MetLife 2001 Annual Report Download

Download and view the complete annual report

Please find the complete 2001 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

|

|

MetLife, Inc. Annual Report 2001

Table of contents

-

Page 1

MetLife, Inc. Annual Report 2001 -

Page 2

... life and annuity clients to view their life insurance policies and annuity contract values and perform select self-service transactions electronically; and the MetLife Auto & Home Agent Resource Site, a Web portal designed to provide agents with the most up-to-date sales and marketing information... -

Page 3

...our new stock-based compensation plans for key officers are implemented, we will continue to ensure that the interests of our shareholders and employees are aligned. The MetLife Board of Directors approved grants of stock options to management, as part of the company's long-term compensation program... -

Page 4

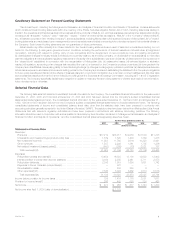

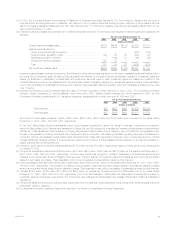

... Data Revenues: Premiums 17,212 Universal life and investment-type product policy fees 1,889 Net investment income(1 11,923 Other revenues 1,507 Net realized investment (losses) gains(2 603) Total revenues(3)(4) Expenses: Policyholder beneï¬ts and claims(5 Interest credited to policyholder... -

Page 5

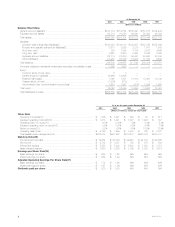

... Sheet Data General account assets(1 Separate account assets Total assets Liabilities: Life and health policyholder liabilities(8 Property and casualty policyholder liabilities(8 Short-term debt Long-term debt Separate account liabilities Other liabilities(1 Total liabilities Company... -

Page 6

... on mutual life insurance companies under Section 809 of the Code. See ''Management's Discussion and Analysis of Financial Condition and Results of Operations.'' Policyholder liabilities include future policy beneï¬ts, policyholder account balances, other policyholder funds, policyholder dividends... -

Page 7

... liability for certain group annuity contracts at New England Financial of $74 million, net of income tax. See Note 13 of Notes to Consolidated Financial Statements. (b) The charge for 2001 was recorded to cover costs associated with the anticipated resolution of class action lawsuits and a related... -

Page 8

... to be recorded as policyholder liabilities beginning January 1, 2001. A signiï¬cant component of the increase in statutory net income is $1.8 billion of investment gains resulting from transactions including the sale of Metropolitan Insurance and Annuity Company (''MIAC'') to MetLife, Inc. and the... -

Page 9

... exchange for that interest, trust interests representing shares of Common Stock held in the MetLife Policyholder Trust, cash or an adjustment to their policy values in the form of policy credits, as provided in the plan. In addition, Metropolitan Life's Canadian branch made cash payments to holders... -

Page 10

... price of $1,006 million. Each unit consists of (i) a contract to purchase shares of Common Stock and (ii) a capital security of MetLife Capital Trust I. On the date of demutualization, Metropolitan Life established a closed block for the beneï¬t of holders of certain individual life insurance... -

Page 11

...'s dental, disability and long-term care businesses. In addition, signiï¬cant premiums received from several existing group life customers in 2001 and the BMA acquisition in 2000 resulted in higher premiums. The 2000 balance includes $124 million in additional insurance coverages purchased by... -

Page 12

... Auto & Home segment. A $110 million decline in the Individual segment is attributable to lower sales of traditional life insurance policies, which reï¬,ects a continued shift in customer preference from those policies to variable life products. Universal life and investment-type product policy fees... -

Page 13

...in the group insurance businesses. Non-deferrable variable expenses include premium tax, commissions and administrative expenses for dental, disability and long-term care businesses. These increases are partially offset by a decline in rebate expenses associated with the Company's securities lending... -

Page 14

... Mexico, South Korea, Taiwan, Spain and Brazil. The decrease in Individual is primarily due to a decline in sales of traditional life insurance policies, which reï¬,ects a continued shift in policyholders' preferences from those policies to variable life products. Universal life and investment-type... -

Page 15

... in the bank-owned life insurance business and increases in the cash values of executive and corporate-owned universal life plans. These increases are partially offset by a decrease in retirement and savings products of $30 million, due to a continued shift in customers' investment preferences from... -

