MetLife 2001 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2001 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

|

|

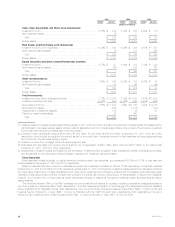

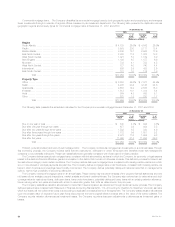

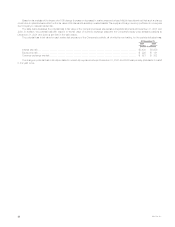

The Company held the following positions in derivative financial instruments at December 31, 2001 and 2000:

2001 2000

Current Market Current Market

or Fair Value or Fair Value

Carrying Notional Carrying Notional

Value Amount Assets Liabilities Value Amount Assets Liabilities

(Dollars in millions)

Financial futures *********************************************** $— $ — $— $— $23 $ 254 $23 $—

Interest rate swaps********************************************* 70 1,849 79 9 41 1,450 41 1

Floors******************************************************** 11 325 11 — — 325 3 —

Caps ******************************************************** 5 7,890 5 — — 9,950 — —

Foreign currency swaps **************************************** 162 1,925 188 26 (1) 1,449 114 44

Exchange traded options**************************************** (12) 1,857 — 12 1 9 1 —

Foreign exchange contracts ************************************* 4674—— ———

Written covered calls ******************************************* —40——— 40——

Credit Default swaps ******************************************* — 270—— — ———

Total contractual commitments ******************************* $240 $14,223 $287 $47 $64 $13,477 $182 $45

Securities Lending

Pursuant to the Company’s securities lending program, it lends securities to major brokerage firms. The Company’s policy requires a minimum of

102% of the fair value of the loaned securities as collateral, calculated on a daily basis. The Company’s securities on loan at December 31, 2001 and

2000 had estimated fair values of $14,404 million and $12,289 million, respectively.

Separate Account Assets

The Company manages each separate account’s assets in accordance with the prescribed investment policy that applies to that specific separate

account. The Company establishes separate accounts on a single client and multi-client commingled basis in conformity with insurance laws. Generally,

separate accounts are not chargeable with liabilities that arise from any other business of the Company. Separate account assets are subject to the

Company’s general account claims only to the extent that the value of such assets exceeds the separate account liabilities, as defined by the account’s

contract. If the Company uses a separate account to support a contract providing guaranteed benefits, the Company must comply with the asset

maintenance requirements stipulated under Regulation 128 of the New York Insurance Department. The Company monitors these requirements at least

monthly and, in addition, performs cash flow analyses, similar to that conducted for the general account, on an annual basis. The Company reports

separately as assets and liabilities investments held in separate accounts and liabilities of the separate accounts. The Company reports substantially all

separate account assets at their fair market value. Investment income and gains or losses on the investments of separate accounts accrue directly to

contract holders, and, accordingly, the Company does not reflect them in its consolidated statements of income and cash flows. The Company reflects

in its revenues fees charged to the separate accounts by the Company, including mortality charges, risk charges, policy administration fees, investment

management fees and surrender charges.

Quantitative and Qualitative Disclosures About Market Risk.

The Company must effectively manage, measure and monitor the market risk associated with its invested assets and interest rate sensitive

insurance contracts. It has developed an integrated process for managing risk, which it conducts through its Corporate Risk Management Department,

several asset/liability committees and additional specialists at the business segment level. The Company has established and implemented comprehen-

sive policies and procedures at both the corporate and business segment level to minimize the effects of potential market volatility.

Market Risk Exposures

The Company has exposure to market risk through its insurance operations and investment activities. For purposes of this disclosure, ‘‘market risk’’

is defined as the risk of loss resulting from changes in interest rates, equity prices and foreign exchange rates.

Interest rates. The Company’s exposure to interest rate changes results from its significant holdings of fixed maturities, as well as its interest rate

sensitive liabilities. The fixed maturities include U.S. and foreign government bonds, securities issued by government agencies, corporate bonds and

mortgage-backed securities, all of which are mainly exposed to changes in medium- and long-term treasury rates. The interest rate sensitive liabilities for

purposes of this disclosure include guaranteed interest contracts and fixed annuities, which have the same interest rate exposure (medium- and long-

term treasury rates) as the fixed maturities. The Company employs product design, pricing and asset/liability management strategies to reduce the

adverse effects of interest rate volatility. Product design and pricing strategies include the use of surrender charges or restrictions on withdrawals in some

products. Asset/liability management strategies include the use of derivatives, the purchase of securities structured to protect against prepayments,

prepayment restrictions and related fees on mortgage loans and consistent monitoring of the pricing of the Company’s products in order to better match

the duration of the assets and the liabilities they support.

Equity prices. The Company’s investments in equity securities expose it to changes in equity prices. It manages this risk on an integrated basis

with other risks through its asset/liability management strategies. The Company also manages equity price risk through industry and issuer diversification

and asset allocation techniques.

Foreign exchange rates. The Company’s exposure to fluctuations in foreign exchange rates against the U.S. dollar results from its holdings in

non-U.S. dollar denominated fixed maturity securities and equity securities and through its investments in foreign subsidiaries. The principal currencies

which create foreign exchange rate risk in the Company’s investment portfolios are Canadian dollars, Euros, Mexican pesos, Chilean pesos and British

pounds. The Company mitigates the majority of its fixed maturities’ foreign exchange rate risk through the utilization of foreign currency swaps and forward

contracts. Through its investments in foreign subsidiaries, the Company is primarily exposed to the Euro, Mexican peso and South Korean won. The

Company has denominated substantially all assets and liabilities of its foreign subsidiaries in their respective local currencies, thereby minimizing its risk to

foreign exchange rate fluctuations.

Risk Management

Corporate risk management. MetLife has established several financial and non-financial senior management committees as part of its risk

management process. These committees manage capital and risk positions, approve asset/liability management strategies and establish appropriate

corporate business standards.

MetLife, Inc.

34