MetLife 2001 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2001 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

|

|

METLIFE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

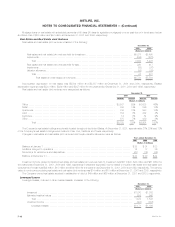

Income Taxes

The Holding Company and its includable life insurance and non-life insurance subsidiaries file a consolidated U.S. federal income tax return in

accordance with the provisions of the Internal Revenue Code of 1986, as amended (the ‘‘Code’’). Non-includable subsidiaries file either separate tax

returns or separate consolidated tax returns. Under the Code, the amount of federal income tax expense incurred by mutual life insurance companies

includes an equity tax calculated based upon a prescribed formula that incorporates a differential earnings rate between stock and mutual life insurance

companies. Metropolitan Life has not been subject to the equity tax since the date of demutualization. The future tax consequences of temporary

differences between financial reporting and tax bases of assets and liabilities are measured at the balance sheet dates and are recorded as deferred

income tax assets and liabilities.

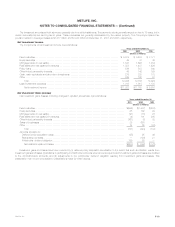

Reinsurance

The Company has reinsured certain of its life insurance and property and casualty insurance contracts with other insurance companies under

various agreements. Amounts due from reinsurers are estimated based upon assumptions consistent with those used in establishing the liabilities related

to the underlying reinsured contracts. Policy and contract liabilities are reported gross of reinsurance credits. Deferred policy acquisition costs are

reduced by amounts recovered under reinsurance contracts. Amounts received from reinsurers for policy administration are reported in other revenues.

The Company assumes and retrocedes financial reinsurance contracts, which represent low mortality risk reinsurance treaties. These contracts are

reported as deposits and are included in other assets. The amount of revenue reported on these contracts represents fees and the cost of insurance

under the terms of the reinsurance agreement.

Separate Accounts

Separate accounts are established in conformity with insurance laws and are generally not chargeable with liabilities that arise from any other

business of the Company. Separate account assets are subject to general account claims only to the extent the value of such assets exceeds the

separate account liabilities. Investments (stated at estimated fair value) and liabilities of the separate accounts are reported separately as assets and

liabilities. Deposits to separate accounts, investment income and recognized and unrealized gains and losses on the investments of the separate

accounts accrue directly to contractholders and, accordingly, are not reflected in the Company’s consolidated statements of income and cash flows.

Mortality, policy administration and surrender charges to all separate accounts are included in revenues.

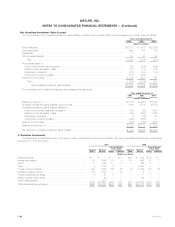

Stock Based Compensation

The Company accounts for the stock-based compensation plans using the accounting method prescribed by Accounting Principles Board Opinion

No. 25, Accounting for Stock Issued to Employees (‘‘APB 25’’) and has included in the notes to consolidated financial statements the pro forma

disclosures required by Statement of Financial Accounting Standards No. 123, Accounting for Stock-Based Compensation (‘‘SFAS 123’’) in Note 17.

Foreign Currency Translation

Balance sheet accounts of foreign operations are translated at the exchange rates in effect at each year-end and income and expense accounts are

translated at the average rates of exchange prevailing during the year. The local currencies of foreign operations are the functional currencies unless the

local economy is highly inflationary. Translation adjustments are charged or credited directly to other comprehensive income or loss. Gains and losses

from foreign currency transactions are reported in earnings.

Earnings Per Share

Earnings per share amounts, on a basic and diluted basis, have been calculated based upon the weighted average common shares outstanding or

deemed to be outstanding only for the period after the date of demutualization.

Basic earnings per share is computed based on the weighted average number of shares outstanding during the period. Diluted earnings per share

includes the dilutive effect of the assumed conversion of forward purchase contracts and exercise of stock options, using the treasury stock method.

Under the treasury stock method, exercise of the forward purchase contracts is assumed with the proceeds used to purchase common stock at the

average market price for the period. The difference between the number of shares assumed issued and number of shares assumed purchased

represents the dilutive shares.

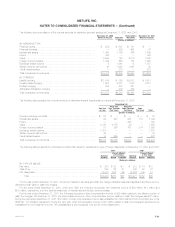

Demutualization and Initial Public Offering

On April 7, 2000 (the ‘‘date of demutualization’’), Metropolitan Life Insurance Company (‘‘Metropolitan Life’’) converted from a mutual life insurance

company to a stock life insurance company and became a wholly-owned subsidiary of MetLife, Inc. The conversion was pursuant to an order by the New

York Superintendent of Insurance (the ‘‘Superintendent’’) approving Metropolitan Life’s plan of reorganization, as amended (the ‘‘plan’’).

On the date of demutualization, policyholders’ membership interests in Metropolitan Life were extinguished and eligible policyholders received, in

exchange for their interests, trust interests representing 494,466,664 shares of common stock of MetLife, Inc. to be held in a trust, cash payments

aggregating $2,550 million and adjustments to their policy values in the form of policy credits aggregating $408 million, as provided in the plan. In

addition, Metropolitan Life’s Canadian branch made cash payments of $327 million in the second quarter of 2000 to holders of certain policies

transferred to Clarica Life Insurance Company in connection with the sale of a substantial portion of Metropolitan Life’s Canadian operations in 1998, as a

result of a commitment made in connection with obtaining Canadian regulatory approval of that sale.

Application of Accounting Pronouncements

Effective January 1, 2001, the Company adopted SFAS 133 which established new accounting and reporting standards for derivative instruments,

including certain derivative instruments embedded in other contracts, and for hedging activities. The cumulative effect of the adoption of SFAS 133, as of

January 1, 2001, resulted in a $33 million increase in other comprehensive income, net of income taxes of $18 million, and had no material impact on net

income. The increase to other comprehensive income is attributable to net gains on cash flow-type hedges at transition. Also at transition, the amortized

cost of fixed income securities decreased and other invested assets increased by $22 million, representing the fair value of certain interest rate swaps

that were accounted for prior to SFAS 133 using fair value-type settlement accounting. During the year ended December 31, 2001, $18 million of the

pre-tax gain reported in accumulated other comprehensive income at transition was reclassified into net investment income. The FASB continues to issue

MetLife, Inc. F-13