MetLife 2001 Annual Report Download - page 9

Download and view the complete annual report

Please find page 9 of the 2001 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

|

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations.

For purposes of this discussion, the term ‘‘Company’’ refers, at all times prior to the date of demutualization (as hereinafter defined), to Metropolitan

Life Insurance Company (‘‘Metropolitan Life’’), a mutual life insurance company organized under the laws of the State of New York, and its subsidiaries,

and at all times on and after the date of demutualization, to MetLife, Inc. (the ‘‘Holding Company’’), a Delaware corporation, and its subsidiaries, including

Metropolitan Life. Following this summary is a discussion addressing the consolidated results of operations and financial condition of the Company for the

periods indicated. This discussion should be read in conjunction with the Company’s consolidated financial statements included elsewhere herein.

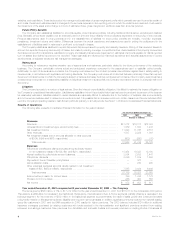

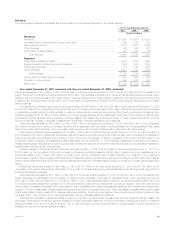

Business Realignment Initiatives

During the fourth quarter of 2001, the Company implemented several business realignment initiatives, which resulted from a strategic review of

operations and an ongoing commitment to reduce expenses. The impact of these actions on a segment basis is as follows:

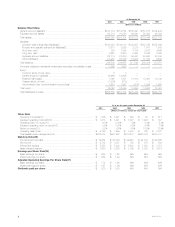

For the Year Ended

December 31, 2001

Net of

Amount Income Tax

(Dollars in millions)

Institutional****************************************************************************** $399 $267

Individual ******************************************************************************* 97 61

Auto & Home *************************************************************************** 32

Total ******************************************************************************* $499 $330

Institutional. The charges to this segment include costs associated with exiting a business, including the write-off of goodwill, severance,

severance-related expenses, and facility consolidation costs. These expenses are the result of the discontinuance of certain 401(k) recordkeeping

services and externally-managed guaranteed index separate accounts. These initiatives will result in the elimination of approximately 450 positions. These

actions resulted in charges to policyholder benefits and claims and other expenses of $215 million and $184 million, respectively.

Individual. The charges to this segment include facility consolidation costs, severance and severance-related expenses, which predominately stem

from the elimination of approximately 560 non-sales positions and 190 operations and technology positions supporting this segment. The costs were

recorded in other expenses.

Auto & Home. The charges to this segment include severance and related costs associated with the elimination of approximately 200 positions.

The costs were recorded in other expenses.

These initiatives are expected to result in savings of approximately $100 million, net of income tax, during 2002, comprised of approximately

$60 million, $35 million and $5 million in the Individual, Institutional and Auto & Home segments, respectively.

Although many of the segments’ underlying business initiatives were completed in 2001, a portion of the activity will continue into 2002. The liability

related to business initiatives at December 31, 2001 was $295 million.

September 11, 2001 Tragedies

On September 11, 2001 a terrorist attack occurred in New York, Washington, D.C. and Pennsylvania (collectively, the ‘‘tragedies’’) triggering a

significant loss of life and property which had an adverse impact on certain of the Company’s businesses. The Company has direct exposures to this

event with claims arising from its Individual, Institutional, Reinsurance and Auto & Home insurance coverages, although it believes the majority of such

claims have been reported or otherwise analyzed by the Company.

As of December 31, 2001, the Company’s estimate of the total expected insurance losses related to the tragedies is $208 million, net of income tax

of $117 million. This estimate is subject to revision in subsequent periods, as claims are received from insureds and the claims to reinsurers are identified

and processed. Any revision to the estimate of gross losses and reinsurance recoveries in subsequent periods will affect income before income taxes

and net income in such periods. Reinsurance recoveries are dependent on the continued creditworthiness of the reinsurers, which may be adversely

affected by their other reinsured losses in connection with the tragedies.

The long-term effects of the tragedies on the Company’s businesses cannot be assessed at this time. The tragedies have had significant adverse

effects on general economic, market and political conditions, increasing many of the Company’s business risks. This may have a negative effect on the

Company’s businesses and results of operations over time. In particular, the declines in share prices experienced after the reopening of the United States

equity markets following the tragedies have contributed, and may continue to contribute, to a decline in separate account assets, which in turn could

have an adverse effect on fees earned in the Company’s businesses. In addition, the Institutional segment may receive disability claims from individuals

suffering from mental and nervous disorders resulting from the tragedies. This may lead to a revision in the Company’s estimated insurance losses related

to the tragedies. The majority of the Company’s disability policies include the provision that such claims be submitted within two years of the traumatic

event.

The Company’s general account investment portfolios include investments, primarily comprised of fixed income securities, in industries that were

affected by the tragedies, including airline, insurance, other travel and lodging and insurance. Exposures to these industries also exist through mortgage

loans and investments in real estate. The market value of the Company’s investment portfolio exposed to industries affected by the tragedies was

approximately $3.0 billion at December 31, 2001.

The Demutualization

On April 7, 2000 (the ‘‘date of demutualization’’), pursuant to an order by the New York Superintendent of Insurance (the ‘‘Superintendent’’) approving

its plan of reorganization, as amended (the ‘‘plan’’), Metropolitan Life converted from a mutual life insurance company to a stock life insurance company

and became a wholly-owned subsidiary of the Holding Company. In conjunction therewith, each policyholder’s membership interest was extinguished

and each eligible policyholder received, in exchange for that interest, trust interests representing shares of Common Stock held in the MetLife

Policyholder Trust, cash or an adjustment to their policy values in the form of policy credits, as provided in the plan. In addition, Metropolitan Life’s

Canadian branch made cash payments to holders of certain policies transferred to Clarica Life Insurance Company in connection with the sale of a

substantial portion of Metropolitan Life’s Canadian operations in 1998, as a result of a commitment made in connection with obtaining Canadian

regulatory approval of that sale. The payments, which were recorded in the second quarter of 2000, were determined in a manner that was consistent

with the treatment of, and fair and equitable to, eligible policyholders of Metropolitan Life.

MetLife, Inc.

6