MetLife 2001 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2001 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

|

|

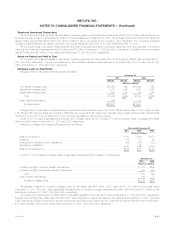

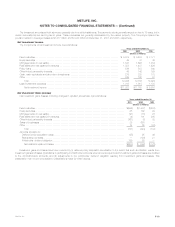

METLIFE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

contract does not expose it to a reasonable possibility of a significant loss from insurance risk, the Company records the contract on a deposit method of

accounting.

Litigation

The Company is a party to a number of legal actions. Given the inherent unpredictability of litigation, it is difficult to estimate the impact of litigation on

the Company’s consolidated financial position. Liabilities are established when it is probable that a loss has been incurred and the amount of the loss can

be reasonably estimated. Liabilities related to certain lawsuits are especially difficult to estimate due to the limitation of available data and uncertainty

around numerous variables used to determine amounts recorded. It is possible that an adverse outcome in certain cases could have an adverse effect

upon the Company’s operating results or cash flows in particular quarterly or annual periods. See Note 11 ‘‘Commitments and Contingencies.’’

General Accounting Policies

Investments

The Company’s fixed maturity and equity securities are classified as available-for-sale and are reported at their estimated fair value. Unrealized

investment gains and losses on securities are recorded as a separate component of other comprehensive income or loss, net of policyholder related

amounts and deferred income taxes. The cost of fixed maturity and equity securities is adjusted for impairments in value deemed to be other than

temporary. These adjustments are recorded as investment losses. Investment gains and losses on sales of securities are determined on a specific

identification basis. All security transactions are recorded on a trade date basis.

Mortgage loans on real estate are stated at amortized cost, net of valuation allowances. Valuation allowances are established for the excess carrying

value of the mortgage loan over its estimated fair value when it is probable that, based upon current information and events, the Company will be unable

to collect all amounts due under the contractual terms of the loan agreement. Valuation allowances are included in net investment gains and losses and

are based upon the present value of expected future cash flows discounted at the loan’s original effective interest rate or the collateral value if the loan is

collateral dependent. Interest income earned on impaired loans is accrued on the net carrying value amount of the loan based on the loan’s effective

interest rate. However, interest ceases to be accrued for loans on which interest is more than 60 days past due.

Real estate, including related improvements, is stated at cost less accumulated depreciation. Depreciation is provided on a straight-line basis over

the estimated useful life of the asset (typically 20 to 40 years). Cost is adjusted for impairment whenever events or changes in circumstances indicate the

carrying amount of the asset may not be recoverable. Impaired real estate is written down to estimated fair value with the impairment loss being included

in net investment gains and losses. Impairment losses are based upon the estimated fair value of real estate, which is generally computed using the

present value of expected future cash flows from the real estate discounted at a rate commensurate with the underlying risks. Real estate acquired in

satisfaction of debt is recorded at estimated fair value at the date of foreclosure. Valuation allowances on real estate held-for-sale are computed using the

lower of depreciated cost or estimated fair value, net of disposition costs.

Policy loans are stated at unpaid principal balances.

Short-term investments are stated at amortized cost, which approximates fair value.

Other invested assets consist principally of leveraged leases and funds withheld at interest. The leveraged leases are recorded net of non-recourse

debt. The Company participates in lease transactions which are diversified by geographic area. The Company regularly reviews residual values and writes

down residuals to expected values as needed. Funds withheld represent amounts contractually withheld by ceding companies in accordance with

reinsurance agreements. For agreements written on a modified coinsurance basis and certain agreements written on a coinsurance basis, assets equal

to the net statutory reserves are withheld and legally owned by the ceding company. Interest accrues to these funds withheld at rates defined by the

treaty terms.

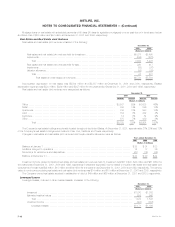

Structured Investment Transactions

The Company participates in structured investment transactions, primarily asset securitizations and structured notes. These transactions enhance

the Company’s total return of the investment portfolio principally by generating management fee income on asset securitizations and by providing equity-

based returns on debt securities through structured notes and similar type instruments.

The Company sponsors financial asset securitizations of high yield debt securities, investment grade bonds and structured finance securities and

also is the collateral manager and a beneficial interest holder in such transactions. As the collateral manager, the Company earns management fees on

the outstanding securitized asset balance, which are recorded in income as earned. When the Company transfers assets to a bankruptcy-remote special

purpose entity (‘‘SPE’’) and surrenders control over the transferred assets, the transaction is accounted for as a sale. Gains or losses on securitizations

are determined with reference to the carrying amount of the financial assets transferred, which is allocated to the assets sold and the beneficial interests

retained based on relative fair values at the date of transfer. Beneficial interests in securitizations are carried at fair value in fixed maturities. Income on the

beneficial interests is recognized using the prospective method in accordance with Emerging Issues Task Force (‘‘EITF’’) Issue No. 99-20, Recognition of

Interest Income and Impairment on Certain Investments. The SPEs used to securitize assets are not consolidated by the Company because unrelated

third parties hold controlling interests through ownership of equity in the SPEs, representing at least three percent of the value of the total assets of the

SPE throughout the life of the SPE, and such equity class has the substantive risks and rewards of the residual interest of the SPE.

The Company purchases or receives beneficial interests in SPEs, which generally acquire financial assets including corporate equities, debt

securities and purchased options. The Company has not guaranteed the performance, liquidity or obligations of the SPEs and the Company’s exposure

to loss is limited to its carrying value of the beneficial interests in the SPEs. The Company uses the beneficial interests as part of its risk management

strategy, including asset-liability management. These SPEs are not consolidated by the Company because unrelated third parties hold controlling

interests through ownership of equity in the SPEs, representing at least three percent of the value of the total assets of the SPE throughout the life of the

SPE, and such equity class has the substantive risks and rewards of the residual interest of the SPE. The beneficial interests in SPEs where the Company

exercises significant influence over the operating and financial policies of the SPE are accounted for in accordance with the equity method of accounting.

Impairments of these beneficial interests are included in investment gains and losses. The beneficial interests in SPEs where the Company does not

exercise significant influence are accounted for based on the substance of the beneficial interest’s rights and obligations. Beneficial interests are

accounted for and are included in fixed maturities. These beneficial interests are generally structured notes, as defined by EITF Issue No. 96-12,

MetLife, Inc. F-9