Rogers 2009 Annual Report Download - page 118

Download and view the complete annual report

Please find page 118 of the 2009 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

-

130

|

|

122 ROGERS COMMUNICATIONS INC. 2009 ANNUAL REPORT

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

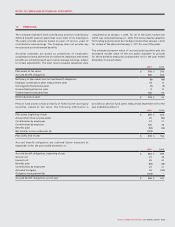

(A) The CRTC collects two different types of fees from broadcast

licensees which are known as Part I and Part II fees. In 2003 and

2004, lawsuits were commenced in the Federal Court alleging

that the Part II licence fees are taxes rather than fees and that the

regulations authorizing them are unlawful. On December 14, 2006,

the Federal Court ruled that the CRTC did not have the jurisdiction

to charge Part II fees. On October 15, 2007, the CRTC sent a letter to

all broadcast licensees stating that the CRTC would not collect Part II

fees due in November 2007. As a result, in the third quarter of 2007,

the Company reversed its accrual of $18 million related to Part II fees

from September 1, 2006 to June 30, 2007. Both the Crown and the

applicants appealed this case to the Federal Court of Appeal. On April

28, 2008, the Federal Court of Appeal overturned the Federal Court

and ruled that Part II fees are valid regulatory charges. As a result,

during the second quarter of 2008, Cable and Media recorded charges

of approximately $30 million and $7 million, respectively, for CRTC

Part II fees covering the period from September 1, 2006 to March 31,

2008. In addition to recording $5 million and $2 million in the second

quarter of 2008 for Cable and Media, respectively, the Company

continued to record these fees on a prospective basis in operating,

general and administrative expenses. Leave to appeal the April 28,

2008 Federal Court of Appeal decision was granted by the Supreme

Court on December 18, 2008. On October 7, 2009, the Government of

Canada announced that a settlement had been reached between the

Government of Canada and members of the broadcasting industry

with respect to Part II fees. Under the terms of the settlement, the

Government agreed to forgive the amounts otherwise owing to it up

to August 31, 2009 and the fees going forward will be approximately

one-third less than historical rates. As a result, during the fourth

quarter of 2009, Cable and Media recorded recoveries in operating,

general and administrative expenses of approximately $60 million

and $19 million, respectively, for CRTC Part II fees covering periods

from September 1, 2006 to August 31, 2009.

(B) In August 2008, a proceeding was commenced in Ontario

pursuant to that province’s Class Proceedings Act, 1992 against

Cable and other providers of communications services in Canada.

The proceedings involve allegations of, among other things, false,

misleading and deceptive advertising relating to charges for long-

distance telephone usage. The plaintiffs are seeking $20 million in

general damages and punitive damages of $5 million. The plaintiffs

intend to seek an order certifying the proceedings as a class action.

Any potential liability is not yet determinable.

(C) In June 2008, a proceeding was commenced in Saskatchewan

under that province’s Class Actions Act against providers of

wireless communications services in Canada. The proceeding

involves allegations of, among other things, breach of contract,

misrepresentation and false advertising in relation to the 911 fee

charged by the Company and the other wireless communication

providers in Canada. The plaintiffs are seeking unquantified

damages and restitution. The plaintiffs intend to seek an order

certifying the proceeding as a national class action in Saskatchewan.

Any potential liability is not yet determinable.

(D) In August 2004, a proceeding under the Class Actions Act

(Saskatchewan) was commenced against providers of wireless

communications in Canada relating to the system access fee charged

by wireless carriers to some of their customers. In September 2007,

the Saskatchewan Court granted the plaintiffs’ application to

have the proceeding certified as a national, “opt-in” class action.

As a national, “opt-in” class action, affected customers outside

Saskatchewan would have to take specific steps to participate in

the proceeding. The Company has applied for leave to appeal the

certification decision to the Saskatchewan Court of Appeal. That

application was later adjourned pending the hearing of certain

motions. In December 2007, the Company brought a motion to

stay the proceeding based on the arbitration clause in its wireless

service agreements. The Company’s motion was granted in February

2008, and the Saskatchewan Court directed that its order in respect

of the certification of the action would exclude from the class of

plaintiffs those customers who are bound by an arbitration clause.

In April 2008, the Class Actions Act (Saskatchewan) was amended to

authorize the certification of national, “opt-out” class actions. In an

“opt-out” class action, affected customers outside of Saskatchewan

would automatically be part of the proceeding in that province. As a

consequence of the amendment, counsel for the plaintiffs brought

a motion to amend the certification order previously granted by the

Saskatchewan Court so as to certify a national, opt-out class action.

In May 2009, the Court refused to grant the requested relief and

dismissed the plaintiffs’ motion. In August 2009, counsel for the

plaintiffs commenced a second proceeding under the Class Actions

Act (Saskatchewan) asserting the same claims against wireless

carriers with respect to the system access fee. In December 2009, the

Court ordered that the second proceeding be conditionally stayed

on the basis that it is an abuse of process. The Company’s application

for leave to appeal the 2007 certification decision in the original

proceeding is currently scheduled to be heard in February 2010. The

Company has not recorded a liability for this contingency since the

likelihood and amount of any potential loss cannot be reasonably

estimated. If the ultimate resolution of this action differs from the

Company’s assessment and assumptions, a material adjustment to

its financial position and results of operations could result.

(E) In April 2004, a proceeding was brought against Fido and other

Canadian wireless carriers claiming damages totalling $160 million,

breach of contract, breach of confidence, breach of fiduciary duty

and, as an alternative to the damages claims, an order for specific

performance of a conditional agreement relating to the use of

38 MHz of MCS Spectrum. In May 2009, the Company settled this

litigation for $4 million, which is included in operating, general and

administrative expenses for the year ended December 31, 2009.

(F) The Company believes that it has adequately provided for

income taxes based on all of the information that is currently

available. The calculation of income taxes in many cases, however,

requires significant judgment in interpreting tax rules and

regulations. The Company’s tax filings are subject to audits, which

could materially change the amount of current and future income

tax assets and liabilities, and could, in certain circumstances, result

in the assessment of interest and penalties.

(G) There exist certain other claims and potential claims against

the Company, none of which is expected to have a material adverse

effect on the consolidated financial position of the Company.

24. CONTINGENT LIABILITIES: