UPS 2011 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2011 UPS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

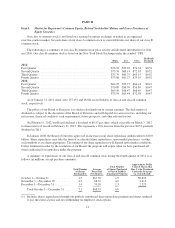

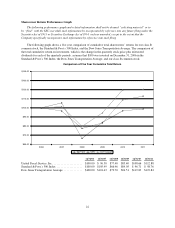

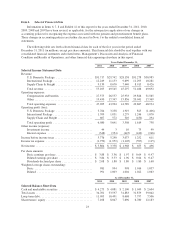

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Overview

The slow pace of the U.S. economic recovery in 2011 put pressure during the first three quarters of the year

on volume and revenue growth in our U.S. Domestic Package segment, as well as U.S. import volume in our

International Package and Supply Chain & Freight segments. Slower growth in industrial production and the lack

of significant inventory rebuilding also pressured our volume in certain industrial sectors; however, overall

growth in retail sales, particularly in e-commerce, resulted in solid business-to-consumer shipment activity

during the year. Growth accelerated in the fourth quarter of 2011 due in large part to a strong holiday season for

e-commerce sales, which resulted in higher volume and revenue for our deferred and ground residential products.

Outside of the U.S., economic growth slowed throughout 2011 due to volatility in world markets. Despite

this sluggish economic environment, we experienced favorable volume and revenue growth for most of the year,

although the growth trend slowed during the latter half of 2011.

In 2011, we continued to undertake initiatives to improve yield management, increase operational efficiency

and contain costs, which led to solid improvements in operating margin and profit in our U.S. Domestic Package

and Supply Chain & Freight segments. During 2010, we completed the second phase of our Worldport expansion

which has allowed the use of larger and more fuel-efficient aircraft, and further improved network efficiencies.

We also streamlined our U.S. domestic management structure and continued to better align our cost structure

with prevailing volume levels.

In our International Package segment, we have continued to invest to support our growth initiatives. In

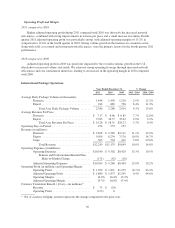

2010, we opened our new intra-Asia air hub in Shenzhen, China, which has allowed us to better serve our

customers by reducing time in transit for shipments in the region. We have also continued to optimize our aircraft

network, to leverage the new route authority we have gained over the last several years and to take full advantage

of faster growing trade lanes. In Asia, we expanded our air network during 2011 by adding flights from Hong

Kong to Cologne, Germany, adding a daily flight from Chengdu, China to Cologne, and adding new routes from

Japan, as well as increasing our capacity to serve the South Korea to U.S. trade lane by adding a flight to and

from Incheon. In Europe, we announced a $200 million expansion of our Cologne hub in Germany in 2011,

which will increase the hub’s sorting capacity from 110,000 to 190,000 packages per hour when completed in

2013. In the Americas, we have expanded our air capacity more than 50% on 19 weekly flights into key markets

in Central and South America during 2011.

Even though we continue to experience solid overall growth in our International Package business, in the

latter half of 2011, we experienced weakness in the important Asia-to-U.S. trade lane. To align our capacity and

cost structure with prevailing volume levels, we reduced our tonnage capacity in this lane, while retaining the

network enhancements and service upgrades previously implemented.

Volatile fuel prices have continued to impact both revenue and expense in all three of our segments. Rising

fuel prices have led to higher fuel surcharge rates and increased fuel and purchased transportation costs.

24