Page 16

... in customer preference from those policies to variable life products. Premiums from annuity and investment-type products declined by $2 million, due to lower sales of supplementary contracts with life contingencies and single premium immediate annuity business. Universal life and investment-type... -

Page 17

... due to a decline in sales of traditional life insurance policies, which reï¬,ects a continued shift in policyholders' preferences from those policies to variable life products. Premiums from annuity and investment products increased by $10 million, or 14%, to $84 million in 2000 from $74 million in... -

Page 18

... insurance coverages purchased by existing customers with funds received in the demutualization. Retirement and savings premiums decreased by $292 million, primarily as a result of $270 million in premiums received in 2000 from existing customers. Universal life and investment-type product policy... -

Page 19

...-owned life insurance business, as well as an increase in the cash values of executive and corporate-owned universal life plans. Retirement and savings decreased by $30 million, or 5%, to $602 million in 2000 from $632 million in 1999, due to a continued shift in customers' investment preferences... -

Page 20

... 2000 period. Interest credited to policyholder account balances relates to amounts credited on deposit-type contracts and certain cash-value contracts. The increase is primarily related to an increase in the underlying account balances due to a new block of single premium deferred annuities... -

Page 21

...which was attributable to increased new business production resulting from an increase in independent agents in this segment's sales force and improved retention in the existing business. Policyholder retention in the standard auto business increased by 1% to 89%. Homeowner premiums increased by $27... -

Page 22

... payments are based upon proï¬tability, investment portfolio performance, new business sales and growth in revenues and proï¬ts. The variable compensation plans reward the employees for growth in their businesses, but also require them to share in the impact of any declines. General MetLife... -

Page 23

...) Revenues Premiums Universal life and investment-type product policy fees Net investment income Other revenues Net investment (losses) gains Total revenues Expenses Policyholder beneï¬ts and claims Interest credited to policyholder account balances Policyholder dividends Payments to... -

Page 24

... in Mexico's participating group business and is in line with the increase in premiums discussed above. Payments of $327 million related to Metropolitan Life's demutualization were made during the second quarter of 2000 to holders of certain policies transferred to Clarica Life Insurance Company in... -

Page 25

.... The Company's principal cash inï¬,ows from its insurance activities come from life insurance premiums, annuity considerations and deposit funds. A primary liquidity concern with respect to these cash inï¬,ows is the risk of early contractholder and policyholder withdrawal. The Company seeks to... -

Page 26

... in letters of credit from various banks were outstanding. Support agreements. In addition to its support agreement with MetLife Funding described above, Metropolitan Life has entered into a net worth maintenance agreement with New England Life Insurance Company (''New England Life''), whereby it is... -

Page 27

... of MetLife Capital Trust I. The primary uses of cash in ï¬nancing activities include cash payments to eligible policyholders in connection with the demutualization, stock repurchases, common stock cash dividends, and the pay-down of short-term debt. Deposits to policyholders' account balances... -

Page 28

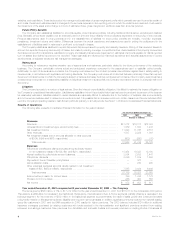

...-for-sale, at fair value 115,398 Mortgage loans on real estate 23,621 Policy loans 8,272 Cash and cash equivalents 7,473 Real estate and real estate joint ventures 5,730 Equity securities and other limited partnership interests 4,700 Other invested assets 3,298 Short-term investments 1,203... -

Page 29

... 31, 2000. The Company invests in privately placed ï¬xed maturities to enhance the overall value of its portfolio, increase diversiï¬cation and obtain higher yields than can ordinarily be obtained with comparable public market securities. Generally, private placements provide the Company with... -

Page 30

... an exchange of debt for equity or a partial forgiveness of principal or interest. The following table presents the estimated fair value of the Company's total ï¬xed maturities classiï¬ed as performing, problem, potential problem and restructured ï¬xed maturities at December 31, 2001 and 2000: At... -

Page 31

...-issued pass-through and collateralized mortgage obligations guaranteed or otherwise supported by the Federal National Mortgage Association, the Federal Home Loan Mortgage Corporation or the Government National Mortgage Association. Other types of mortgage-backed securities comprised the balance... -

Page 32

... home equity loans, credit card receivables, collateralized debt obligations and automobile receivables, are purchased both to diversify the overall risks of the Company's ï¬xed maturities assets and to provide attractive returns. The Company's asset-backed securities are diversiï¬ed both by type... -

