MetLife 2001 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2001 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

|

|

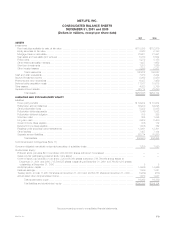

METLIFE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

1. Summary of Significant Accounting Policies

Business

MetLife, Inc. (the ‘‘Holding Company’’) and its subsidiaries (together with the Holding Company, ‘‘MetLife’’ or the ‘‘Company’’) is a leading provider of

insurance and financial services to a broad section of individual and institutional customers. The Company offers life insurance, annuities and mutual

funds to individuals and group insurance, reinsurance and retirement and savings products and services to corporations and other institutions.

Basis of Presentation

The accompanying consolidated financial statements include the accounts of the Holding Company and its subsidiaries, partnerships and joint

ventures in which the Company has a majority voting interest or general partner interest with limited removal rights by limited partners. Closed block

assets, liabilities, revenues and expenses are combined on a line by line basis with the assets, liabilities, revenues and expenses outside the closed

block based on the nature of the particular item. Intercompany accounts and transactions have been eliminated.

The Company uses the equity method to account for its investments in real estate joint ventures and other limited partnership interests in which it

does not have a controlling interest, but has more than a minimal interest.

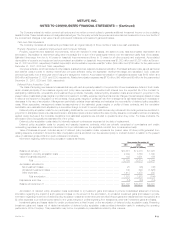

Minority interest related to consolidated entities included in other liabilities was $442 million and $409 million at December 31, 2001 and 2000,

respectively.

Certain amounts in the prior years’ consolidated financial statements have been reclassified to conform with the 2001 presentation.

Summary of Critical Accounting Policies

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America (‘‘GAAP’’) requires

management to adopt accounting policies and make estimates and assumptions that affect amounts reported in the consolidated financial statements.

The critical accounting policies and related judgments underlying the Company’s consolidated financial statements are summarized below. In applying

these policies, management makes subjective and complex judgments that frequently require estimates about matters that are inherently uncertain. Many

of these policies are common in the insurance and financial services industries; others are specific to the Company’s businesses and operations.

Investments

The Company’s principal investments are in fixed maturities, mortgage loans and real estate, all of which are exposed to three primary sources of

investment risk: credit, interest rate and market valuation. The financial statement risks are those associated with the recognition of income, impairments

and the determination of fair values. In addition, the earnings on certain investments are dependent upon market conditions which could result in

prepayments and changes in amounts to be earned due to changing interest rates or equity markets.

Derivatives

The Company enters into freestanding derivative transactions to manage the risk associated with variability in cash flows related to the Company’s

financial assets and liabilities or to changing fair values. The Company also purchases investment securities and issues certain insurance policies with

embedded derivatives. The associated financial statement risk is the volatility in net income, which can result from (i) changes in fair value of derivatives

that are not designated as hedges, and (ii) ineffectiveness of designated hedges in an environment of changing interest rates or fair values. In addition,

accounting for derivatives is complex, as evidenced by significant interpretations of the primary accounting standards which continue to evolve, as well as

the significant judgments and estimates involved in determining fair value in the absence of quoted market values. These estimates are based on

valuation methodologies and assumptions deemed appropriate in the circumstances; however, the use of different assumptions may have a material

effect on the estimated fair value amounts.

Deferred Policy Acquisition Costs

The Company incurs significant costs in connection with acquiring new insurance business. These costs, which vary with, and are primarily related

to, the production of new business, are deferred. The recovery of such costs is dependent on the future profitability of the related business. The amount

of future profit is dependent principally on investment returns, mortality, morbidity, persistency, expenses to administer the business (and additional

charges to the policyholders) and certain economic variables, such as inflation. These factors enter into management’s estimates of gross margins and

profits which generally are used to amortize certain of such costs. Revisions to estimates result in changes to the amounts expensed in the reporting

period in which the revisions are made and could result in the impairment of the asset and a charge to income if estimated future gross margins and

profits are less than amounts deferred.

Future Policy Benefits

The Company also establishes liabilities for amounts payable under insurance policies, including traditional life insurance, annuities and disabled

lives. Generally, amounts are payable over an extended period of time and the profitability of the products is dependent on the pricing of the products.

Principal assumptions used in pricing policies and in the establishment of liabilities for future policy benefits are mortality, morbidity, expenses,

persistency, investment returns and inflation. Differences between the actual experience and assumptions used in pricing the policies and in the

establishment of liabilities result in variances in profit and could result in losses.

The Company establishes liabilities for unpaid claims and claims expenses for property and casualty insurance. Pricing of this insurance takes into

account the expected frequency and severity of losses, the costs of providing coverage, competitive factors, characteristics of the property covered and

the insured, and profit considerations. Liabilities for property and casualty insurance are dependent on estimates of amounts payable for claims reported

but not settled and claims incurred but not reported. These estimates are influenced by historical experience and actuarial assumptions of current

developments, anticipated trends and risk management strategies.

Reinsurance

Accounting for reinsurance requires extensive use of assumptions and estimates, particularly related to the future performance of the underlying

business. The Company periodically reviews actual and anticipated experience compared to the assumptions used to establish policy benefits.

Additionally, for each of its reinsurance contracts, the Company must determine if the contract provides indemnification against loss or liability relating to

insurance risk, in accordance with applicable accounting standards. The Company must review all contractual features, particularly those that may limit

the amount of insurance risk to which the Company is subject or features that delay the timely reimbursement of claims. If the Company determines that a

MetLife, Inc.

F-8