Neiman Marcus 2005 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2005 Neiman Marcus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

|

|

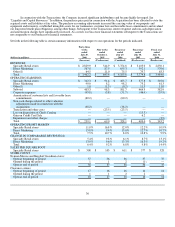

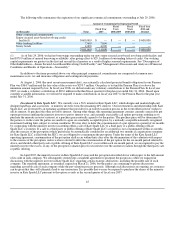

LIQUIDITY AND CAPITAL RESOURCES

Our cash requirements consist principally of:

• the funding of our merchandise purchases;

• capital expenditures for new store construction, store renovations and upgrades of our management information systems;

• debt service requirements;

• income tax payments; and

• obligations related to our Pension Plan.

Our primary sources of short-term liquidity are comprised of cash on hand and availability under our Asset-Based Revolving

Credit Facility. The amounts of cash on hand and borrowings under the Asset-Based Revolving Credit Facility are influenced by a

number of factors, including revenues, working capital levels, vendor terms, the level of capital expenditures, cash requirements related to

financing instruments and debt service obligations following the Transactions, Pension Plan funding obligations and our tax payment

obligations, among others.

Our working capital requirements fluctuate during the fiscal year, increasing substantially during the first and second quarters of

each fiscal year as a result of higher seasonal levels of inventories. We have typically financed the increases in working capital needs

during the first and second fiscal quarters with cash flows from operations and, to a lesser extent, with cash provided from borrowings

under our credit facilities. During fiscal year 2006, we financed our seasonal increases in working capital with cash flows from operations

and borrowings under our Asset-Based Revolving Credit Facility. During the first quarter of fiscal year 2006, we borrowed $150 million

under our Asset-Based Revolving Credit Facility. We repaid these borrowings in the second quarter of fiscal year 2006.

We believe that operating cash flows, available vendor financing and amounts available pursuant to our senior secured Asset-

Based Revolving Credit Facility will be sufficient to fund our operations, anticipated capital expenditure requirements, debt service

obligations, contractual obligations and commitments and Pension Plan funding requirements through the end of fiscal year 2007.

At July 29, 2006, cash and equivalents were $224.8 million compared to $853.4 million at July 30, 2005. This $628.6 million

decrease in cash is primarily due to:

• higher cash balance at July 30, 2005 as a result of the net cash proceeds of $533.7 million received from the Credit

Card Sale in July 2005;

• the use of available cash of approximately $666.1 million in connection with the consummation of the Transactions in

October 2005;

• higher debt and interest requirements in fiscal year 2006, including a $100 million voluntary principal repayment on

the Senior Secured Term Loan Facility made in the second quarter; offset, in part by,

• pretax net cash proceeds of $40.8 million received for the Gurwitch Disposition in July 2006.

Net cash provided by operating activities was $400.2 million in fiscal year 2006 compared to $845.4 million in fiscal year 2005.

Cash flows related to operating activities in fiscal year 2005 were favorably impacted by 1) the $533.7 million net cash proceeds received

by the Predecessor in connection with the Credit Card Sale, partially offset by 2) the funding of a $68.8 million increase in accounts

receivable prior to the Credit Card Sale.

Net cash used for investing activities was $5,286.1 million fiscal year 2006 which consisted of cash outflows of $5,156.4 million

paid to effect the Acquisition and $167.2 million of capital expenditures, partially offset by $40.8 million pretax net cash proceeds

received in connection with the Gurwitch Disposition. Net cash used in investing activities was $228.8 million in fiscal year 2005

primarily for $199.7 million of capital expenditures and $40.7 million cash restricted for the repayment of the outstanding indebtedness

on our Credit Card Facility, offset by $14.4 million in cash proceeds from the sale of

37