Page 33

...regions and property types for commercial mortgage loans at December 31, 2001 and 2000: At December 31, 2001 Carrying Value 2000 % of Carrying Total Value (Dollars in millions) % of Total Region South Atlantic Paciï¬c Middle Atlantic East North Central West South Central New England Mountain... -

Page 34

... in the supply and/or demand for rental space which cause changes in vacancy rates and/or rental rates. Financial risks include the overall level of debt on the property and the amount of principal repaid during the loan term. Capital market risks include the general level of interest rates, the... -

Page 35

...and 2000, respectively. Substantially all of the common stock is publicly traded on major securities exchanges. The carrying value of the other limited partnership interests (which primarily represent ownership interests in pooled investment funds that make private equity investments in companies in... -

Page 36

...to these funds withheld at rates deï¬ned by the treaty terms. The Company's other invested assets represented 1.9% and 1.8% of cash and invested assets at December 31, 2001 and 2000, respectively. Derivative Financial Instruments The Company uses derivative instruments to manage market risk through... -

Page 37

... separate account to support a contract providing guaranteed beneï¬ts, the Company must comply with the asset maintenance requirements stipulated under Regulation 128 of the New York Insurance Department. The Company monitors these requirements at least monthly and, in addition, performs cash ï¬,ow... -

Page 38

... models include asset cash ï¬,ow projections reï¬,ecting interest payments, sinking fund payments, principal payments, bond calls, mortgage prepayments and defaults. New York Insurance Department regulations require that MetLife perform some of these analyses annually as part of the annual proof of... -

Page 39

... to the fair value of currency exchange rates and the Company's equity price sensitive positions at December 31, 2001 and 2000 is set forth in the table below. The potential loss in fair value for each market risk exposure of the Company's portfolio, all of which is non-trading, for the periods... -

Page 40

... and 2000 and for the years ended December 31, 2001, 2000 and 1999: Consolidated Balance Sheets Consolidated Statements of Income Consolidated Statements of Stockholders' Equity Consolidated Statements of Cash Flows Notes to Consolidated Financial Statements Page F-2 F-3 F-4 F-5 F-6 F-8 MetLife... -

Page 41

... Report The Board of Directors and Shareholders of MetLife, Inc.: We have audited the accompanying consolidated balance sheets of MetLife, Inc. and subsidiaries (the ''Company'') as of December 31, 2001 and 2000, and the related consolidated statements of income, stockholders' equity, and cash flows... -

Page 42

... data) 2001 2000 ASSETS Investments: Fixed maturities available-for-sale, at fair value 115,398 Equity securities, at fair value 3,063 Mortgage loans on real estate 23,621 Real estate and real estate joint ventures 5,730 Policy loans 8,272 Other limited partnership interests 1,637 Short-term... -

Page 43

... per share data) 2001 2000 1999 REVENUES Premiums Universal life and investment-type product policy fees Net investment income Other revenues Net investment losses (net of amounts allocable to other accounts of $(134), $(54) and $(67), respectively Total revenues EXPENSES Policyholder bene... -

Page 44

... at December 31, 1999 Policy credits and cash payments to eligible policyholders ** Common stock issued in demutualization Initial public offering of common stock Private placement of common stock Unit offering Treasury stock acquired Dividends on common stock Comprehensive income: Net loss... -

Page 45

... to net cash provided by operating activities: Depreciation and amortization expenses 87) Losses from sales of investments and businesses, net 737 Interest credited to other policyholder account balances 3,084 Universal life and investment-type product policy fees 1,889) Change in premiums and... -

Page 46

... 2001, 2000 AND 1999 (Dollars in millions) 2001 2000 1999 Supplemental disclosures of cash ï¬,ow information: Cash paid during the year for: Interest Income taxes Non-cash transactions during the year: Policy credits to eligible policyholders Business acquisitions - assets Business acquisitions... -

Page 47

... the ''Company'') is a leading provider of insurance and ï¬nancial services to a broad section of individual and institutional customers. The Company offers life insurance, annuities and mutual funds to individuals and group insurance, reinsurance and retirement and savings products and services to... -

Page 48

... SPE, and such equity class has the substantive risks and rewards of the residual interest of the SPE. The Company purchases or receives beneï¬cial interests in SPEs, which generally acquire ï¬nancial assets including corporate equities, debt securities and purchased options. The Company has not... -

