MetLife 2001 Annual Report Download - page 7

Download and view the complete annual report

Please find page 7 of the 2001 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

|

|

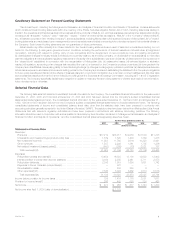

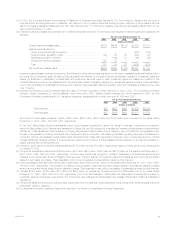

(10) The following provides a reconciliation of net income to adjusted operating income:

For the Years Ended December 31,

2001 2000 1999 1998 1997

(Dollars in millions)

Net income ***************************************************** $ 473 $ 953 $ 617 $ 1,343 $ 1,203

Adjustments to reconcile net income to operating income:

Gross investments losses (gains) ********************************* 737 444 137 (2,629) (1,018)

Income tax on gross investment gains and losses ******************* (208) (175) (92) 883 312

Investment losses (gains), net of income tax ********************** 529 269 45 (1,746) (706)

Amounts allocated to investment gains and losses (see note 4)******** (134) (54) (67) 608 231

Income tax on amounts allocated to investment gains and losses ****** 38 21 45 (204) (71)

Amount allocated to investment gains and losses, net of income tax (96) (33) (22) 404 160

Demutualization costs******************************************* — 230 260 6 —

Income tax on demutualization costs ****************************** — (60) (35) (2) —

Demutualization costs, net of income tax************************* — 170 225 4 —

Payments to former Canadian policyholders ************************ — 327 — — —

Surplus tax**************************************************** — (145) 125 18 (40)

Operating income(a) ********************************************** 906 1,541 990 23 617

Adjustments to reconcile operating income to adjusted operating income:

September 11, 2001 tragedies*********************************** 325 — — — —

Income tax on September 11, 2001 tragedies ********************** (117) — — — —

September 11, 2001 tragedies, net of income tax***************** 208 — — — —

Adjustment for charges for alleged race-conscious underwriting, for

sales practices claims and for personal injury claims caused by

exposure to asbestos or asbestos-containing products(b)*********** 250 — 499 1,895 300

Income tax on such charges ************************************* (91) — (182) (692) (110)

Adjustment for charges for alleged race-conscious underwriting, for

sales practices claims and for personal injury claims caused by

exposure to asbestos or asbestos-containing products, net of

income tax************************************************ 159 — 317 1,203 190

Adjusted operating income(a) ************************************** $1,273 $1,541 $1,307 $ 1,226 $ 807

The Company believes the supplemental operating information presented above allows for a more complete analysis of the results of operations.

Investment gains and losses have been excluded due to their volatility between periods and because such data are often excluded when evaluating

the overall financial performance of insurers. Demutualization costs, payments to former Canadian policyholders, and surplus tax have been

excluded since such amounts are associated with Metropolitan Life’s conversion to a stock company. Operating income and adjusted operating

income should not be considered as a substitute for any GAAP measure of performance. The Company’s method of calculating operating income

and adjusted operating income may be different from the method used by other companies and therefore comparability may be limited.

(a) Operating income and adjusted operating income for the year ended December 31, 2001 include charges related to several business

realignment initiatives of $330 million, net of income tax, and the establishment of a policyholder liability for certain group annuity contracts at New

England Financial of $74 million, net of income tax. See Note 13 of Notes to Consolidated Financial Statements.

(b) The charge for 2001 was recorded to cover costs associated with the anticipated resolution of class action lawsuits and a related regulatory

inquiry pending against Metropolitan Life, involving alleged race-conscious underwriting practices prior to 1973. The charge for 1999 was

principally related to the settlement of a multidistrict litigation proceeding involving alleged improper sales practices, accruals for sales practices

claims not covered by the settlement and other legal costs. The amounts reported for 1998 and 1997 include charges for sales practices claims

and claims for personal injuries caused by exposure to asbestos or asbestos-containing products. See Note 11 of Notes to Consolidated

Financial Statements.

The Company believes that supplemental adjusted operating income data provides information useful in measuring operating trends by excluding

the unusual amounts of expenses associated with the September 11, 2001 tragedies, the anticipated resolution of proceedings alleging race-

conscious underwriting practices, sales practices and asbestos-related claims.

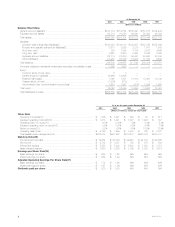

(11) Operating return on equity is defined as operating income divided by average total equity excluding accumulated other comprehensive income

(loss). The Company believes the operating return on equity information presented supplementally allows for a more complete analysis of results of

operations. Accumulated other comprehensive income (loss) has been excluded due to its volatility between periods and because such data is

often excluded when evaluating the overall financial performance of insurers. Operating return on equity should not be considered as a substitute for

any GAAP measure of performance. The Company’s method of calculating operating return on equity may be different from the method used by

other companies and, therefore, comparability may be limited.

(12) Adjusted operating return on equity is defined as adjusted operating income divided by average total equity, excluding accumulated other

comprehensive income (loss). The Company believes that supplemental adjusted operating return on equity data provides information useful in

measuring operating trends by excluding the unusual amounts of expenses associated with the September 11, 2001 tragedies, the anticipated

resolution of proceedings alleging race-conscious underwriting practices, sales practices and asbestos-related claims. Adjusted operating return on

equity should not be considered as a substitute for net income in accordance with GAAP.

MetLife, Inc.

4