Dollar General 2008 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2008 Dollar General annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

|

|

72

Impairment of long-lived assets

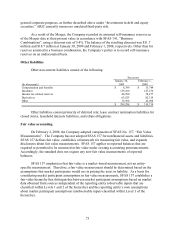

When indicators of impairment are present, the Company evaluates the carrying value of

long-lived assets, other than goodwill, in relation to the operating performance and future cash

flows or the appraised values of the underlying assets. In accordance with SFAS 144,

“Accounting for the Impairment or Disposal of Long-Lived Assets,” the Company reviews for

impairment stores open more than two years for which current cash flows from operations are

negative. Impairment results when the carrying value of the assets exceeds the undiscounted

future cash flows over the life of the lease. The Company’ s estimate of undiscounted future cash

flows over the lease term is based upon historical operations of the stores and estimates of future

store profitability which encompasses many factors that are subject to variability and difficult to

predict. If a long-lived asset is found to be impaired, the amount recognized for impairment is

equal to the difference between the carrying value and the asset’s estimated fair value. The fair

value is estimated based primarily upon estimated future cash flows (discounted at the

Company’ s credit adjusted risk-free rate) or other reasonable estimates of fair market value.

Assets to be disposed of are adjusted to the fair value less the cost to sell if less than the book

value.

The Company recorded impairment charges included in SG&A expense of approximately

$4.0 million in 2008, $0.2 million in the 2007 Predecessor period and $9.4 million in 2006 to

reduce the carrying value of certain of its stores’ assets as deemed necessary based on the

Company’ s evaluation that such amounts would not be recoverable primarily due to insufficient

sales or excessive costs resulting in negative current and projected future cash flows at these

locations. The majority of the 2006 charges were recorded pursuant to certain strategic initiatives

discussed in Note 3.

Goodwill and other intangible assets

The Company amortizes intangible assets over their estimated useful lives unless such

lives are deemed indefinite. Amortizable intangible assets are tested for impairment when

indicators of impairment are present, based on undiscounted cash flows, and if impaired, written

down to fair value based on either discounted cash flows or appraised values.

Goodwill and intangible assets with indefinite lives are tested for impairment annually or

more frequently if indicators of impairment are present and written down to fair value as

required. No impairment of intangible assets has been identified during any of the periods

presented.

The goodwill impairment test is a two-step process that requires management to make

judgments in determining what assumptions to use in the calculation. The first step of the process

consists of estimating the fair value of the Company’ s reporting unit based on valuation

techniques (including a discounted cash flow model using revenue and profit forecasts) and

comparing that estimated fair value with the recorded carrying value, which includes goodwill. If

the estimated fair value is less than the carrying value, a second step is performed to compute the

amount of the impairment by determining an “implied fair value” of goodwill. The determination

of the “implied fair value” of goodwill would require the Company to allocate the estimated fair

value of its reporting unit to its assets and liabilities. Any unallocated fair value would represent