Vodafone 2003 Annual Report Download - page 129

Download and view the complete annual report

Please find page 129 of the 2003 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

Vodafone Group Plc Annual Report & Accounts and Form 20-F 2003 127

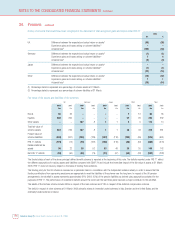

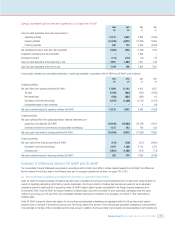

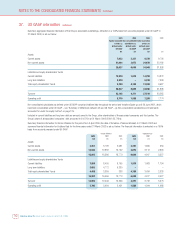

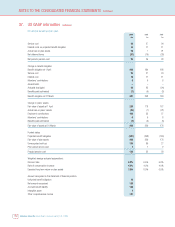

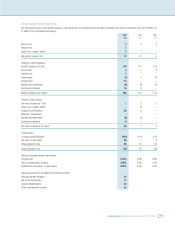

(g) Income taxes

Under UK GAAP, deferred tax is provided in full on timing differences that result in an obligation at the balance sheet date to pay more tax, or a right to pay

less tax, at a future date, at rates expected to apply when they crystallise based on current tax rates and law. Under US GAAP, deferred tax assets and

liabilities are provided in full on all temporary differences and a valuation adjustment is established in respect of those deferred assets where it is more likely

than not that some portion will not be realised. The most significant component of the income tax adjustment is due to the temporary difference between the

assigned values and tax values of intangible assets acquired in a business combination, which results in the recognition of a deferred tax liability under US

GAAP. Under UK GAAP, no deferred tax liability is recognised.

Under UK GAAP, the tax benefit received on the exercise of share options by employees, being the tax on the difference between the market value on the

date of exercise and the exercise price, is shown as a component of the tax charge for the period. Under US GAAP, the tax benefit is shown as a component

of paid-in capital on issue of shares.

In addition, deferred taxation assets are recognised for future deductions and utilisation of tax carry-forwards, subject to a valuation allowance. The valuation

allowance established against deferred tax assets is £11,446m (2002: £488m), the movement in the year being £10,958m. The valuation allowance is

mainly in respect of tax losses amounting to £11,226m (2002: £378m) not recognised.

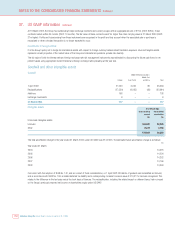

(h) Minority interests

The adjustments in respect of minority interests primarily relate to intangibles and provisions for deferred tax which have been recognised for US GAAP

purposes by a less than 100% owned subsidiary undertaking.

(i) Loss on sale of business

The loss on sale of business in 2002 represents the loss on sale of a business, which was sold fifteen months after the date of acquisition.

Under UK GAAP, the fair value of an acquired business can be amended up until the end of the financial year after acquisition. Under US GAAP, the fair value

can only be adjusted for one year following acquisition.

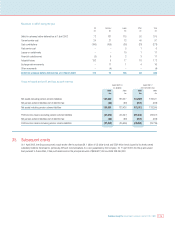

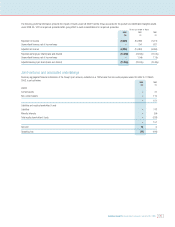

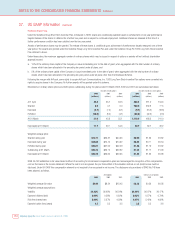

(j) Other

Licence fee amortisation – Under UK GAAP, the Group has adopted a policy of amortising licence fees in proportion to the capacity of the network during the

start up period and then on a straight line basis. Under US GAAP, licence fees are amortised on a straight line basis from the date that operations commence

to the date the licence expires.

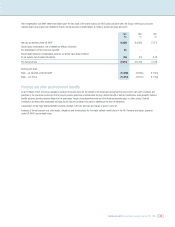

Pension costs – Under both UK GAAP and US GAAP pension costs provide for future pension liabilities. However, there are differences in the prescribed

methods of valuation, which give rise to GAAP adjustments to the pension cost and the pension prepayment.

Capitalisation of computer software costs – Under UK GAAP, costs that are directly attributable to the development of computer software for continuing use in

the business, whether purchased from external sources or developed internally, are capitalised. Under US GAAP, data conversion costs and costs incurred

during the research stage of software projects are not capitalised.

Investments in own shares – Investment in the Company’s own shares are included within other fixed asset investments under UK GAAP. US GAAP requires

investments in own shares to be shown as a deduction from equity.

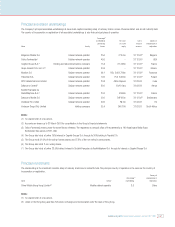

Gain on disposal of fixed assets and fixed asset investments – Under US GAAP, the net gain on disposal of fixed assets and fixed asset investments of £3m

and £255m, respectively (2002: £10m and £9m, 2001: £6m and £6m) would be included within operating income.

Marketable securities – Under US GAAP, SFAS No. 115, “Accounting for Certain Investments in Debt and Equity Securities”, the Group classifies its

marketable equity securities with readily determinable fair values as available-for-sale and are stated at fair value with the unrealised loss or gain, net of

deferred taxes, reported in shareholders’ equity.

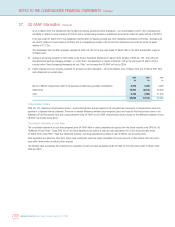

Derivative instruments – All the Group’s transactions in derivative financial instruments are undertaken for risk management purposes only and are used to

hedge its exposure to interest rate and foreign currency risk. In accordance with UK GAAP, to the extent that such instruments are matched against an

underlying asset or liability, they are accounted for as hedging transactions and recorded at appropriate historical amounts, with fair value information

disclosed in the Notes to the Consolidated Financial Statements. Under US GAAP, in accordance with SFAS No. 133, the Group’s derivative financial

instruments, together with any separately identified embedded derivatives, are reported as assets or liabilities on the Group’s balance sheet at fair value with

changes in their fair value accounted for through either the profit and loss account or statement of other comprehensive income. However, the Group has

designated certain of its derivative instruments as hedges for US GAAP purposes and accordingly, recognises any corresponding changes in the fair value of

the underlying assets, liabilities or positions being hedged. Under US GAAP, all derivatives not designated as hedges are recorded on the balance sheet at fair

value, with all changes in fair value accounted for in the profit and loss account. The Group does not pursue hedge accounting treatment for:

–interest rate futures, which are typically used to switch floating interest rates to fixed interest rates;

– derivatives entered into for funding and liquidity purposes, including forwards; or

–individual contracts where the underlying value of the transaction amounts to less than £10m.

Upon first adopting SFAS No. 133, on 1 April 2002, a cumulative transition adjustment was made which increased US GAAP net income and other

comprehensive income by £17m and £Nil, respectively. For the year ended 31 March 2002, the impact of SFAS No. 133 on the Group’s financial position