MetLife 2001 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2001 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

|

|

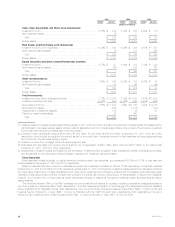

The principal risks inherent in holding mortgage-backed securities are prepayment, extension and collateral risks, which will affect the timing of when

cash flow will be received. The Company’s active monitoring of its mortgage-backed securities mitigates exposure to losses from cash flow risk

associated with interest rate fluctuations.

Asset-backed securities. Asset-backed securities, which include home equity loans, credit card receivables, collateralized debt obligations and

automobile receivables, are purchased both to diversify the overall risks of the Company’s fixed maturities assets and to provide attractive returns. The

Company’s asset-backed securities are diversified both by type of asset and by issuer. Home equity loans constitute the largest exposure in the

Company’s asset-backed securities investments. Except for asset-backed securities backed by home equity loans, the asset-backed securities

investments generally have little sensitivity to changes in interest rates. Approximately $3,427 million and $3,149 million, or 42.1% and 40.1%, of total

asset-backed securities were rated Aaa/AAA by Moody’s or S&P at December 31, 2001 and 2000, respectively.

The principal risks in holding asset-backed securities are structural, credit and capital market risks. Structural risks include the security’s priority in the

issuer’s capital structure, the adequacy of and ability to realize proceeds from the collateral and the potential for prepayments. Credit risks include

consumer or corporate credits such as credit card holders, equipment lessees, and corporate obligors. Capital market risks include the general level of

interest rates and the liquidity for these securities in the marketplace.

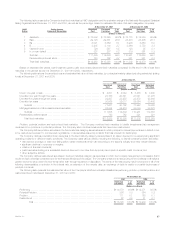

Structured investment transactions. The Company participates in structured investment transactions as part of its risk management strategy,

including asset liability management, and to enhance the Company’s total return on its investment portfolio. These investments are predominately made

through bankruptcy-remote SPEs, which generally acquire financial assets, including corporate equities, debt securities and purchased options. These

investments are referred to as beneficial interests.

The Company’s exposure to losses related to these SPEs is limited to its carrying value since the Company has not guaranteed the performance,

liquidity or obligations of the SPEs. As prescribed by GAAP, the Company does not consolidate such SPEs since unrelated third parties hold controlling

interests through ownership of the SPEs’ equity, representing at least three percent of the total assets of the SPE throughout the life of the SPE, and such

equity class has the substantive risks and rewards of the residual interests in the SPE.

The Company also sponsors financial asset securitizations of high yield debt securities, investment grade bonds and structured finance securities

and also is the collateral manager and a beneficial interest holder in such transactions. As the collateral manager, the Company earns a management fee

on the outstanding securitized asset balance. When the Company transfers assets to an SPE and surrenders control over the transferred assets, the

transaction is accounted for as a sale. Gains or losses on securitizations are determined with reference to the carrying amount of the financial assets

transferred, which is allocated to the assets sold and the beneficial interests retained based on relative fair values at the date of transfer. The Company

has sponsored four securitizations with a total of approximately $1.5 billion in financial assets as of December 31, 2001. Two of these transactions, which

were executed in 2001, included the transfer of assets totaling approximately $289 million which resulted in the recognition of an insignificant amount of

investment gains. The Company’s beneficial interests in these SPEs and the related investment income were insignificant as of and for the years ended

December 31, 2001 and 2000.

The Company also invests in structured investment transactions which are managed and controlled by unrelated third parties. In instances where the

Company exercises significant influence over the operating and financial policies of an SPE, the beneficial interests are accounted for in accordance with

the equity method of accounting. Where the Company does not exercise significant influence, the structure of the beneficial interests (i.e., debt or equity

securities) determines the method of accounting for the investment. Such beneficial interests generally are structured notes, which are classified as fixed

maturities, and the related income is recognized using the retrospective interest method. Beneficial interests other than structured notes are also

classified as fixed maturities, and the related income is recognized using the level yield method. The carrying value of all such investments was

approximately $1.6 billion and $1.3 billion at December 31, 2001 and 2000, respectively. The related income recognized was $44 million and $62 million

for the years ended December 31, 2001 and 2000, respectively.

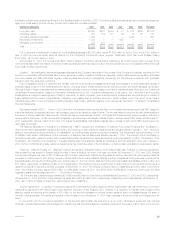

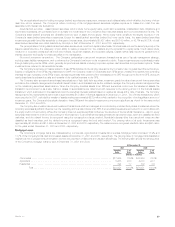

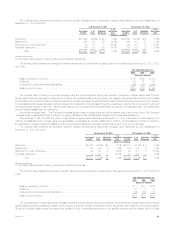

Mortgage Loans

The Company’s mortgage loans are collateralized by commercial, agricultural and residential properties. Mortgage loans comprised 13.9% and

13.7% of the Company’s total cash and invested assets at December 31, 2001 and 2000, respectively. The carrying value of mortgage loans is stated at

original cost net of prepayments, amortization of premiums, accretion of discounts and valuation allowances. The following table shows the carrying value

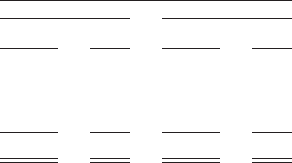

of the Company’s mortgage loans by type at December 31, 2001 and 2000:

At December 31,

2001 2000

Carrying % of Carrying % of

Value Total Value Total

(Dollars in millions)

Commercial ********************************************************************* $17,959 76.0% $16,869 76.8%

Agricultural ********************************************************************** 5,268 22.3 4,973 22.7

Residential ********************************************************************** 394 1.7 109 0.5

Total ******************************************************************* $23,621 100.0% $21,951 100.0%

MetLife, Inc. 29