Page 49

... of assets or liabilities and anticipated transactions. Additionally, Metropolitan Life enters into income generation and replication derivative transactions as permitted by its derivatives use plan that was approved by the New York State Insurance Department (the ''Department''). The Company... -

Page 50

... life of the contract for participating traditional life, universal life and investment-type products. Generally, deferred policy acquisition costs are amortized in proportion to the present value of estimated gross margins or proï¬ts from investment, mortality, expense margins and surrender... -

Page 51

...force or, for annuities, the amount of expected future policy beneï¬t payments. Premiums related to non-medical health contracts are recognized on a pro rata basis over the applicable contract term. Deposits related to universal life and investment-type products are credited to policyholder account... -

Page 52

... and number of shares assumed purchased represents the dilutive shares. Demutualization and Initial Public Offering On April 7, 2000 (the ''date of demutualization''), Metropolitan Life Insurance Company (''Metropolitan Life'') converted from a mutual life insurance company to a stock life insurance... -

Page 53

... losses. The application of SAB 102 by the Company did not have a material impact on the Company's consolidated ï¬nancial statements. In October 2001, the FASB issued SFAS No. 144, Accounting for the Impairment or Disposal of Long-Lived Assets (''SFAS 144''). SFAS 144 provides a single model for... -

Page 54

...The majority of the Company's disability policies include the provision that such claims be submitted within two years of the traumatic event. The Company's general account investment portfolios include investments, primarily comprised of ï¬xed income securities, in industries that were affected by... -

Page 55

... concentration of credit risk in its ï¬xed maturities portfolio. Securities Lending Program The Company participates in securities lending programs whereby blocks of securities, which are included in investments, are loaned to third parties, primarily major brokerage ï¬rms. The Company requires... -

Page 56

...properties were located in California, New York and Florida, respectively. Generally, the Company (as the lender) requires that a minimum of one-fourth of the purchase price of the underlying real estate be paid by the borrower. Certain of the Company's real estate joint ventures have mortgage loans... -

Page 57

... 27%, 23% and 12% of the Company's real estate holdings were located in New York, California and Texas, respectively. Changes in real estate and real estate joint ventures held-for-sale valuation allowance were as follows: Years ended December 31, 2001 2000 1999 (Dollars in millions) Balance at... -

Page 58

...31, 2001 2000 1999 (Dollars in millions) Fixed maturities Equity securities Mortgage loans on real estate Real estate and real estate joint ventures Policy loans Other limited partnership interests Cash, cash equivalents and short-term investments Other Total Less: Investment expenses Net... -

Page 59

... Value Carrying Assets Liabilities Value (Dollars in millions) 2000 Notional Amount Current Market or Fair Value Assets Liabilities Financial futures Interest rate swaps Floors Caps Foreign currency swaps Exchange traded options Forward exchange contracts Written covered call options Credit... -

Page 60

... BY DERIVATIVE TYPE Financial futures Financial forwards Interest rate swaps Floors Caps Foreign currency swaps Exchange traded options Written covered call options Credit default swaps Total contractual commitments BY STRATEGY Liability hedging Invested asset hedging Portfolio hedging... -

Page 61

... Value (Dollars in millions) December 31, 2000 Assets: Fixed maturities Equity securities Mortgage loans on real estate Policy loans Short-term investments Cash and cash equivalents Mortgage loan commitments Liabilities: Policyholder account balances Short-term debt Long-term debt Payable... -

Page 62

...average earnings history. The Company also provides certain postemployment beneï¬ts and certain postretirement health care and life insurance beneï¬ts for retired employees through insurance contracts. Substantially all of the Company's employees may, in accordance with the plans applicable to the... -

Page 63

... December 31, 2001, 2000 and 1999, respectively. 7. Closed Block On the date of demutualization, Metropolitan Life established a closed block for the beneï¬t of holders of certain individual life insurance policies of Metropolitan Life. Assets have been allocated to the closed block in an amount... -

Page 64

... CLOSED BLOCK Investments: Fixed maturities available-for-sale, at fair value (amortized cost: $25,761 and $25,657, respectively Equity securities, at fair value (amortized cost: $240 and $52, respectively Mortgage loans on real estate Policy loans Short-term investments Other invested assets... -

