Vodafone 2003 Annual Report Download - page 117

Download and view the complete annual report

Please find page 117 of the 2003 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

Vodafone Group Plc Annual Report & Accounts and Form 20-F 2003 115

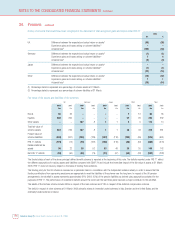

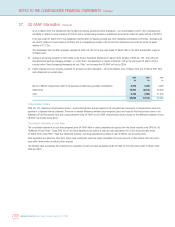

34. Pensions

As at 31 March 2003, the Group operated a number of pension plans for the benefit of its employees throughout the world, which vary with conditions and

practices in the countries concerned. All the Group’s pension plans are provided either through defined benefit or defined contribution arrangements. Defined

benefit schemes provide benefits based on the employees’ length of pensionable service and their final pensionable salary or other criteria. Defined

contribution schemes offer employees individual funds that are converted into benefits at the time of retirement.

Further details on the three principal defined benefit pension schemes, in the United Kingdom, Germany and Japan are shown below. In addition to principal

schemes, the Group operates defined benefit schemes in Ireland, Sweden, Italy, Greece and the United States. Defined contribution pension schemes are

provided in Australia, Egypt, Germany, Greece, Ireland, Italy, Malta, the Netherlands, New Zealand, Portugal, Spain, the United Kingdom and the United States.

The Group accounts for its pension schemes in accordance with SSAP 24, “Accounting for pension costs”. Disclosures required by SSAP 24 are detailed in

“Pension disclosures required under SSAP 24”below. Additional disclosures regarding the Group’s defined benefit pension schemes are also required under

the transitional provisions of FRS 17, “Retirement benefits”and these are set out in “Additional disclosures in respect of FRS 17”below.

The bases of calculation under FRS 17 are significantly different to SSAP 24. Whilst both require use of formal actuarial valuations, FRS 17 requires the use

of a different set of underlying assumptions and also specifies more frequent valuation updates. Accordingly, if FRS 17 is implemented in full, the Group’s

reported pension costs and balance sheet position are likely to change.

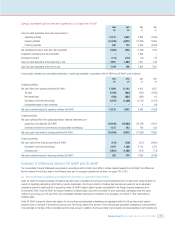

United Kingdom

The majority of the UK employees are members of the Vodafone Group Pension Scheme (the “main scheme”). This is a tax approved scheme, the assets of

which are held in a separate trustee-administered fund. In addition there is an internally funded unapproved defined benefit plan in place for a small number

of senior executives. The Group also operates a funded unapproved defined contribution scheme for certain senior executives. The pension cost for all three

arrangements is included in the summary information shown below.

The main scheme is subject to quarterly funding updates by independent actuaries and to formal actuarial valuations at least every three years. The most

recent formal valuation of this scheme was carried out as at 31 March 2001 using market based principles and the projected unit funding method of

valuation including allowance for projected earnings growth. The principal actuarial assumptions used in valuing the scheme liabilities are set out in “Pension

disclosures required under SSAP 24”below.

At 31 March 2001, the market value of the main scheme of £177m was sufficient to cover 84% of the benefits accrued to members. Against the shortfall at

31 March 2001 the UK companies have already made special lump sum contributions totalling £94m, including a £72m contribution during the 2003

financial year. In addition, the UK companies continue to make contributions significantly in excess of the cost of the benefits being earned each year. Using

consistent assumptions to those outlined above the updated funding level as at 31 March 2003 has been estimated as 92%. The average contribution rate

for the year ended 31 March 2003, excluding special lump sum contributions, was 13% of pensionable earnings. This level of contributions is currently

expected to continue.

As a result of the acceleration of payments a net prepayment of £136m (2002: £54m) is included in debtors due after more than one year, representing the

excess of the amounts funded over accumulated pension costs.

Germany

There are a number of separate pension and associated arrangements in Germany, one of which is fully externally financed and a number of which are now

funded through a trust arrangement.

During the 2003 financial year, the Group obtained approval to set up a separate trustee administered arrangement to fund part of its pension and other

associated obligations in relation to employees in Germany. An initial contribution of £95m was made into this trust arrangement relating to the pension and

deferred compensation obligations of certain of the German operating companies. The shortfall in external funding continues to be accrued within provisions.

The German schemes are subject to annual valuations, with the last formal valuation prepared at 1 April 2002, which are undertaken by independent

actuaries using the projected unit funding method of valuation. At 1 April 2002, the total pension liability for the internally funded benefits was £121m. The

total pension liability for the externally funded benefits was £7m and the market value of the scheme’s assets for the externally funded benefits also

amounted to £7m.

At 31 March 2003, the estimated liabilities for the externally funded arrangements was £146m and the market value of the trust and other assets

was £95m.

An amount of £64m (2002: £135m) is included in provisions for liabilities and charges, representing the excess of the accumulated pension costs over the

amounts funded externally and reflects the internally funded nature of part of the principal arrangements.

Japan

There are a number of separate pension schemes in relation to employees in Japan and these are not generally funded, with any shortfall in external funding

being accrued within provisions.