and

financial position under UK GAAP when reconciling to US GAAP.

The difference can be attributed to three separate items: a) the difference in

goodwill arising as a result of the different basis by which the purchase price is

derived under US GAAP; b) the allocation of the resultant purchase price to a

series of identifiable intangible assets under US GAAP as opposed to only

goodwill under UK GAAP; and c) the US GAAP deferred tax treatment of

intangible assets which increases acquisition liabilities. Of these three

adjustments, the only one to involve management judgement is b). Allocation of

the purchase price affects the future results of the Group under US GAAP as the

requirements for separate identification of intangible assets is more prescriptive

under US GAAP.

Once capitalised, goodwill and other indefinite-lived intangible assets are not

amortised but are reviewed annually for impairment. Other intangible assets are

amortised over their estimated useful economic life under the basis described for