Page 65

... of Signiï¬cant Accounting Policies-Demutualization and Initial Public Offering.'' Closed block revenues and expenses were as follows: For the Period For the April 7, 2000 Year Ended through December 31, December 31, 2001 2000 (Dollars in millions) REVENUES Premiums Net investment income Net... -

Page 66

... return or account value to the policyholder. Fees charged to the separate accounts by the Company (including mortality charges, policy administration fees and surrender charges) are reï¬,ected in the Company's revenues as universal life and investment-type product policy fees and totaled $564... -

Page 67

... annuity contracts or certiï¬cates. Implementation of the settlement is substantially completed. Similar sales practices class actions against New England Mutual, with which Metropolitan Life merged in 1996, and General American, which was acquired in 2000, have been settled. The New England Mutual... -

Page 68

...to Metropolitan Life's, New England Mutual's or General American's sales of individual life insurance policies or annuities. Over the past several years, these and a number of investigations by other regulatory authorities were resolved for monetary payments and certain other relief. The Company may... -

Page 69

... action is pending in the Supreme Court of the State of New York for New York County and has been brought on behalf of a purported class of beneï¬ciaries of Metropolitan Life annuities purchased to fund structured settlements claiming that the class members should have received common stock or cash... -

Page 70

...Departments in a number of states initiated inquiries in 2000 about possible race-conscious underwriting of life insurance. These inquiries generally have been directed to all life insurers licensed in their respective states, including Metropolitan Life and certain of its subsidiaries. The New York... -

Page 71

... with the assumption of certain funding agreements. The fee was considered part of the purchase price of GenAmerica. GenAmerica is a holding company which included General American Life Insurance Company, approximately 49% of the outstanding shares of RGA common stock, and 61.0% of the outstanding... -

Page 72

... ended December 31, 2001 2000 1999 (Dollars in millions) Tax provision at U.S. statutory rate Tax effect of: Tax exempt investment income Surplus tax State and local income taxes Prior year taxes Demutualization costs Payment to former Canadian policyholders Sales of businesses Other, net... -

Page 73

...of long-term guaranteed interest contracts and structured settlement lump sum contracts accounted for as a ï¬nancing transaction. Reinsurance and ceded commissions payables, included in other liabilities, were $295 million and $225 million at December 31, 2001 and 2000, respectively. F-34 MetLife... -

Page 74

...Trust for the beneï¬t of policyholders of Metropolitan Life in connection with the demutualization. On April 10, 2000, the Holding Company issued 30,300,000 additional shares of common stock as a result of the exercise of over-allotment options granted to underwriters in the initial public offering... -

Page 75

... the distribution. Under the New York Insurance Law, the Superintendent has broad discretion in determining whether the ï¬nancial condition of a stock life insurance company would support the payment of such dividends to its stockholders. The Department has established informal guidelines for such... -

Page 76

METLIFE, INC. NOTES TO CONSOLIDATED FINANCIAL STATEMENTS - (Continued) Shares Weighted Average Exercise Price Granted Canceled Outstanding at end of year Exercisable at end of year Weighted average fair value of options granted during 2001 The following table summarizes information about stock... -

Page 77

...including life insurance, annuities and mutual funds. Institutional offers a broad range of group insurance and retirement and savings products and services, including group life insurance, non-medical health insurance such as short and long-term disability, long-term care, and dental insurance, and... -

Page 78

...Premiums 4,673 Universal life and investment-type product policy fees 1,221 Net investment income 6,475 Other revenues 650 Net investment gains (losses 227 Policyholder beneï¬ts and claims 5,054 Interest credited to policyholder account balances** 1,680 Policyholder dividends 1,742 Payments... -

Page 79

... Institutional Total Premiums Universal life and investment-type product policy fees Net investment income Other revenues Net investment (losses) gains Policyholder beneï¬ts and claims Interest credited to policyholder account balances** Policyholder dividends Demutualization costs Other... -

Page 80

...Inc. Member, Audit Committee and Corporate Social Responsibility Committee JAMES R. HOUGHTON Retired Chairman of the Board and Chief Executive Ofï¬cer Mobil Corporation Member, Compensation Committee and Governance and Finance Committee Executive Vice President, MetLife Financial Services TERENCE... -

Page 81

... Avenue New York, NY 10010 212-578-2211 Internet Address http://www.metlife.com Common Stock and Dividend Information MetLife Inc.'s common stock is traded on the New York Stock Exchange (NYSE) under the trading symbol ''MET.'' The following table presents the high and low closing prices for...