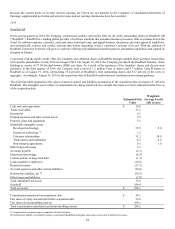

Lexmark 2015 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2015 Lexmark annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

|

|

75

rewards approach under current guidance. The new standard provides guidance for transactions that were not previously addressed

comprehensively, including service revenue and contract modifications, eliminates the software industry revenue recognition

guidance, and requires enhanced disclosures about revenue.

ASU 2014-09 may be adopted through either retrospective application to all periods presented in the financial statements or through a

cumulative effect adjustment to retained earnings by applying the new guidance to contracts that are not completed at the effective

date. In August 2015, the FASB issued Accounting Standards Update No. 2015-14, Revenue from Contracts with Customers (Topic

606): Deferral of the Effective Date to provide a one year delay in the effective date of ASU 2014-09. The effective date of the new

guidance for the Company is now January 1, 2018; however, early application is permitted for the Company’s 2017 fiscal year.

The Company is in the process of evaluating a sample of its contracts with customers under the new standard and cannot currently

estimate the financial statement impact of adoption. The Company hopes to have completed its initial assessment of whether a

material impact is expected by the later part of 2016. A decision has not yet been made regarding the transition method the Company

will use to adopt the new standard.

Areas of potential change for the Company include, but are not limited to:

Units of accounting.

Estimating and allocating variable consideration as well as changes in variable consideration and cumulative adjustments to

revenue.

Changes in allocation due to the removal of guidance for separately priced extended warranties, software, and contingent

revenue limitation.

Determining standalone selling price of software licenses.

Decoupling revenue recognition from invoicing for some goods and services.

Capitalization of certain contract costs, including sales commissions.

In August 2014, the FASB issued Accounting Standards Update No. 2014-15, Presentation of Financial Statements – Going Concern

(Subtopic 205-40): Disclosure of Uncertainties about an Entity’s Ability to Continue as a Going Concern (“ASU 2014-15”). Under

ASU 2014-15, management must evaluate on a quarterly basis whether there are conditions or events that raise substantial doubt about

the entity’s ability to continue as a going concern. Substantial doubt exists when it is probable that the entity will be unable to meet its

obligations as they become due within one year after the date that the financial statements are issued. Disclosures will be required if

conditions or events give rise to substantial doubt. The amendments in ASU 2014-15 will be effective starting with the Company’s

2016 annual financial statements and are not expected to have a material impact.

In January 2016, the FASB issued Accounting Standards Update No. 2016-01, Financial Instruments - Overall (Subtopic 825-10):

Recognition and Measurement of Financial Assets and Financial Liabilities (“ASU 2016-01”). The amendments in ASU 2016-01

require equity investments in unconsolidated entities that are not accounted for under the equity method to be measured at fair value

and any changes in fair value to be recognized in net income each reporting period unless the equity investments do not have readily

determinable fair values. Available-for-sale classification where changes in fair value are reported in other comprehensive income is

no longer available for these securities. Equity investments without readily determinable fair values can be reported at cost, less

impairment, plus or minus changes resulting from observable price changes if they qualify for the practicability exception. ASU 2016-

01 also requires that the realizability of a deferred tax asset related to an available-for-sale debt security be assessed in combination

with other deferred tax assets and makes other changes to existing presentation and disclosure requirements. The amendments in ASU

2016-01 will be effective for the Company starting January 1, 2018 and will require a cumulative-effect adjustment to beginning

retained earnings with limited exceptions. The Company is currently evaluating this guidance but does not expect a material effect on

its financial statements at this time given that the Company has primarily held debt securities in its investment portfolio rather than

equity investments in unconsolidated entities. The Company liquidated its marketable securities investments during 2015 in order to

help fund the acquisition of Kofax.

In February 2016, the FASB issued Accounting Standards Update No. 2016-02, Leases (Topic 842) (“ASU 2016-02”). ASU 2016-02

requires that lessees recognize all leases (other than leases with a term of twelve months or less) on the balance sheet as lease

liabilities, based upon the present value of the lease payments, with corresponding right of use assets. ASU 2016-02 also makes

targeted changes to other aspects of current guidance, including the lease classification criteria and the lessor accounting model. The

amendments in ASU 2016-02 will be effective for the Company on January 1, 2019 and will require modified retrospective

application as of the beginning of the earliest period presented in the financial statements. Early application is permitted. The

Company is currently evaluating this guidance.