US Cellular 2015 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2015 US Cellular annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

Provided all other assumptions remained the same, the Wireline, Cable and HMS discount rates would have to increase

to 7.3%, 10.0% and 13.3%, respectively, to yield estimated fair values equal to their respective carrying values at

November 1, 2015. Further, provided all other assumptions remained the same, the Wireline, Cable and HMS terminal

revenue growth rate assumptions would need to decrease to negative 1.2%, positive 1.6% and negative 2.1%,

respectively, to yield an estimate of fair value equal to the carrying value of the respective reporting units at November 1,

2015.

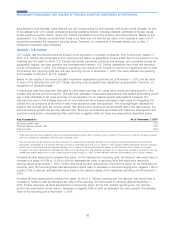

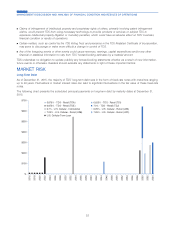

The Goodwill balances of the reporting units tested for impairment as of November 1, 2015 and the percentage by

which the estimated fair value of the corresponding reporting units exceeded their carrying values, as a percentage of

carrying value, was as follows:

Excess of estimated Fair

Reporting unit Goodwill balance Value over Carrying Value

(Dollars in thousands)

Wireline1............................................ $ 408,770 5.9%

Cable ............................................. $ 95,322 7.5%

HMS.............................................. $ 34,830 32.3%

1Between the November 1, 2015 impairment date and the December 31, 2015 Consolidated Balance Sheet date, TDS recorded an immaterial adjustment

to the Goodwill balance related to the divestiture of certain Wireline markets.

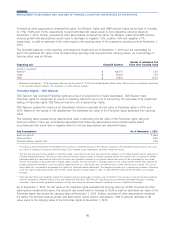

Franchise Rights – TDS Telecom

TDS Telecom has recorded Franchise rights as a result of acquisitions of cable businesses. TDS Telecom tests

Franchise rights for impairment at a level of reporting referred to as a unit of accounting. For purposes of its impairment

testing of Franchise rights, TDS Telecom had one unit of accounting: Cable.

TDS Telecom applied the build-out (or Greenfield) method to estimate the fair value of Franchise rights in 2015 and

2014. Based on the results of this assessment, the estimated fair value of the Franchise rights exceeded their carrying

value.

The following table represents key assumptions used in estimating the fair value of the Franchise rights using the

build-out method. There are uncertainties associated with these key assumptions and potential events and/or

circumstances that could have a negative effect on the key assumptions are described below.

Key Assumptions As of November 1, 2015

Build-out period1....................................................... 2 years

Discount rate2......................................................... 8.0%

Terminal revenue growth rate3............................................... 2.5%

1The build-out period represents the estimated time to perform a hypothetical build of the network. Changes in the estimated build-out period can occur

as a result of changes in resources and technology. Such changes could negatively or positively impact the results.

2The discount rate used in the valuation of Franchise rights is less than the discount rate used in the valuation of the Cable reporting unit for purposes of

Goodwill impairment testing. The discount rate used for Franchise rights includes a reduced company-specific risk premium as it is assumed a market

participant starting a cable network build would construct and operate its network in an optimal manner and would not be constrained by the current

network and operations associated with a mature cable company. The discount rate is estimated based on the overall risk-free interest rate adjusted for

industry participant information, such as a typical capital structure (i.e., debt-equity ratio), the after-tax cost of debt, and the cost of equity. The cost of

equity takes into consideration the average risk specific to individual market participants. The weighted average cost of capital may increase if borrowing

costs rise, market participants weight more of their capital structure towards equity vs. debt, or other elements affecting the estimated cost of equity

increase.

3There are risks that could negatively impact the projected revenue growth rates, including, but not limited to: the success of new and existing products/

services, competition, network buildout costs and operational difficulties. TDS Telecom’s reporting units use internally generated forecasts to develop

such rates. These internally generated forecasts consider such things as observed demand, market factors and competitive knowledge.

As of November 1, 2015, the fair value of the franchise rights exceeded its carrying value by 34.8%. Provided all other

assumptions remained the same, the discount rate would have to increase to 8.5% to yield an estimated fair value of the

Franchise rights that equals the carrying value at November 1, 2015. Further, provided all other assumptions remained

the same, the terminal revenue growth rate assumption would need to decrease to 1.6% to yield an estimate of fair

value equal to the carrying value of the Franchise rights at November 1, 2015.

45

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS