Neiman Marcus 2005 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2005 Neiman Marcus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

|

|

approximately $75.4 million in fiscal year 2005. If the Credit Card Sale had been consummated as of the first day of fiscal year 2005, we

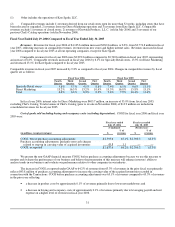

believe the HSBC Program Income for fiscal year 2005 would have been at least $42 million. HSBC and the Company are currently in

the process of implementing changes to the proprietary credit card program that we expect will be fully implemented during the fourth

quarter of fiscal year 2006. Had such changes been fully implemented on the first day of fiscal year 2005, we believe the HSBC Program

Income for fiscal year 2005 would have been approximately $56 million.

Segment operating earnings. Operating earnings for our Specialty Retail stores segment were $377.8 million for fiscal year

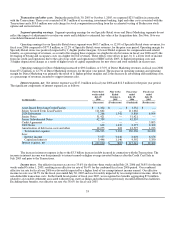

2005 compared to $310.6 million for fiscal year 2004. This 21.6% increase was primarily the result of increased revenues and margins

and net decreases in both buying and occupancy expenses and selling, general and administrative expenses as a percentage of revenues.

Operating earnings for Direct Marketing increased to $75.2 million in fiscal year 2005 from $61.3 million for fiscal year 2004.

This 22.6% increase was primarily the result of increased revenues and margins and net decreases in both buying and occupancy

expenses and selling, general and administrative expenses as a percentage of revenues, partly offset by a higher level of net markdowns.

Interest expense, net. Net interest expense was $12.3 million in fiscal year 2005 and $15.9 million in fiscal year 2004.

The net decrease in net interest expense was due to:

• increases in interest income of $4.4 million generated by higher cash balances; and

• increases in capitalized interest charges of $2.3 million associated with store construction and remodeling activities.

The net decrease in interest expense was offset by a $3.5 million increase in the interest expense attributable to the monthly

distributions to the holders of certain interests issued by a trust in connection with our revolving credit securitization program (the

obligations under which have been transferred as part of the Credit Card Sale). We began charging those distributions to interest expense

in December 2003 as a result of the discontinuance of Off-Balance Sheet Accounting (as defined below under " —Critical Accounting

Policies—Accounts Receivable—Prior to the Credit Card Sale").

Income taxes. Our effective income tax rate was 36.7% for fiscal year 2005 and 36.7% for fiscal year 2004. The income tax

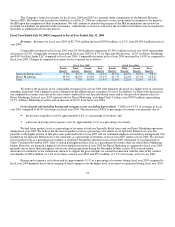

rate for fiscal year 2005 was favorably impacted by tax-exempt interest income, offset by non-deductible transaction costs. In the fourth

fiscal quarter of fiscal year 2005, we recognized tax benefits aggregating $7.6 million related to a favorable settlement associated with

previous state tax filings and reductions in previously recorded deferred tax liabilities. Excluding these benefits, our effective tax rate was

38.6% for fiscal year 2005. In the second fiscal quarter of fiscal year 2004, we also recognized a tax benefit of $7.5 million related to

favorable settlements associated with previous state tax filings. Excluding this benefit, our effective tax rate was 39.0% for fiscal year

2004.

Inflation and Deflation

We believe changes in revenues and net earnings that have resulted from inflation or deflation have not been material during the

periods presented. In recent years, we have experienced certain inflationary conditions related to 1) increases in product costs due

primarily to changes in foreign currency exchange rates that have reduced the purchasing power of the U.S. dollar and 2) increases in

SG&A. We purchase a substantial portion of our inventory from foreign suppliers whose costs are affected by the fluctuation of their

local currency against the dollar or who price their merchandise in currencies other than the dollar. Accordingly, changes in the value of

the dollar relative to foreign currencies may increase our cost of goods sold and if we are unable to pass such cost increases to our

customers, our gross margins, and ultimately our earnings, would decrease. Fluctuations in the euro-U.S. dollar exchange rate affect us

most significantly; however, we source goods from numerous countries and thus are affected by changes in numerous currencies and,

generally, by fluctuations in the U.S. dollar relative to such currencies. Although we hedge some exposures to changes in foreign currency

exchange rates arising in the ordinary course of business, foreign currency fluctuations could have a material adverse effect on our

business, financial condition and results of operations in the future. We attempt to offset the effects of inflation through price increases

and control of expenses, although our ability to increase prices may be limited by competitive factors. We attempt to offset the effects of

merchandise deflation, which has occurred on a limited basis in recent years, through control of expenses. There is no assurance,

however, that inflation or deflation will not materially affect our operations in the future.

36