MetLife 2001 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2001 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

|

|

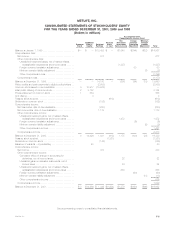

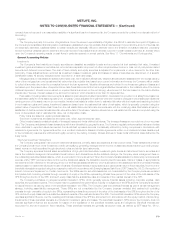

METLIFE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

The Company enters into written covered call options and net written covered collars to generate additional investment income on the underlying

assets it holds. These derivatives are not designated as hedges. The Company records the premiums received as net investment income over the life of

the contract and changes in fair value of such options and collars as net investment gains and losses.

Cash and Cash Equivalents

The Company considers all investments purchased with an original maturity of three months or less to be cash equivalents.

Property, Equipment, Leasehold Improvements and Computer Software

Property, equipment and leasehold improvements, which are included in other assets, are stated at cost, less accumulated depreciation and

amortization. Depreciation is determined using either the straight-line or sum-of-the-years-digits method over the estimated useful lives of the assets.

Estimated lives range from ten to 40 years for leasehold improvements and three to 15 years for all other property and equipment. Accumulated

depreciation of property and equipment and accumulated amortization on leasehold improvements was $1,352 million and $1,287 million at Decem-

ber 31, 2001 and 2000, respectively. Related depreciation and amortization expense was $97 million, $89 million and $106 million for the years ended

December 31, 2001, 2000 and 1999, respectively.

Computer software, which is included in other assets, is stated at cost, less accumulated amortization. Purchased software costs, as well as internal

and external costs incurred to develop internal-use computer software during the application development stage, are capitalized. Such costs are

amortized generally over a three-year period using the straight-line method. Accumulated amortization of capitalized software was $169 million and

$86 million at December 31, 2001 and 2000, respectively. Related amortization expense was $110 million, $45 million and $5 million for the years ended

December 31, 2001, 2000 and 1999, respectively.

Deferred Policy Acquisition Costs

The costs of acquiring new insurance business that vary with, and are primarily related to, the production of new business are deferred. Such costs,

which consist principally of commissions, agency and policy issue expenses, are amortized with interest over the expected life of the contract for

participating traditional life, universal life and investment-type products. Generally, deferred policy acquisition costs are amortized in proportion to the

present value of estimated gross margins or profits from investment, mortality, expense margins and surrender charges. Interest rates are based on rates

in effect at the inception or acquisition of the contracts. Actual gross margins or profits can vary from management’s estimates resulting in increases or

decreases in the rate of amortization. Management periodically updates these estimates and evaluates the recoverability of deferred policy acquisition

costs. When appropriate, management revises its assumptions of the estimated gross margins or profits of these contracts, and the cumulative

amortization is re-estimated and adjusted by a cumulative charge or credit to current operations.

Deferred policy acquisition costs for non-participating traditional life, non-medical health and annuity policies with life contingencies are amortized in

proportion to anticipated premiums. Assumptions as to anticipated premiums are made at the date of policy issuance or acquisition and are consistently

applied during the lives of the contracts. Deviations from estimated experience are included in operations when they occur. For these contracts, the

amortization period is typically the estimated life of the policy.

Deferred policy acquisition costs related to internally replaced contracts are expensed at the date of replacement.

Deferred policy acquisition costs for property and casualty insurance contracts, which are primarily comprised of commissions and certain

underwriting expenses, are deferred and amortized on a pro rata basis over the applicable contract term or reinsurance treaty.

Value of business acquired, included as part of deferred policy acquisition costs, represents the present value of future profits generated from

existing insurance contracts in force at the date of acquisition and is amortized over the expected policy or contract duration in relation to the present

value of estimated gross profits from such policies and contracts.

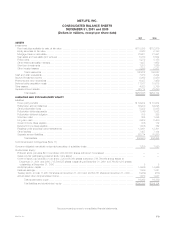

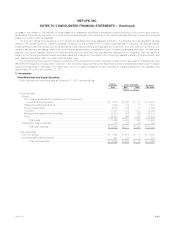

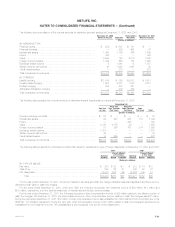

Information regarding deferred policy acquisition costs is as follows:

Years ended December 31

2001 2000 1999

(Dollars in millions)

Balance at January 1 ******************************************************************** $10,618 $ 9,070 $ 7,028

Capitalization of policy acquisition costs ***************************************************** 2,039 1,863 1,160

Value of business acquired**************************************************************** 102 1,681 156

Total*************************************************************************** 12,759 12,614 8,344

Amortization allocated to:

Net investment losses ****************************************************************** 25 (95) (46)

Unrealized investment losses ************************************************************ 140 590 (1,628)

Other expenses *********************************************************************** 1,413 1,478 930

Total amortization **************************************************************** 1,578 1,973 (744)

Dispositions and other******************************************************************** (14) (23) (18)

Balance at December 31 ***************************************************************** $11,167 $10,618 $ 9,070

Amortization of deferred policy acquisition costs is allocated to (i) investment gains and losses to provide consolidated statement of income

information regarding the impact of such gains and losses on the amount of the amortization, (ii) unrealized investment gains and losses to provide

information regarding the amount of deferred policy acquisition costs that would have been amortized if such gains and losses had been recognized, and

(iii) other expenses to provide amounts related to the gross margins or profits originating from transactions other than investment gains and losses.

Investment gains and losses related to certain products have a direct impact on the amortization of deferred policy acquisition costs. Presenting

investment gains and losses net of related amortization of deferred policy acquisition costs provides information useful in evaluating the operating

performance of the Company. This presentation may not be comparable to presentations made by other insurers.

MetLife, Inc. F-11