MetLife 2001 Annual Report Download - page 13

Download and view the complete annual report

Please find page 13 of the 2001 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

|

|

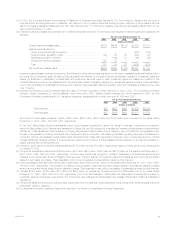

dental, disability and long-term care insurance businesses, commensurate with the variance in premiums, partially offset by a decrease in policyholder

benefits and claims related to the retirement and savings business. Policyholder benefits and claims for the Reinsurance segment rose by $388 million

due to unfavorable mortality experience in the first and fourth quarters of 2001, as well as adverse results on the reinsurance of Argentine pension

business, reflecting the impact of recent economic and political events in that country. In addition, reinsurance claims arising from the September 11,

2001 tragedies of approximately $16 million, net of amounts recoverable from reinsurers, contributed to the variance. A $179 million rise in the Individual

segment is primarily the result of an increase in the liabilities for future policy benefits commensurate with the aging of the in-force block of business. In

addition, an increase of $74 million in the policyholder dividend obligation and $24 million in liabilities and claims associated with the September 11, 2001

tragedies contributed to the variance. International policyholder benefits and claims increased by $127 million as a result of growth in Mexico, South

Korea and Taiwan, as well as acquisitions in Brazil and Chile. These fluctuations are partially offset by a decline in Argentina, reflecting the impact of recent

economic and political events in that country. A $116 million increase in the Auto & Home segment is predominately the result of increased average claim

costs, growth in the auto business and increased non-catastrophe weather-related losses.

Interest credited to policyholder account balances grew by $149 million, or 5%, to $3,084 million for the year ended December 31, 2001 from

$2,935 million for the comparable 2000 period, primarily due to an increase of $218 million in the Individual segment, partially offset by a $77 million

reduction in the Institutional segment. The establishment of a policyholder liability of $118 million with respect to certain group annuity contracts at New

England Financial is the primary driver of the fluctuation in Individual. In addition, higher average policyholder account balances and slightly increased

crediting rates contributed to the variance. The decrease in the Institutional segment is primarily due to an overall decline in crediting rates in 2001 as a

result of the current interest rate environment, partially offset by an increase in average customer account balances stemming from asset growth. The

remaining variance is due to minor fluctuations in the Reinsurance and International segments.

Policyholder dividends increased by $167 million, or 9%, to $2,086 million for the year ended December 31, 2001 from $1,919 million for the

comparable 2000 period, primarily due to increases of $135 million and $25 million in the Institutional and Individual segments, respectively. The rise in

the Institutional segment is primarily attributed to favorable experience on a large group life contract in 2001. Policyholder dividends vary from period to

period based on participating contract experience. The change in the Individual segment reflects growth in the assets supporting policies associated with

this segment’s aging block of traditional life insurance business. The remaining variance is due to minor fluctuations in the International and Reinsurance

segments.

Payments of $327 million were made during the second quarter of 2000, as part of Metropolitan Life’s demutualization, to holders of certain policies

transferred to Clarica Life Insurance Company in connection with the sale of a substantial portion of the Canadian operations in 1998.

Demutualization costs of $230 million were incurred during the year ended December 31, 2000. These costs are related to Metropolitan Life’s

demutualization on April 7, 2000.

Other expenses decreased by $459 million, or 6%, to $7,565 million for the year ended December 31, 2001 from $8,024 million for the comparable

2000 period. Excluding the capitalization and amortization of deferred policy acquisition costs, which are discussed below, other expenses declined by

$218 million, or 3%, to $8,191 million in 2001 from $8,409 million in 2000. This variance is attributable to reductions in the Asset Management, Individual

and Auto & Home segments, partially offset by increases in the other segments. A decrease of $532 million in the Asset Management segment is

predominately the result of the sales of Nvest and Conning on October 30, 2000 and July 2, 2001, respectively. The Individual segment’s expenses

declined by $167 million due to continued expense management, primarily due to reduced employee costs and lower discretionary spending. In

addition, there were reductions in volume-related commission expenses in the broker/dealer and other subsidiaries and rebate expenses associated with

the Company’s securities lending program. The income associated with securities lending activity is included in net investment income. These items are

partially offset by an increase of $97 million related to fourth quarter 2001 business realignment initiatives. A $34 million decrease in Auto & Home is

attributable to a reduction in integration costs associated with the acquisition of the standard personal lines property and casualty insurance operations of

The St. Paul Companies in September 1999 (‘‘St. Paul acquisition’’). An increase of $232 million in Institutional expenses is primarily driven by expenses

associated with fourth quarter business realignment initiatives of $184 million and a rise in non-deferrable variable expenses associated with premium

growth in the group insurance businesses. Non-deferrable variable expenses include premium tax, commissions and administrative expenses for dental,

disability and long-term care businesses. These increases are partially offset by a decline in rebate expenses associated with the Company’s securities

lending program. The income associated with securities lending activity is included in net investment income. The income associated with securities

lending activity is included in net investment income. Other expenses in Corporate & Other grew by $219 million primarily due to a $250 million

race-conscious underwriting loss provision which was recorded in the fourth quarter of 2001, as well as $29 million of additional expenses associated

with MetLife, Inc. shareholder services costs and start-up costs relating to MetLife’s banking initiatives. These increases are partially offset by a

$58 million decline in interest expense due to reduced average levels of borrowing and a lower interest rate environment in 2001. An increase of

$43 million in the International segment is predominately the result of growth in Mexico and South Korea, and acquisitions in Brazil and Chile, partially

offset by a decrease in Spain’s other expenses due to a planned cessation of product lines offered through a joint venture with Banco Santander. The

acquisition of the remaining interest in RGA Financial Group, LLC during the second half of 2000 contributed to the $20 million increase in other

expenses in the Reinsurance segment.

Deferred policy acquisition costs are principally amortized in proportion to gross margins or profits, including investment gains or losses. The

amortization is allocated to investment gains and losses to provide consolidated statement of income information regarding the impact of investment

gains and losses on the amount of the amortization, and other expenses to provide amounts related to gross margins or profits originating from

transactions other than investment gains and losses.

Capitalization of deferred policy acquisition costs increased to $2,039 million for the year ended December 31, 2001 from $1,863 million for the

comparable 2000 period. This variance is attributable to increases in the Individual, Reinsurance, Institutional and International segments. The growth in

the Individual segment is primarily due to higher sales of variable and universal life insurance policies and annuity and investment-type products, resulting

in additional commissions and other deferrable expenses. The increases in the Reinsurance, Institutional and International segments are commensurate

with growth in those businesses. Total amortization of deferred policy acquisition costs increased to $1,438 million in 2001 from $1,383 million in 2000.

Amortization of $1,413 million and $1,478 million are allocated to other expenses in 2001 and 2000, respectively, while the remainder of the amortization

in each year is allocated to investment gains and losses. The decrease in amortization of deferred policy acquisition costs allocated to other expenses is

attributable to a decline in the Individual segment, partially offset by increases in the Reinsurance and International segments. The decline in the Individual

segment is due to refinements in the calculation of estimated gross margins and profits. Contributing to this variance are modifications made in the third

quarter of 2001 relating to the manner in which estimates of future market performance are developed. These estimates are used in determining

unamortized deferred policy acquisition costs balances and the amount of related amortization. The modification will reflect an expected impact of past

MetLife, Inc.

10